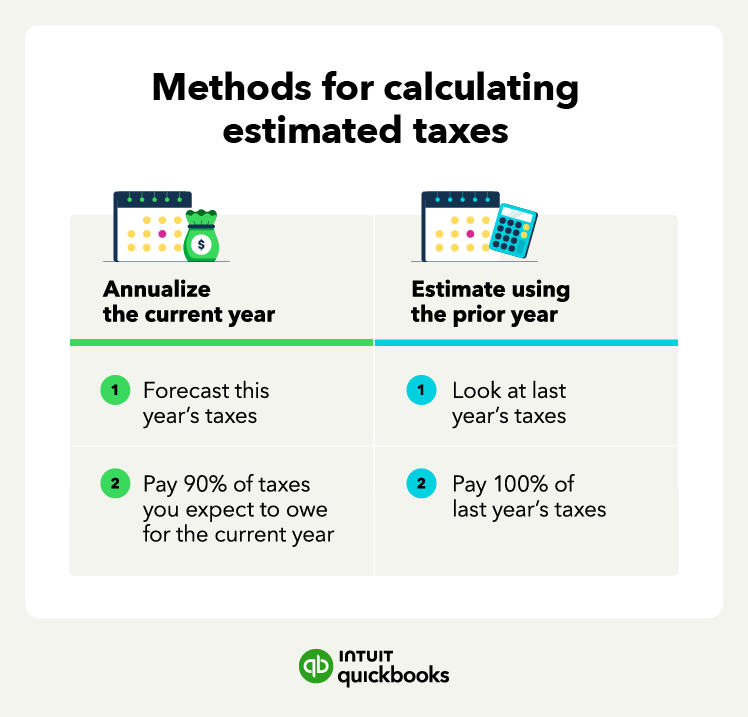

Estimate taxes using prior-year tax

This method is simpler than forecasting your revenue and expenses for the current year. To use the estimate method, you look at what you paid last year and divide by four. That’s your quarterly installment payment for estimated taxes.

For example, if your tax obligation last year was $5,000, your quarterly tax installment would be $1,250 ($5,000 / 4).

Note that if your adjusted gross income last year was more than $150,000, the prior-year percentage increases to 110%. So if your income taxes were $5,000 last year, you’ll need to pay at least $5,500 ($5,000 x 110%) in the current year, or $1,375 per quarter ($5,500 / 4).

If you expect your income in the current year to be the same or higher than last year, this is usually the easiest and safest strategy for figuring out your estimated tax. Just be ready to make up any shortfall in your taxes for the year when you file your return.

How do you pay quarterly estimated taxes?

The IRS can penalize individuals and corporations who don’t file quarterly taxes on due dates. However, they make paying these taxes relatively easy. You can use Form 1040-ES to estimate your quarterly taxes and then file and pay online. You can also link your bank account to EFTPS.gov, known as the electronic federal tax payment system.

You also don’t have to pay estimated taxes just quarterly. You can make estimated tax payments weekly, biweekly, monthly, etc., as long as you pay enough by the end of the quarter.

Estimated tax tips for business owners

One of the biggest struggles with quarterly taxes is not having cash on hand to pay them. Business owners use their income to pay creditors, make investments to grow the business, and more. But business owners and independent contractors must remember that anything they earn is taxable.