Everything you need to know about tracking and managing inventory for your business.

Inventory

Manage inventory with ease

Inventory tracking

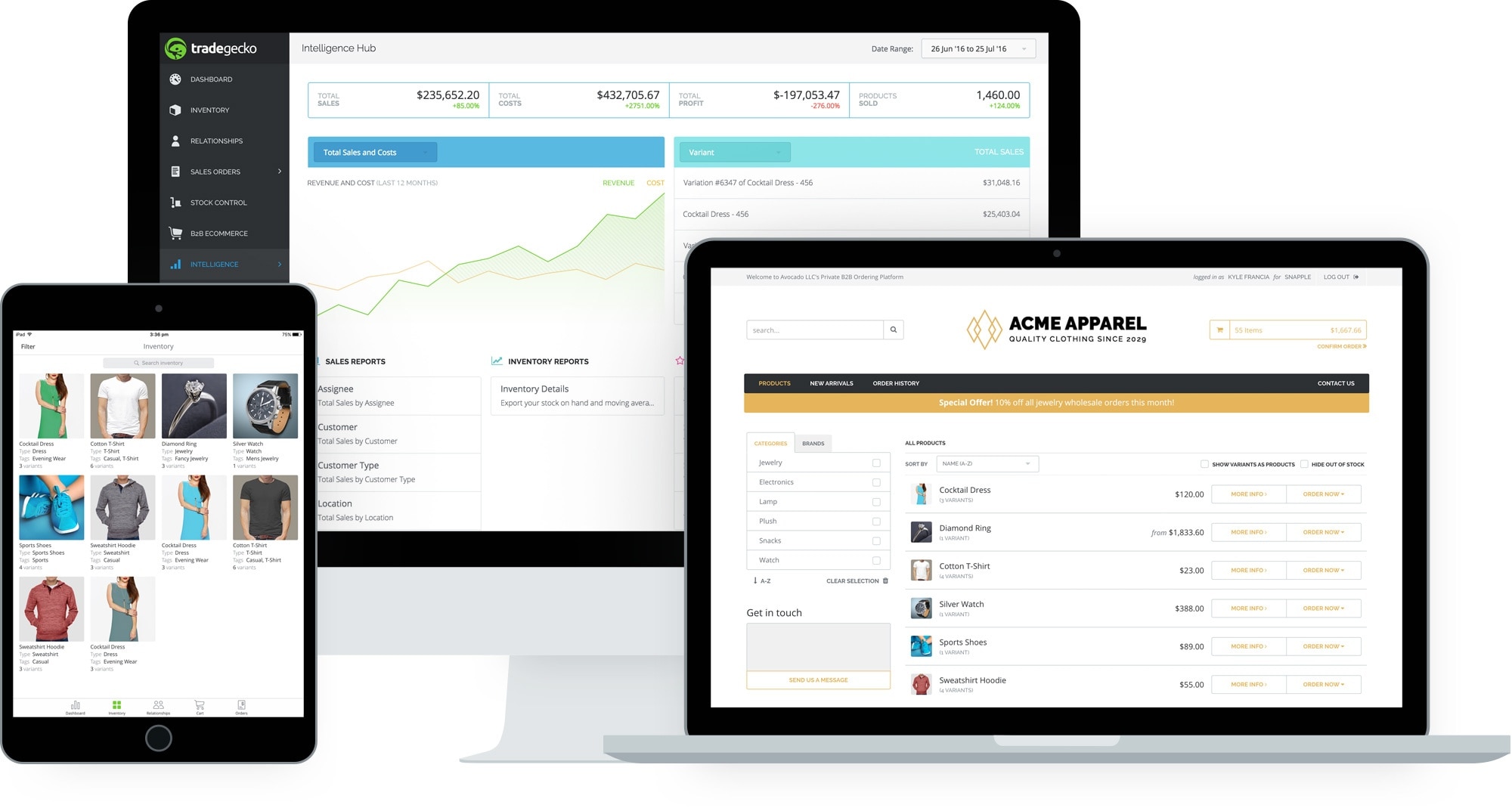

Boost your business with inventory analysis

Get started with e-commerce

Inventory metrics you should know

Inventory by industry

Types of inventory

Small Business Templates

Looking for something else?

Call Sales: 1-877-683-3280