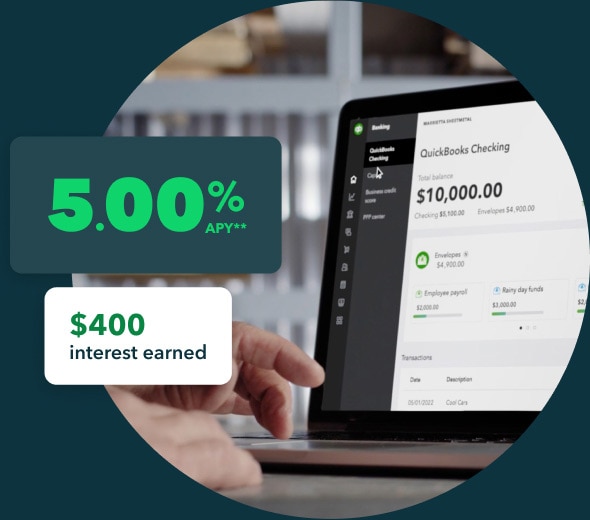

Earn 5.00% APY** with savings envelopes—that’s over 70x the US average.1

With fast payment deposits and high-yield savings, a QuickBooks Checking bank account lets you move, manage, and grow your money with confidence.

QuickBooks and Intuit are a technology company, not a bank. Banking services provided by Green Dot Bank. ![]()

Discover smart ways to save

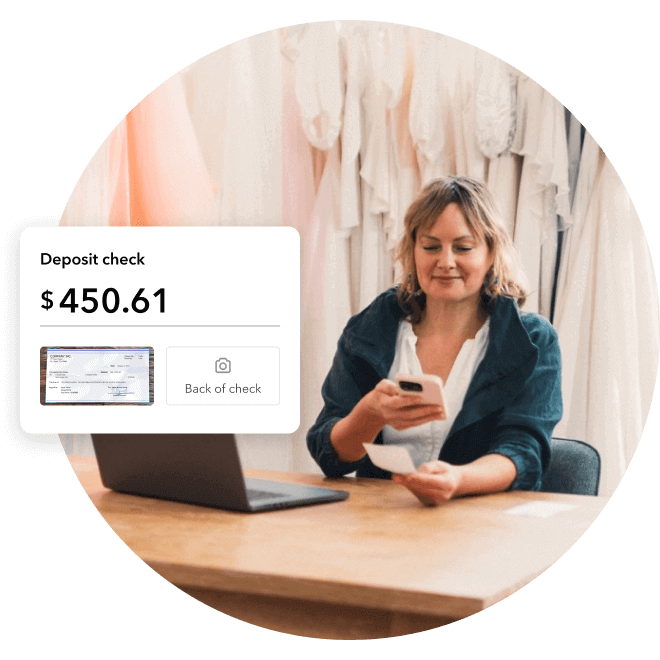

Payments go straight to the bank

Deposit eligible payments into QuickBooks Checking to see your money faster—without the fees.**

Maximize money with high-yield savings

Make your money work harder—move funds to savings envelopes and earn 5.00% APY.**

Fewer fees, more money for your business

Your checking account is free to open—no monthly fees, overdraft fees, or minimum balances.**

Complete banking, made for you

With QuickBooks, you have everything you need to streamline money management and then some.

Deposit customer payments, upload checks, and match them to invoices in real time. Use ACH and wire transfers to move money when you need to—no matter where you’re working.

