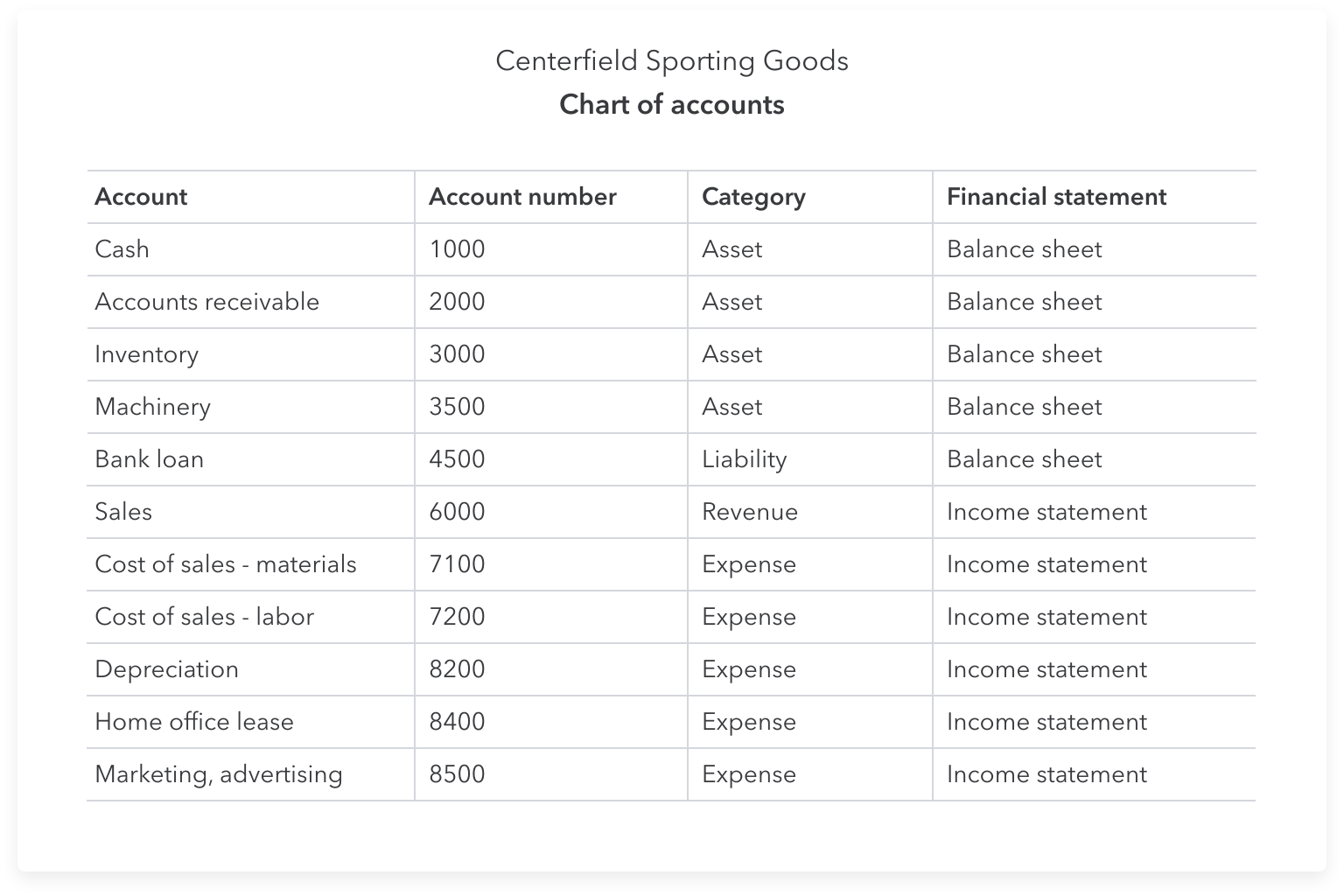

Starting a business is an exciting undertaking, but it can come with challenges. Your initial focus is likely to be on delivering a great product/service and finding customers—which means that administrative tasks such as bookkeeping can take a back seat.

However, good bookkeeping is an essential part of business growth and success. Many small business owners use an Excel accounting template when they get started, which is a useful tool in the early stages of business.

In this guide, we’ll cover everything you need to know about Excel and accounting, and provide tips for upgrading your accounting system as your business expands.