Turn on suggestions

Auto-suggest helps you quickly narrow down your search results by suggesting possible matches as you type.

Showing results for

Hi,

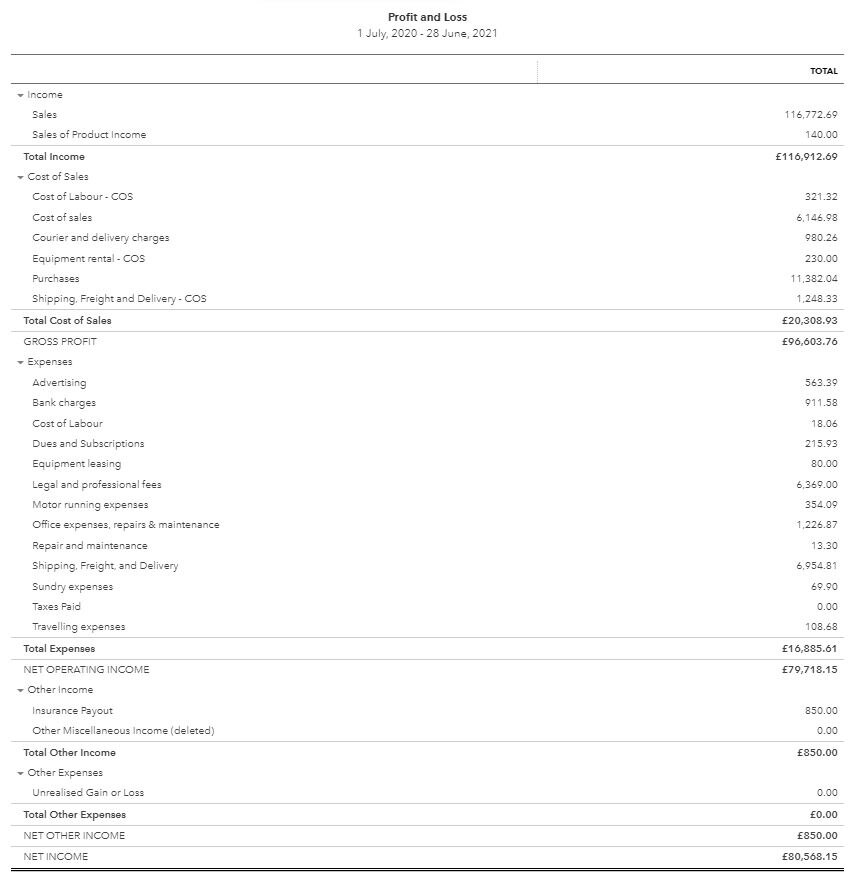

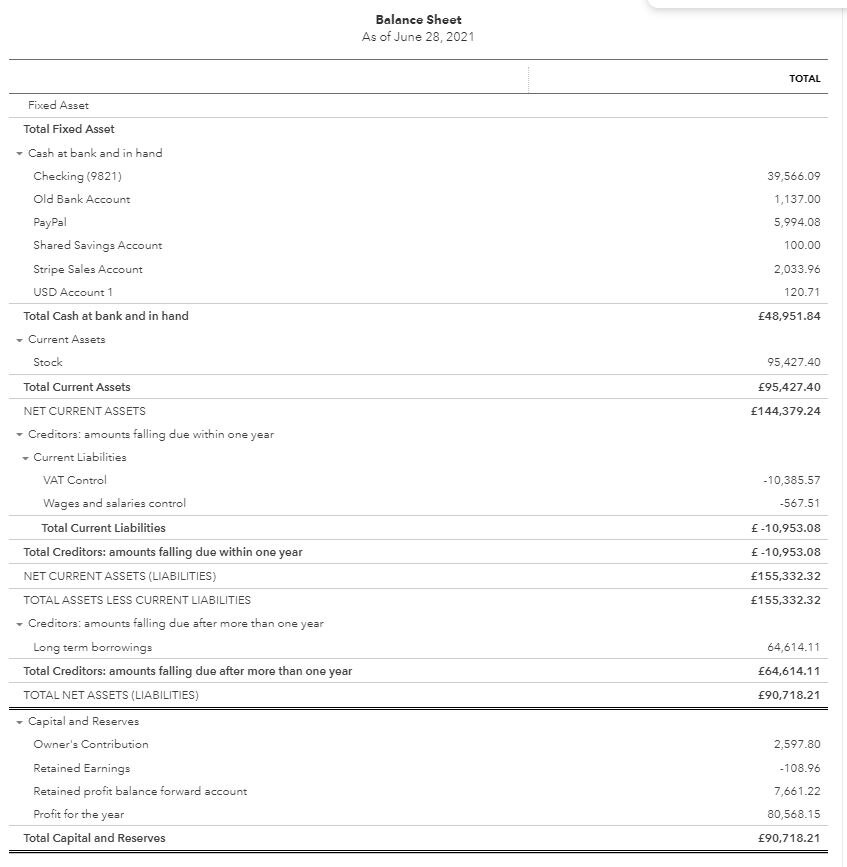

I ran into an issue while doing company accounts. Since the start of the company last year, the company bought stock to resell for £94,000. This includes £50,000 worth that just arrived last week. Anything before this was sold. I put all of their stock purchases into the current assets - stock account to show on the balance sheet. However, now, the price that they have paid for the stock is not on the profit and loss account as a purchase expense, only stock, which skyrocketed the net profit for the end of the year.

I need to decrease the stock by about £48,000 that has already been sold and show the purchase expenses on the profit and loss account. I put all of the sales in the income - sales account and cost of sales into cost of sales accounts.

How can I have the stock purchased as an expense on the profit and loss account and the remaining stock on the balance sheet as available inventory to be sold?

For extra information, now the stock account is at £94,000, and because these stock purchases are not shown on the profit and loss account, the net profit is £80,000.

Attach images for reference.

Any help would be greatly appriciated.

Thank you.

Solved! Go to Solution.

Hi FauxHydon,

Thank you for reaching out to the Commmunity!

Normally, you would record your inventory purchases after selling them, but in this case, it looks like the sale happened first before having those inventories. Since some of the transactions happened last year, I would recommend reaching out to an accountant. That way, they can help you adjust your books.

If your accountant has instructions that you find challenging to do in QuickBooks, just comment below. We're just here to help you again.

Hi FauxHydon,

Thank you for reaching out to the Commmunity!

Normally, you would record your inventory purchases after selling them, but in this case, it looks like the sale happened first before having those inventories. Since some of the transactions happened last year, I would recommend reaching out to an accountant. That way, they can help you adjust your books.

If your accountant has instructions that you find challenging to do in QuickBooks, just comment below. We're just here to help you again.

You have clicked a link to a site outside of the QuickBooks or ProFile Communities. By clicking "Continue", you will leave the community and be taken to that site instead.

{kind=link}

{kind=link}