Earn 5.00% APY** with savings envelopes—that’s over 70x the U.S. average.1

We keep track of thousands of tax laws so you don’t have to.

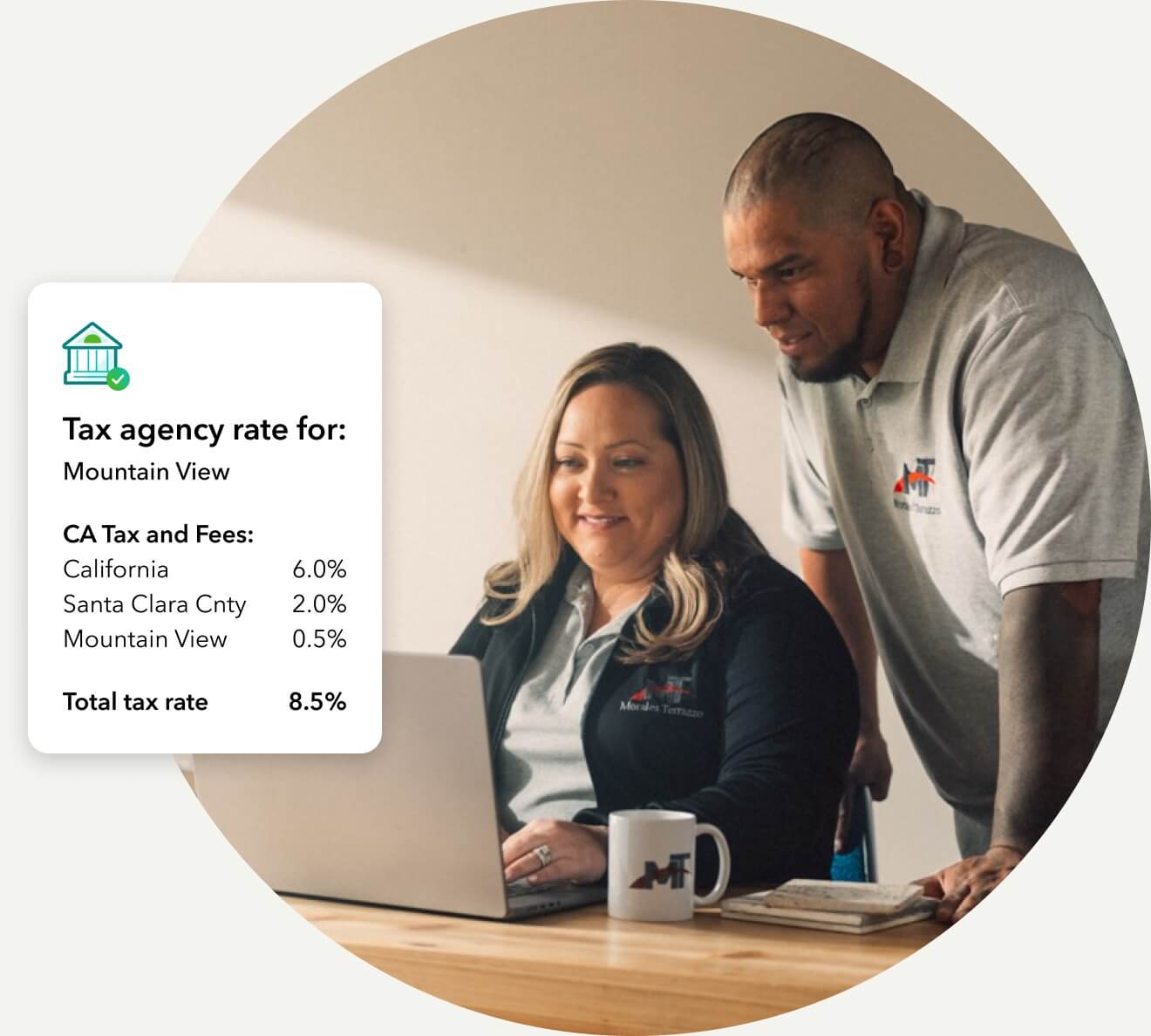

Sales tax calculations made easy

Automatic sales tax calculation

When you add sales tax to an invoice in QuickBooks, the calculations are automatically taken care of. We calculate the sales tax rate based on date, location, type of product or service, and customer you indicate.

