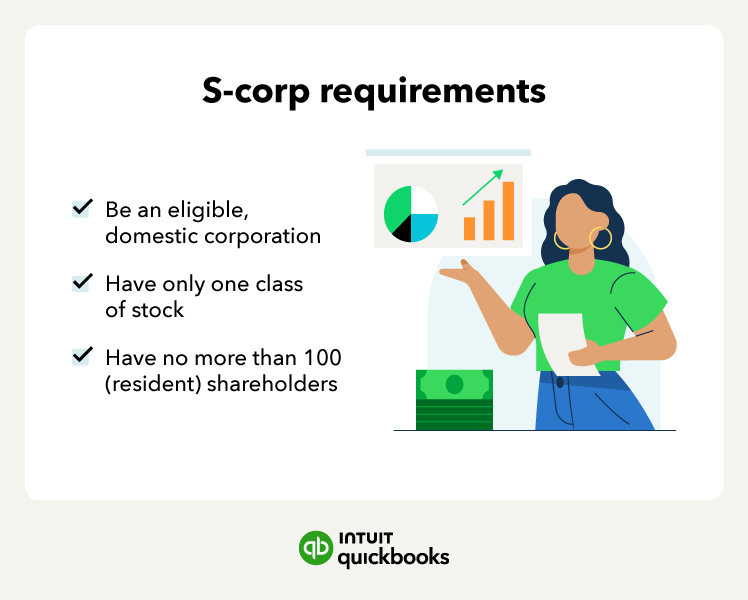

Advantages of electing S-corp status

The tax advantages and liability protection offered by S-corp status make it an attractive option for small business owners and solopreneurs alike. Electing S-corp status has two major pros for shareholders:

- S-corp self-employment tax: For S-corp owners who also work for the company, part of your income can be classified as salary, subject to payroll taxes, while the remaining profits are distributed as dividends and may not be subject to self-employment tax.

- Pass-through taxation: Refers to the taxation method where business profits "pass-through" the S-corp and are directly taxed on the owners' individual income tax returns, allowing S-corporation profits and losses to be reported on shareholders' personal tax returns, avoiding double taxation.

Although an S-corp has unique taxation requirements, there are payroll services for S corporations available. If these tax write-off wins sound advantageous for your business, it’s time to consider if an S-corp is right for you.

How to know if an S-corp is right for you

Determining whether an S-corp is the right choice for your business requires careful consideration. Here are some key points to help guide your decision:

- When to elect to be an LLC: Opting for an LLC may be more suitable if you prioritize simplicity or are anticipating substantial growth with numerous shareholders. As your business grows, considering S-corp taxation is a natural next step since it allows owners to be employees and take home a salary subject to payroll taxes.

- When to elect to be a C-corp: Choosing a C corporation might be preferable if you intend to attract external investors and raise substantial capital for your business. Select this option if you foresee the need for multiple classes of stock, as well as more complex ownership and management structures.

Regardless of whether an S-corp, is the right status for your business, consult with your financial advisor and tax professionals before electing a new business status.

Start your business with confidence

As you consider learning how to start an S-corp, remember that your business can only qualify for advantages like the pass-through tax if you adhere to the requirements above. In order to do so, you may need the help of accounting software.

From registering your business to electing an LLC or C-corp status, staying organized every step ofthe way is vital to the success as an S-corp. To keep your status valid, maintain adherence to the S-corp guidelines.