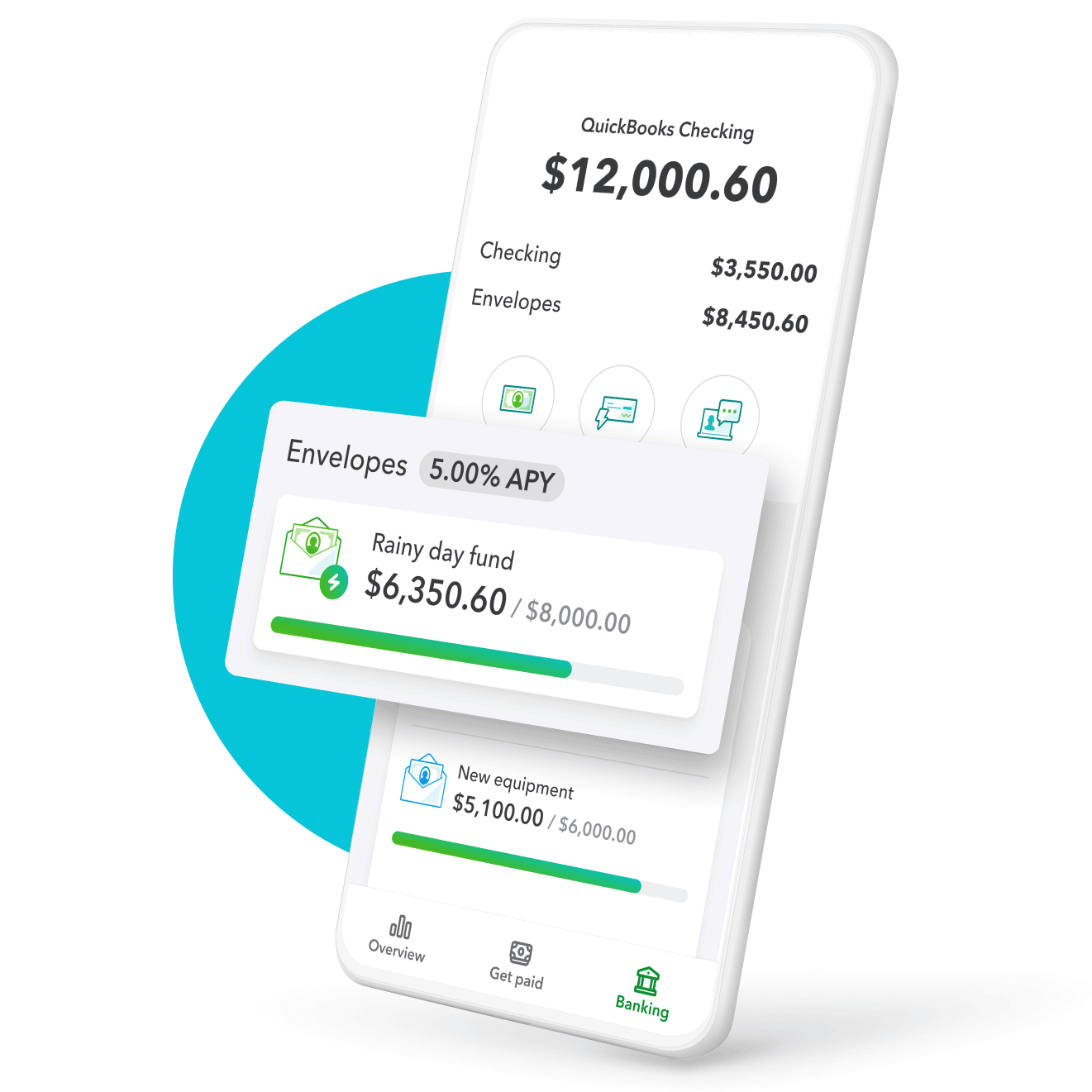

Every dollar put away in savings envelopes earns you interest at over 70x the U.S. average. Build your rainy-day fund and rest easy knowing your money’s working, even when you’re not.1

Once deposited, spend funds right away using your QuickBooks Debit Card. Or visit over 19,000 fee-free AllPoint ATMs, and even add your card to Apple Pay or Google Pay.**

QuickBooks can automatically move what you owe in sales taxes to a separate envelope so you stay ready. If you have a QuickBooks Online plan with QuickBooks Payroll, you can set aside what you owe for payroll and QuickBooks will automatically apply those funds when you pay your team.**

Do even more with QuickBooks Online

Get an accounting plan to keep your banking and books connected, so you’re always up to date.

Get instant deposit at no added cost

Get paid faster by depositing payments into QuickBooks Checking. Eligible payments hit the bank instantly, and we waive the 1.75% fee.**

Do bookkeeping without the busywork

QuickBooks matches your payments and spending for you and lets you attach receipts to transactions.** Read-only access helps accountants stay informed.

Discover all-in-one financial clarity

Your QuickBooks Checking bank account connects with other QuickBooks tools like payments, payroll, and bill pay to help you manage everything in one place.

Banking that fits your business

Compare our QuickBooks solutions to see what’s right for you. Manage just your business money or get a plan with accounting tools, too.

Manage money

Manage money and accounting

QuickBooks Money

Money management features without the bookkeeping.

Just pay per transaction

Just pay per transaction

Business bank account

Get a business bank account that’s free to open—with no monthly fees and no minimum balances.**

Earn 5.00% APY

Every dollar put away in savings envelopes earns you interest at over 70x the U.S. average.

