Not every project delivers the same value to your business. While new work can drive revenue, some projects may require more time, effort and resources than they generate in return. Understanding the true profitability of each project can help businesses make more informed decisions and improve overall performance.

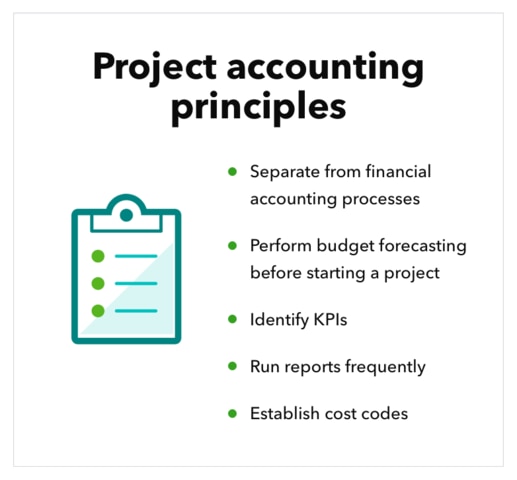

Project accounting is a method of tracking the costs, revenue and profitability of individual projects. By monitoring financial performance on a project-by-project basis, businesses can identify which projects add value, where margins can be improved, and how resources can be allocated more effectively. This guide explores the key principles of project accounting and how it can benefit small and mid-size businesses.