The CRA provides comprehensive differences between a registered charity and a non-profit organization ; review the table at the bottom of the FAQ page for specific differences.

The differences between returns for a Not-for-Profit Organization and a registered charity

A registered charity must complete a T3010 form. The T3010 form is available in the FX module.

The CRA provides information related to Charities and giving, as well as a T4033 guide to completing the Registered Charity Information return.

A non-profit may have to complete a T2 return and may have to complete a T1044 form. The T1044 form is available in both the T2 and FX modules.

The CRA provides a T4177 income tax guide to completing the NPO information return.

A not-for-profit may also be exempt from federal income tax as a NPO or registered charity within the means of section 149.

Completing a T2 return for a Not-for-Profit Organization

1. Open the T2 return.

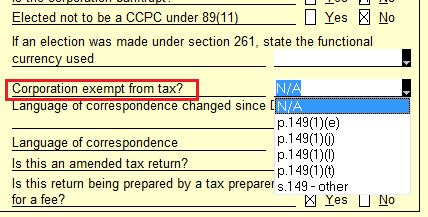

2. Navigate to the Info page of the T2 return.

3. Select the applicable option from the drop-down menu for the question Corporation exempt from tax?

The tax payable is set to nil.

Note: If selecting option 149(1) (t), indicate on T2 line 370 how much income is exempt.

Review more information on 149 options at the Ministry of Justice page.