Product categorization

Rules for how to tax a product can change from state to state. Once your products are categorized, QuickBooks will make sure the correct rate is applied to your transactions based on the product category and the location of sale you indicate.

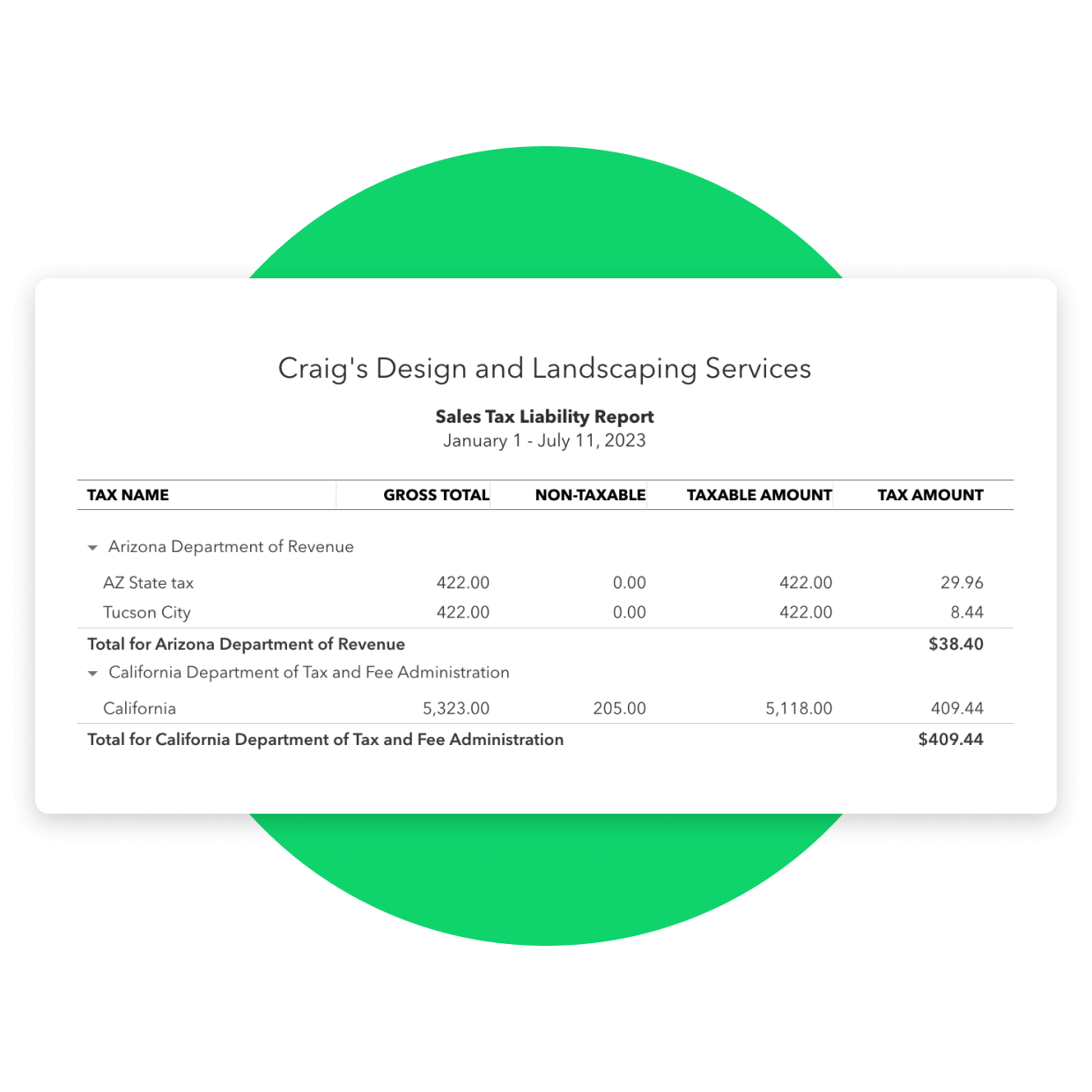

Know how much you owe

You can view your sales tax information any time with the Sales Tax Liability Report. This on-demand report will keep you up-to-date on your taxable and nontaxable sales, all broken down by tax agency.

