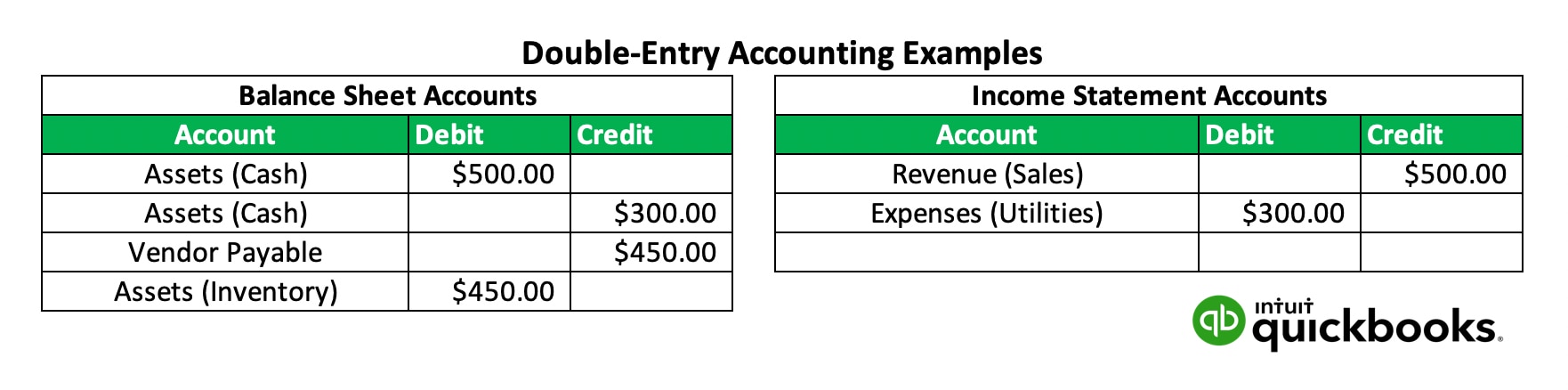

The amount of accounting methods known to man are vast and complicated. It can take decades of study to thoroughly understand the inner workings of the different financial systems and regulations. However, one accounting system that offers a straightforward approach to financial record keeping is the double-entry system.

Double-entry accounting, also known as double-entry bookkeeping, is the standard method of recording transactions in two or more account entries. Just like the name suggests, every transaction will be accounted for in two entries to your account ledger.

So how can you use this accounting method effectively for your small business finances?