NEW

Accept payments

Give customers flexible ways to pay—via PayPal,** Venmo, Apple Pay®, credit, debit, or ACH payments.

Payment transaction rates

Get competitive payment processing rates with no setup costs or hidden fees—just pay as you go.

Invoices

Send instantly payable invoices, schedule recurring invoices, track their status, send payment reminders, and match payments to invoices—automatically.

Same-day deposit

Eligible payments land in your bank account the same day—nights, weekends, and holidays—so you can access cash fast at no extra cost.**

Business Network

Sync with customers, see their contact info, send invoices, and accept and track payments with ease.

Cash flow history

See your business money come in and out over time, so you can make smart business decisions and pivot as you grow.

OR

QuickBooks Simple Start

Start with basic bookkeeping and money management tools.

Business bank account

Open a QuickBooks Checking account for free—there’s no monthly fees or minimum balance.**

Earn 5.00% APY

Every dollar put away in savings envelopes earns you interest at over 70x the U.S. average.

NEW

Accept payments

Give customers flexible ways to pay—via PayPal,** Venmo, Apple Pay®, credit, debit, or ACH payments.

Payment transaction rates

Get competitive payment processing rates with no setup costs or hidden fees—just pay as you go.

Invoices

Send instantly payable invoices, schedule recurring invoices, track their status, send payment reminders, and match payments to invoices—automatically.

Instant deposit

Get instant access to eligible payments no matter what time of day you get paid.**

Business Network

Sync with customers, see their contact info, send invoices, and accept and track payments with ease.

Cash flow history

See your business money come in and out over time, so you can make smart business decisions and pivot as you grow.

In-person payments

Let customers insert, tap, or use digital wallets to make in-person payments seamless.**

Recurring invoices

Automate recurring invoices and give your customers the option to set up automatic payments.

Estimates

Customize estimates, accept mobile signatures, see estimate status, and convert estimates into invoices.

Line of Credit

Apply for a flexible line of credit to get cash when you need it.

Business loan

Explore funding options with competitive rates—no hidden fees and no surprises.

Free guided setup

A QuickBooks expert can help you set up your chart of accounts, connect your banks, and show you best practices.

Income and expenses

Securely import transactions and organize your finances automatically.

Tax deductions

Share your books with your accountant or export important documents.**

General reports

Run and export reports including profit & loss, expenses, and balance sheets.*

Receipt capture

Snap photos of your receipts and categorize them on the go.**

Mileage tracking

Automatically track miles, categorize trips, and get sharable reports.**

Track sales

Accept credit cards anywhere, connect to e-commerce tools, and calculate taxes automatically.**

Contractors

Assign vendor payments to 1099 categories, see payment history, prepare and file 1099s from QuickBooks.**

Connect 1 sales channel

Connect 1 online sales channel and automatically sync with QuickBooks.

QuickBooks Essentials

Manage accounting, business money, and automate work.

Business bank account

Open a QuickBooks Checking account for free—there’s no monthly fees or minimum balance.**

Earn 5.00% APY

Every dollar put away in savings envelopes earns you interest at over 70x the U.S. average.

NEW

Accept payments

Give customers flexible ways to pay—via PayPal,** Venmo, Apple Pay®, credit, debit, or ACH payments.

Payment transaction rates

Get competitive payment processing rates with no setup costs or hidden fees—just pay as you go.

Invoices

Send instantly payable invoices, schedule recurring invoices, track their status, send payment reminders, and match payments to invoices—automatically.

Instant deposit

Get instant access to eligible payments no matter what time of day you get paid.**

Business Network

Sync with customers, see their contact info, send invoices, and accept and track payments with ease.

Cash flow history

See your business money come in and out over time, so you can make smart business decisions and pivot as you grow.

In-person payments

Let customers insert, tap, or use digital wallets to make in-person payments seamless.**

Recurring invoices

Automate recurring invoices and give your customers the option to set up automatic payments.

Estimates

Customize estimates, accept mobile signatures, see estimate status, and convert estimates into invoices.

Line of Credit

Apply for a flexible line of credit to get cash when you need it.

Business loan

Explore funding options with competitive rates—no hidden fees and no surprises.

Manage bills

Organize and track your business bills online.

Free guided setup

A QuickBooks expert can help you set up your chart of accounts, connect your banks, and show you best practices.

Income and expenses

Securely import transactions and organize your finances automatically.