Plans for every kind of business

Now with Live Assisted Bookkeeping (add $50/month)

1

Select plan

2

Add Payroll

3

Checkout

Simple Start

$30

$15/mo

Save 50% for 3 months*

Access expert tax help

Save time and effort by seamlessly moving from books to taxes, then prepare your current tax year return with unlimited expert help to get every credit you deserve. Access live tax experts powered by TurboTax and pay only when you file. Costs vary by entity type. Subject to eligibility.

NEW

with QuickBooks Live Tax

Free guided setup

A QuickBooks expert can help you set up your chart of accounts, connect your banks, and show you best practices.

Income and expenses

Securely import transactions and organize your finances automatically.

Banking with 5.00% APY

Every dollar put away in savings envelopes earns you interest at over 70x the U.S. average.

NEW

Bookkeeping automation

Automate bookkeeping to cut down on tedious tasks and get more time to focus on your business.

NEW

Invoice and payments

Accept credit cards and bank transfers in the invoice with QuickBooks Payments, get status updates and reminders.**

Tax deductions

Share your books with your accountant or export important documents.**

General reports

Run and export reports including profit & loss, expenses, and balance sheets.*

Receipt capture

Snap photos of your receipts and categorize them on the go.**

Mileage tracking

Automatically track miles, categorize trips, and get sharable reports.**

Cash flow

Get paid online or in person, deposited instantly, if eligible.

Sales and sales tax

Accept credit cards anywhere, connect to e-commerce tools, and calculate taxes automatically.**

Estimates

Customize estimates, accept mobile signatures, see estimate status, and convert estimates into invoices.**

Contractors

Assign vendor payments to 1099 categories, see payment history, prepare and file 1099s from QuickBooks.**

Connect 1 sales channel

Connect 1 online sales channel and automatically sync with QuickBooks.

Bookkeeping support

Add $50 per month

Add $50 per month

Essentials

$60

$30/mo

Save 50% for 3 months*

Access expert tax help

Save time and effort by seamlessly moving from books to taxes, then prepare your current tax year return with unlimited expert help to get every credit you deserve. Access live tax experts powered by TurboTax and pay only when you file. Costs vary by entity type. Subject to eligibility.

NEW

with QuickBooks Live Tax

Free guided setup

A QuickBooks expert can help you set up your chart of accounts, connect your banks, and show you best practices.

Income and expenses

Securely import transactions and organize your finances automatically.

Banking with 5.00% APY

Every dollar put away in savings envelopes earns you interest at over 70x the U.S. average.

NEW

Bookkeeping automation

Automate bookkeeping to cut down on tedious tasks and get more time to focus on your business.

NEW

Invoice and payments

Accept credit cards and bank transfers in the invoice with QuickBooks Payments, get status updates and reminders.**

Tax deductions

Share your books with your accountant or export important documents.**

Enhanced reports

Know how your business is doing with sales, accounts receivable, and accounts payable reports.*

Receipt capture

Snap photos of your receipts and categorize them on the go.**

Mileage tracking

Automatically track miles, categorize trips, and get sharable reports.**

Cash flow

Get paid online or in person, deposited instantly, if eligible.

Sales and sales tax

Accept credit cards anywhere, connect to e-commerce tools, and calculate taxes automatically.**

Estimates

Customize estimates, accept mobile signatures, see estimate status, and convert estimates into invoices.**

Contractors

Assign vendor payments to 1099 categories, see payment history, prepare and file 1099s from QuickBooks.**

Connect 3 sales channels

Connect up to 3 online sales channels and automatically sync with QuickBooks.

