A Balance Sheet report, also known as a statement of financial position, gives you a snapshot of your business’ financial standing at a specific point in time. It helps you assess your business’ financial health and performance.

This article will cover:

- The basics of a Balance Sheet report

- How to run a Balance Sheet report

- Differences between a Balance Sheet report and other reports

- Comparing Balance Sheet report with Accounts Receivable Ageing reports and different time periods

- Troubleshooting incorrect balance and mismatch with account history

The basics of a Balance Sheet report

The balance sheet shows your business’ assets (what it owns), liabilities (how much it owes), and equity (the owners’ stake in the business).

The balance sheet follows a simple equation: Shareholders' Equity = Liabilities + Assets.

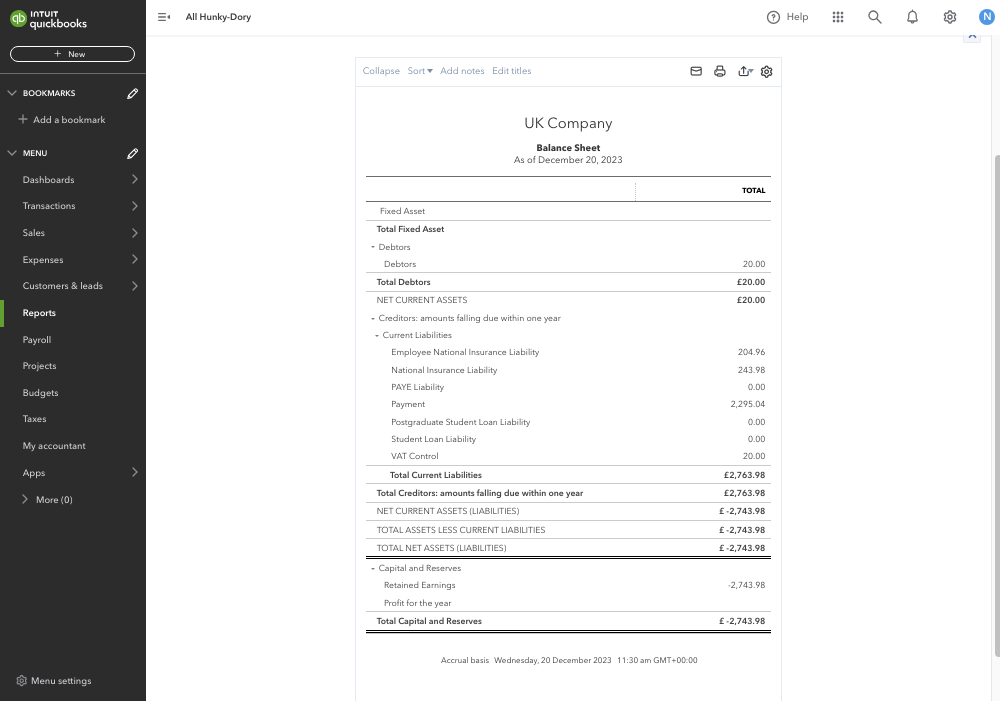

Here’s an example of what a Balance Sheet report looks like:

Let’s go over the main components of a Balance Sheet report:

- Assets

Assets can include things like cash in the bank, money owed to the company, or stock on hand.

- Liabilities

These can include any bills to be paid or loans that your company owes.

- Equity

This represents the owners’ stake in the company, including any products that have been kept or invested back into the business.

Note: The total for equity includes your company's net income for the financial year to date.

Run a Balance Sheet report

- Go to Reports (Take me there).

- Select Business overview.

- Select Balance Sheet.

- Select the date range for the report.

- Select Run report.

- The Balance Sheet report will be displayed on your screen. You can view the report in the browser or export it to a PDF or Excel file.

Tip: To see a higher-level summary, run the Balance Sheet Summary report instead.

Differences between a Balance Sheet report and other reports

Your Balance Sheet report may not match your other reports, even if the filters are the same. This happens because:

- Your Balance Sheet report is a cumulative report that carries a beginning balance.

- In other reports, the date range you choose only applies to net income and the specific account you select within the report.

For example, if you have GBP £50 of VAT in March and GBP £60 in April, the Balance Sheet will show a total of GBP £110 for the VAT liability account.

If you set the date range for the report as April, the cumulative total of GBP £110 will still show. However, if you select GBP £110, the transaction detail report will show a beginning balance of GBP £50 and a transaction of GBP £60 for April.

In addition, the Sales by Product/Service report is limited to the date range you set. So, if you set the report date for April, it will accurately reflect only April and show the GBP £60 amount.

Comparing a Balance Sheet report and Accounts Receivable Ageing reports and different time period

To compare the Balance Sheet report with the Accounts Receivable Ageing Summary or Accounts Receivable Ageing Detail reports, follow these steps:

- Go to Reports (Take me there).

- Select Who owes you.

- Select Accounts receivable ageing summary or Accounts receivable ageing detail.

- Make sure you specify the correct Ageing method.

- If you run a Balance Sheet report for a past date, select the Report period for the Ageing method on your Accounts Receivable Ageing reports. This will help make sure that the Total Debtors matches on both reports.

Comparing a Balance Sheet report to different time periods

You can customise your Balance Sheet report to show Year-over-Year columns.

- Go to Reports (Take me there).

- Select Business overview.

- Select Balance Sheet Comparison.

- Select Customise.

- Under Rows/Columns, select the Change columns.

- Select the appropriate checkbox to see the desired period.

- Select Run report.

Troubleshooting Balance Sheet report

Incorrect balance

The value of assets should always be equal to the combined value of liabilities and equity, which can be calculated using the formula Assets - Liabilities = Equity.

To troubleshoot an unbalanced balance sheet, follow these steps:

- Review each account on the report to see the transactions associated with the balance of each account.

- Run the report for the year-to-date (YTD) period and gradually narrow down on the date range each month until you pinpoint the specific day when the balance sheet becomes unbalanced.

- Check the transactions during that narrowed date range to find the specific transaction causing the imbalance.

- Take the necessary steps to fix the issue and bring the balance sheet back to balance.

Mismatch with account history

If your company's financial year doesn't follow the same dates as the regular calendar year, you might find that the numbers on your financial report and account history don't match up.

This happens because the balance sheet is typically prepared based on the calendar year. But don't worry, there are a couple of ways to fix this problem.

Option 1: Change the date of the report to match your financial year

- Go to Reports (Take me there).

- Select Business overview.

- Select Balance Sheet.

- Select Customise.

- Select the appropriate Report period.

- Select Run report.

Option 2: Change your financial year on the company file

- Go to Settings ⚙, then select Account and settings.

- Select Advanced.

- In the Accounting section, select the edit ✏️ icon.

- From the First month of tax year dropdown, select January.

- Select Save and Done.