Direct Labour

Hiking boot production also requires labour costs. Outdoor Manufacturing pays workers to operate cutting and sewing machines, and to stitch some portions of each boot by hand.

Based on industry experience, the management knows how many hours of labour costs are required to produce a boot. The hours multiplied by the hourly pay rate equals the direct labour costs per boot. Outdoor Manufacturing knows the direct labour costs required to produce 1,000 boots.

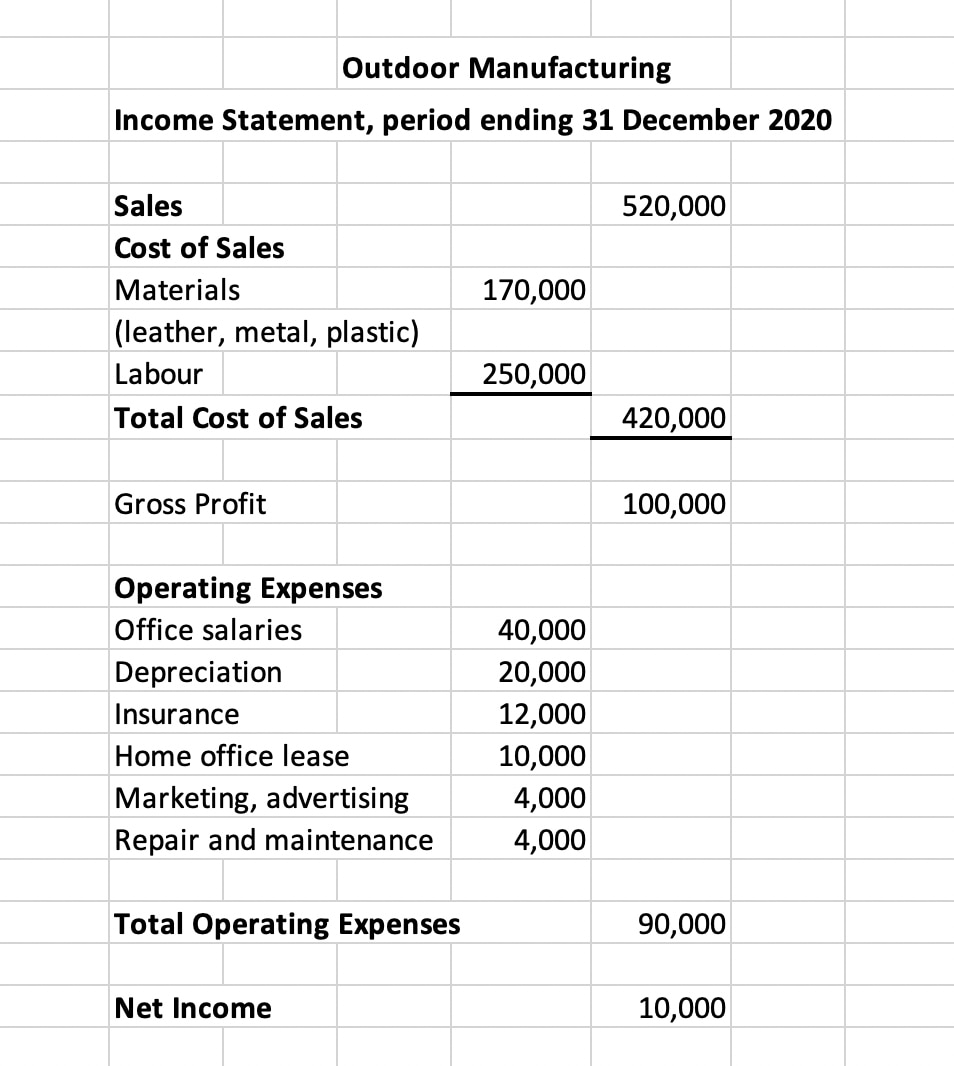

The 2020 income statement reports that Outdoor Manufacturing incurred $170,000 in direct material costs and $250,000 in direct labour costs.

Allocation of Overhead

Outdoor Manufacturing’s overhead costs are posted to the operating expenses. The only way to recover the overhead costs is to sell an item to a customer, so each dollar of overhead must be allocated to a product or service.

Overhead costs are allocated based on a level of activity. Here are some common examples:

Tradespeople (like carpenters, plumbers and tree service firms) incur travel costs, as they travel to each client’s location. The more kilometres driven, the more repair and maintenance costs incurred on the vehicles. A plumber may allocate overhead costs based on the kilometres driven. If serving a customer requires driving 30 kilometres, the plumber adds 10 cents per kilometre to cover the vehicle repair and maintenance costs.

Overhead costs are frequently allocated using machine hours incurred or labour hours required, or simply using the number of units produced.

Fixed Costs vs Variable Costs

Managers need to know why a particular cost is being incurred. One way to understand costs is to determine if the expense is fixed or variable.

Direct costs, such as materials and labour, are typically costs that vary with production. However, if a customer contract requires you to hire an outside firm to assess quality control, that one-time cost may be considered a fixed direct cost.

The cost paid to an office security company is a fixed overhead cost. You need the firm to protect the company’s assets, regardless of how much you produce or sell. On the other hand, the hourly rate paid to repair the company’s machinery is a variable overhead cost.

Inventoriable costs are not immediately assigned to the COGS account.

Inventoriable Costs

Inventoriable costs are defined as all costs to prepare an inventory item for sale. This balance includes the amount paid for the inventory item and shipping costs. If a retailer must build shelving or incur other costs to display the inventory, the expenses are inventoriable costs.

The cost to train people to use a product is also included in this category. The cost to train employees to use IT is a good example.

When the inventory item is sold, the inventoriable costs are reclassified to the COGS account. A retailer may have thousands or even millions of dollars in inventoriable costs that are not yet expensed.