Multiple currencies

Record transactions in other currencies without worrying about exchange rate conversions.

Bill management

Organize and track your business bills online.

Includes 3 users

Invite your accountant to access your books, control user-access levels, and share reports without sharing a log-in.**

Enter time

Enter employee time by client/project and automatically add it to invoices.

Bookkeeping support

- Add $50 per month

Plus

$90

$45/mo

Save 50% for 3 months*

Access expert tax help

Save time and effort by seamlessly moving from books to taxes, then prepare your current tax year return with unlimited expert help to get every credit you deserve. Access live tax experts powered by TurboTax and pay only when you file. Costs vary by entity type. Subject to eligibility.

NEW

with QuickBooks Live Tax

Free guided setup

A QuickBooks expert can help you set up your chart of accounts, connect your banks, and show you best practices.

Income and expenses

Securely import transactions and organize your finances automatically.

Banking with 5.00% APY

Every dollar put away in savings envelopes earns you interest at over 70x the U.S. average.

NEW

Bookkeeping automation

Automate bookkeeping to cut down on tedious tasks and get more time to focus on your business.

NEW

Invoice and payments

Accept credit cards and bank transfers in the invoice with QuickBooks Payments, get status updates and reminders.**

Tax deductions

Share your books with your accountant or export important documents.**

Comprehensive reports

Stay on track with inventory reports, enhanced sales reports, and profitability reports.*

Receipt capture

Snap photos of your receipts and categorize them on the go.**

Mileage tracking

Automatically track miles, categorize trips, and get sharable reports.**

Cash flow

Get paid online or in person, deposited instantly, if eligible.

Sales and sales tax

Accept credit cards anywhere, connect to e-commerce tools, and calculate taxes automatically.**

Estimates

Customize estimates, accept mobile signatures, see estimate status, and convert estimates into invoices.**

Contractors

Assign vendor payments to 1099 categories, see payment history, prepare and file 1099s from QuickBooks.**

Connect all sales channels

Connect any available online sales channels and automatically sync with QuickBooks.

Multiple currencies

Record transactions in other currencies without worrying about exchange rate conversions.

Bill management

Organize and track your business bills online.

Includes 5 users

Invite your accountant to access your books, control user-access levels, and share reports without sharing a log-in.**

Enter time

Enter employee time by client/project and automatically add it to invoices.

Inventory

Track products, cost of goods, see what’s popular, create purchase orders, and manage vendors.

Project profitability

Track all your projects in one place, track labor costs, payroll and expenses.

Financial planning

Create budgets with real-time data you can collaborate with your team on.

NEW

Bookkeeping support

- Add $50 per month

Advanced

$200

$100/mo

Save 50% for 3 months*

Access expert tax help

Save time and effort by seamlessly moving from books to taxes, then prepare your current tax year return with unlimited expert help to get every credit you deserve. Access live tax experts powered by TurboTax and pay only when you file. Costs vary by entity type. Subject to eligibility.

NEW

with QuickBooks Live Tax

Free guided setup

A QuickBooks expert can help you set up your chart of accounts, connect your banks, and show you best practices.

Income and expenses

Securely import transactions and organize your finances automatically.

Banking with 5.00% APY

Every dollar put away in savings envelopes earns you interest at over 70x the U.S. average.

NEW

Bookkeeping automation

Automate bookkeeping to cut down on tedious tasks and get more time to focus on your business.

NEW

Invoice and payments

Accept credit cards and bank transfers in the invoice with QuickBooks Payments, get status updates and reminders.**

Tax deductions

Share your books with your accountant or export important documents.**

Powerful reports

Monitor financial metrics and build customized dashboards that measure performance.

