This list should demonstrate why there is a need to hire a qualified quantity surveyor. Hiring an inexperienced or unqualified surveyor could cause you to either depreciate ineligible items or, perhaps even worse, not deduct items that you’re eligible to depreciate.

2. How does tax depreciation impact mobile phones?

As a small business owner, you or your employees may use mobile phones for work purposes, for example, to contact or manage staff. If this is the case, then you could claim your business’s mobile phones as a tax deduction.

However, to be able to claim the decline in value of the mobile phone over its effective life, the price you paid for it must be over $300. You also need to keep in mind that only a percentage of the mobile phone and its use can be claimed if you use the device for personal and work purposes.

It is also important to keep records for the phone, data and internet, for example:

- Bills for your mobile plan

- Purchase receipts for the devices you buy

- Evidence that you do work-related phone calls from the mobile device

3. How does tax depreciation impact vehicles?

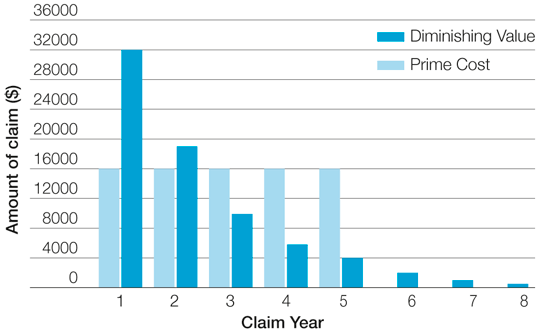

Like property depreciation, vehicle depreciation can also be a complicated subject, and to make sure you are getting the most out of your car’s value it is essential to understand what vehicle depreciation is and how it can help your business.

As a small business owner, there is a chance that you have a vehicle you use for work, and that it depreciates over time thanks to wear and tear.

Depending on your eligibility, you could choose to claim business vehicle depreciation using either general depreciation or simplified depreciation rules, and in order to claim your business vehicle depreciation, you must consider the following points:

- The cost or original value of the car

- The depreciation rule, or method of depreciation chosen

- The effective life of the vehicle

- The luxury car threshold

Once you’ve considered the above, you can determine which depreciation route is best for you and your vehicle, and move to the next steps on claiming relevant tax deductions for the depreciation of your vehicle.

You can read our guide to business vehicle depreciation to learn more about how tax depreciation impacts vehicles.

_resized900x600?scl=1&fmt=jpg&qlt=60,0&resMode=sharp2&op_usm=1.75,0.3,2,0&jpegSize=50)