Tax deductions

Share your books with your accountant or export important documents.**

Enhanced reports

Run and export reports including profit & loss, expenses, and balance sheets.*

Receipt capture

Snap photos of your receipts and categorize them on the go.**

Mileage tracking

Automatically track miles, categorize trips, and get sharable reports.**

Track sales

Accept credit cards anywhere, connect to e-commerce tools, and calculate taxes automatically.**

Contractors

Assign vendor payments to 1099 categories, see payment history, prepare and file 1099s from QuickBooks.**

Connect 3 sales channels

Connect up to 3 online sales channels and automatically sync with QuickBooks.

Enter time

Enter employee time by client/project and automatically add it to invoices.

QuickBooks Plus

Manage accounting, business money, and project profitability.

Business bank account

Open a QuickBooks Checking account for free—there’s no monthly fees or minimum balance.**

Earn 5.00% APY

Every dollar put away in savings envelopes earns you interest at over 70x the U.S. average.

NEW

Accept payments

Give customers flexible ways to pay—via PayPal,** Venmo, Apple Pay®, credit, debit, or ACH payments.

Payment transaction rates

Get competitive payment processing rates with no setup costs or hidden fees—just pay as you go.

Invoices

Send instantly payable invoices, schedule recurring invoices, track their status, send payment reminders, and match payments to invoices—automatically.

Instant deposit

Get instant access to eligible payments no matter what time of day you get paid.**

Business Network

Sync with customers, see their contact info, send invoices, and accept and track payments with ease.

Cash flow history

See your business money come in and out over time, so you can make smart business decisions and pivot as you grow.

In-person payments

Let customers insert, tap, or use digital wallets to make in-person payments seamless.**

Recurring invoices

Automate recurring invoices and give your customers the option to set up automatic payments.

Estimates

Customize estimates, accept mobile signatures, see estimate status, and convert estimates into invoices.

Line of Credit

Apply for a flexible line of credit to get cash when you need it.

Business loan

Explore funding options with competitive rates—no hidden fees and no surprises.

Manage bills

Organize and track your business bills online.

Free guided setup

A QuickBooks expert can help you set up your chart of accounts, connect your banks, and show you best practices.

Income and expenses

Securely import transactions and organize your finances automatically.

Tax deductions

Share your books with your accountant or export important documents.**

Comprehensive reports

Run and export reports including profit & loss, expenses, and balance sheets.*

Receipt capture

Snap photos of your receipts and categorize them on the go.**

Mileage tracking

Automatically track miles, categorize trips, and get sharable reports.**

Track sales

Accept credit cards anywhere, connect to e-commerce tools, and calculate taxes automatically.**

Contractors

Assign vendor payments to 1099 categories, see payment history, prepare and file 1099s from QuickBooks.**

Connect 3 sales channels

Connect up to 3 online sales channels and automatically sync with QuickBooks.

Enter time

Enter employee time by client/project and automatically add it to invoices.

Inventory

Track products, cost of goods, see what’s popular, create purchase orders, and manage vendors.

Project profitability

Track all your projects in one place, track labor costs, payroll and expenses.

Discover the key differences

Compare our main features to see which plan is right for you.

QuickBooks Money

QuickBooks Money is one tool for managing payments and banking. Signing up is free, accounting features not included.

QuickBooks Online plans

Paid accounting plans that include access to online payments, banking, and connected business tools.

Free-to-open bank account

No monthly fees or minimums**

![]()

![]()

5.00% APY

Stash money in Envelopes and earn**

![]()

![]()

Accounting

Your bank and books stay connected**

![]()

Free-to-open bank account

No monthly fees or minimums**

QuickBooks Money

QuickBooks Money is one tool for managing payments and banking. Signing up is free, accounting features not included.

![]()

QuickBooks Online plans

Paid accounting plans that include access to online payments, banking, and connected business tools.

![]()

5.00% APY

Stash money in Envelopes and earn**

QuickBooks Money

QuickBooks Money is one tool for managing payments and banking. Signing up is free, accounting features not included.

![]()

QuickBooks Online plans

Paid accounting plans that include access to online payments, banking, and connected business tools.

![]()

Accounting

Your bank and books stay connected**

QuickBooks Money

QuickBooks Money is one tool for managing payments and banking. Signing up is free, accounting features not included.

QuickBooks Online plans

Paid accounting plans that include access to online payments, banking, and connected business tools.

![]()

Frequently asked questions

Build your knowledge

Check out these helpful resources to learn the ins-and-outs of opening a business bank account.

Call Sales: 1-800-285-4854