Receipt capture

Snap photos of your receipts and categorize them on the go.**

Mileage tracking

Automatically track miles, categorize trips, and get sharable reports.**

Cash flow

Get paid online or in person, deposited instantly, if eligible.

Sales and sales tax

Accept credit cards anywhere, connect to e-commerce tools, and calculate taxes automatically.**

Estimates

Customize estimates, accept mobile signatures, see estimate status, and convert estimates into invoices.**

Contractors

Assign vendor payments to 1099 categories, see payment history, prepare and file 1099s from QuickBooks.**

Connect all sales channels

Connect any available online sales channels and automatically sync with QuickBooks.

Multiple currencies

Record transactions in other currencies without worrying about exchange rate conversions.

Bill management

Organize and track your business bills online.

Includes 25 users

Invite your accountant to access your books, control user-access levels, and share reports without sharing a log-in.**

Enter time

Enter employee time by client/project and automatically add it to invoices.

Inventory

Track products, cost of goods, see what’s popular, create purchase orders, and manage vendors.

Project profitability

Track all your projects in one place, track labor costs, payroll and expenses.

Financial planning

Create budgets with real-time data you can collaborate with your team on.

NEW

Auto-track fixed assets

Automatically track fixed asset values, access all fixed asset info in one spot, and get insights about what may come next.

NEW

Data sync with Excel

Seamlessly send data back and forth between QuickBooks Online Advanced and Excel for more accurate business data and custom insights.

Employee expenses

Employees submit expenses in QuickBooks, so everything’s in one place and easy to track.

Batch invoices and expenses

Create invoices, enter, edit, and send multiple invoices faster.**

Custom access controls

Easily control who sees your data, assign work to specific users, and create custom permissions.

Workflow automation

Save time and mitigate risk with automated workflows and set reminders for improved cash flows and more.

Data restoration

Continuously and automatically back up your changes, restore a specific version of your company, and view version history.**

24/7 support & training

QuickBooks Priority Circle support and access to special training resources.

Revenue recognition

Stay consistent, compliant, and credible with automated revenue recognition.

Bookkeeping support

- Add $50 per month

NEW

NEW

Get help from our bookkeepers when you need it. They’ll provide guidance, answer your questions, and teach you how to do tasks in QuickBooks, so you can stay on track for tax time and run your business with confidence.

QuickBooks-certified bookkeepers can help you with:

- Automating QuickBooks based on your business needs

- Categorizing transactions and reconciling accounts correctly

- Reviewing key business reports

- Ensuring you stay on track for tax time

Add $50/month

QUICKBOOKS LIVE

Real experts. Real confidence.

All QuickBooks Online plans come with a one-time Guided Setup with an expert and customer support.

Need more help? QuickBooks Live helps you stay organized and be ready for tax time with:

- Live Assisted Bookkeeping

- Live Full-Service Bookkeeping

Ready to get started?

Or call 1-800-365-9606

Add sales tax to invoices

Easily add sales tax to invoices. You can include sales tax on your invoice templates, or you can add sales tax to individual invoices. When you add sales tax to an invoice, the calculations and tracking are done automatically for you.

Automatic sales tax tracking

Sales tax is a fee charged by government agencies, and in order to collect it, your customers pay the tax to you and then you are required to pass it on by making tax payments. Because QuickBooks automatically records your transactions, it keeps track of how much sales tax you need to send to the tax agencies.

Collect sales tax for multiple tax agencies

You may need to pay sales tax to multiple tax agencies, such as your city, your county, and your state. In QuickBooks, you can use a combined rate to charge your customer one sales tax amount, and then QuickBooks will split out the appropriate amounts for each tax agency.

Easily accessible reports

The Sales Tax Liability Report (STLR) shows a summary of sales tax you’ve collected and owe to the tax agencies. It gives you the total taxable sales, total nontaxable sales, tax rate, tax collected, and sales tax payable – all broken down by tax agency.

Frequently asked questions

Join over 7 million customers globally and find the QuickBooks plan that works for you4

Call Sales: 1-800-285-4854