Within each category, line items will distinguish the specific accounts. Each line item represents an account within each category.

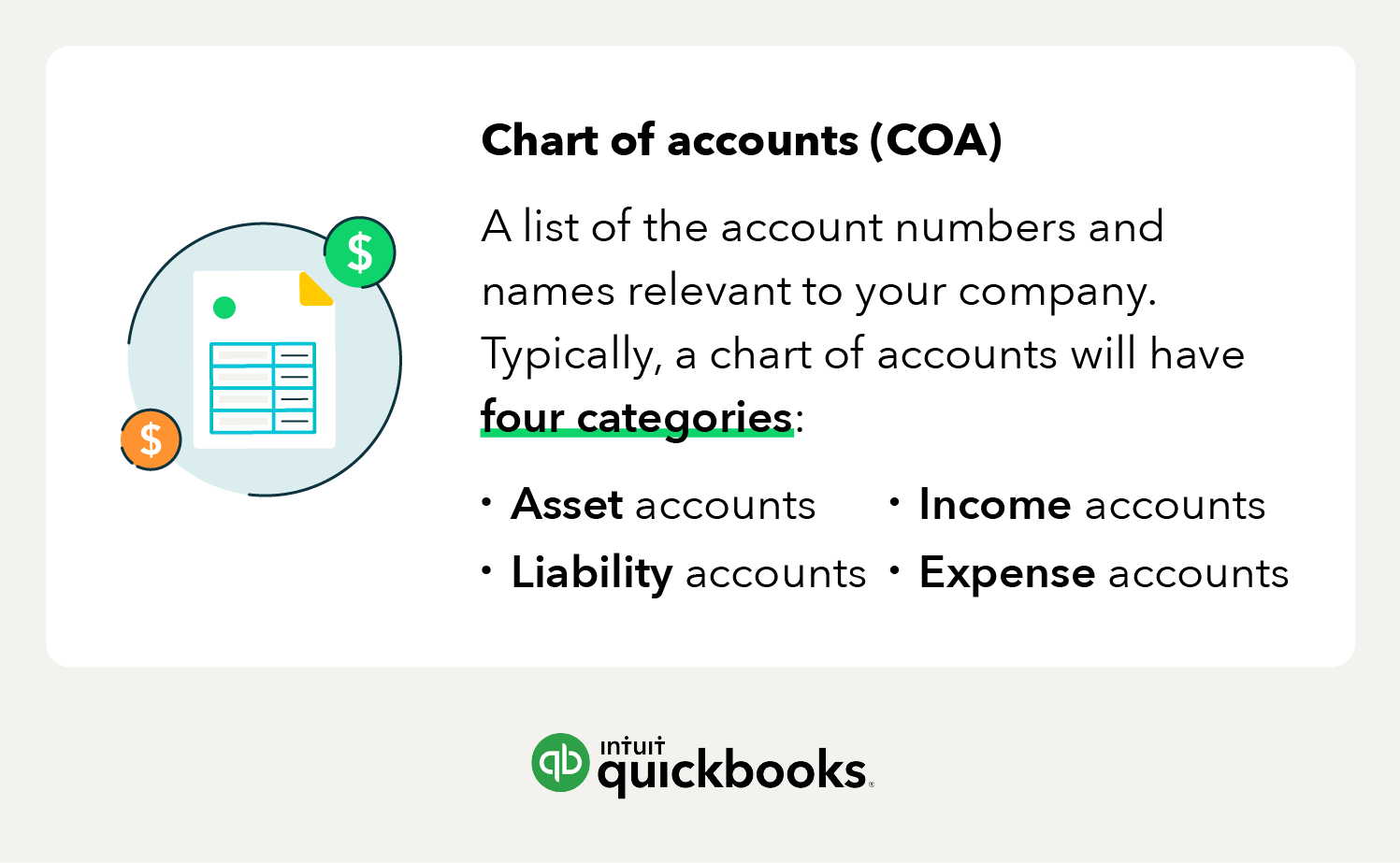

Here’s a brief overview of the four accounts that are commonly associated with the chart of accounts in Australia:

Asset Accounts

Your asset accounts will include anything you own that has value, such as:

- Buildings

- Land

- Equipment

- Vehicles

- Valuables

- Inventory

- Cash

- Accounts receivable

- Notes receivable

Unfortunately, your assets may not look as pretty on your chart of accounts as they would on a real estate agent’s website. Asset accounts can be confusing because they not only track what you paid for the property, but they also follow things like depreciation.

Asset accounts also include things that are liquid, such as your checking account and other bank accounts. Additional asset accounts could be things like accounts receivable – or your unpaid invoices and notes receivable. The chart of accounts streamlines various asset accounts by organising them into line items so that you can track multiple components easily.

Liability Accounts

Liability accounts include things like:

- Bank loans

- Mortgages

- Personal loans

- Promissory notes

- Income taxes payable

- Payroll taxes

- Credit card balances

- Bills

When entering a loan into your company’s chart, you should make sure that you only include the amount of the loan. Log just the principal amount and forgo the interest owed. When you make each monthly payment and enter the payment in your accounting system, you will split the payment into an amount subtracted from what you owe, and an amount of interest paid, which will go into an expense account.

Income Accounts

Income tends to be the category that business owners underuse the most. Here are the most common types of revenue or income accounts:

- Sales income

- Rental income

- Dividend income

- Contra income

Most businesses start with broad income categories like ‘sales’ and ‘services’, but separating income types in your chart of accounts provides better financial insights.

Instead of lumping all income into one account, classify it by source – such as ‘income from food sold’ and ‘income from books sold’ – to track profitability more effectively. This helps identify high-earning activities, manage cash flow, and assess costs like the cost of goods sold (COGS). Be sure to include all revenue sources, including interest income.

Expense Accounts

Expense accounts represent any money that you’ve spent. For instance, if you rent, the money moves from your cash account to the rent expense account. Expense accounts allow you to keep track of money that you no longer have.

Below are more examples of expense accounts your business may use:

- Cost of sales

- Advertising expense

- Interest expense

- Depreciation expense

- Salaries or wages

- Interest expense

- Depreciation expense

It’s also a good idea to break up expenses into separate accounts. For instance, if you ship a lot of products, you may want to track your costs from different shipping carriers separately. Within each line account, you can create sub-categories for the various expenses associated with each carrier.