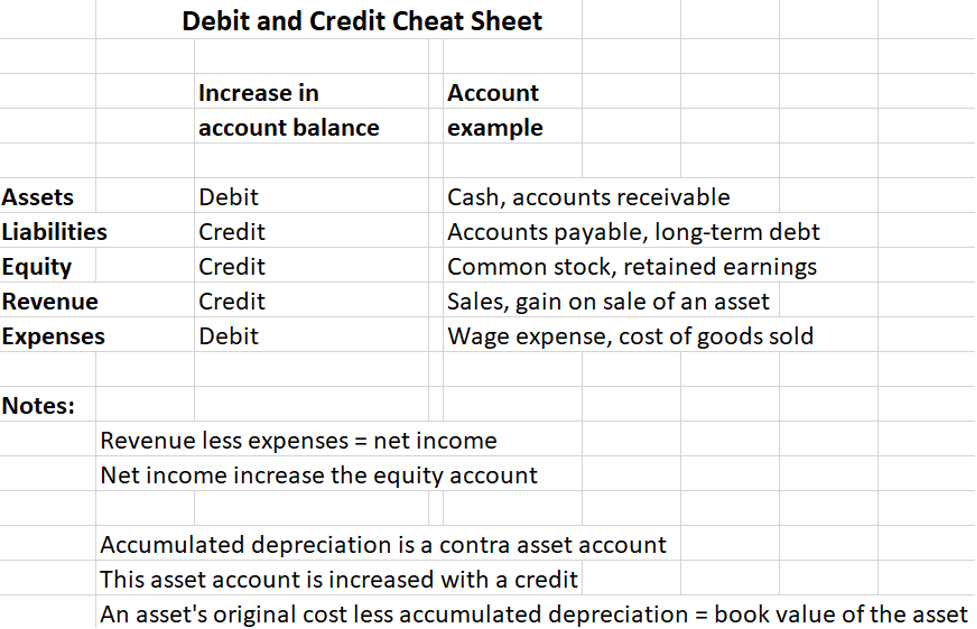

Credit examples

Liabilities and equity are on the right side of the balance sheet formula, and these accounts are increased with a credit entry.

Is equity a debit or credit?

An equity account may include ordinary shares, additional paid in capital and retained earnings, and the balance is increased with a credit. Let’s assume that, on 3 April, a company increases its ordinary shares by $1,000 and additional paid in capital by $6,000 when it issues stock for $7,000 in cash. Here’s the entry:

3 April

Debit #1000 Cash $7,000 (increase)

Credit #8000 Ordinary shares $1,000 (increase)

Credit #8100 Additional paid in capital $6,000 (increase)

(To record the cash payment received for issuance of shares.)

Now, you see that the number of debit and credit entries is different. As long as the total dollar amount of the debits and credits is in balance, the balance sheet formula stays in balance.

Liabilities are amounts owed to third parties.

Are liabilities a debit or credit?

Here’s a 4 April entry to record $12,000 in IT expenses that were not paid in cash immediately:

4 April

Debit #7000 IT expenses $12,000 (increase)

Credit #6000 Accounts payable $12,000 (increase)

(To record IT expenses purchased on credit.)

The expense account is increased with a debit, and the liability account is increased with a credit. Here are some other payment situations and the accounting treatment for each:

- If you pay with a credit card, you have a liability balance with the credit card company. Getting cash back with a purchase increases your debt.

- Debit card payments reduce your checking account balance and are considered a use of cash. A cardholder should not confuse a “debit card” with the debit and credit rules explained here.

- When you swipe your card at an ATM, you’re decreasing the cash balance. Reconcile your bank account immediately after the end of the month to avoid overdraft charges and unnecessary fees.

The majority of activities in the revenue category are sales to customers.

Is revenue a debit or credit?

This 5 April entry posts $15,000 in sales to customers that are paid in cash:

5 April

Debit #1000 Cash $15,000 (increase)

Credit #9000 Revenue: sales $15,000 (increase)

(To record sales to customers paid for in cash.)

Both cash and revenue are increased, and the revenue is increased with a credit.

As you process more accounting transactions, you’ll become more familiar with this process. Cash is typically the account that includes the most accounting activities. When you need to post a new entry, decide if the transaction impacts cash.

Your use of credit, including traditional loans and credit cards, impacts your business credit score. Monitor your company’s credit score, and try to develop sufficient cash inflows to operate your business and avoid using credit.