“Marginal cost” is the extra cost a business incurs when it produces an additional unit of a product. Also known as the “marginal cost of production”, this includes all the additional expenses – such as labour and materials – directly related to making that extra unit.

In this article, we’ll cover everything you need to know about marginal cost, its meaning, how to calculate it accurately, and how to use it.

To jump ahead to a section, click the links below:

- What is a marginal cost?

- Benefits of knowing your marginal costs

- What is an example of a marginal cost?

- How to calculate marginal costs

- The marginal cost formula

- How production costs affect marginal costs

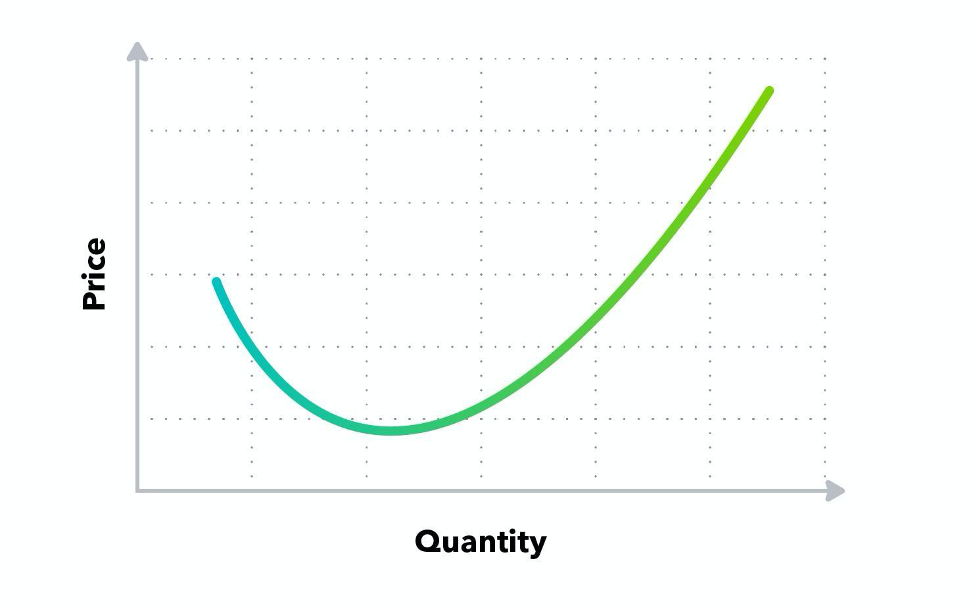

- Understanding the marginal cost curve

- Contribution in marginal costing

- What is marginal revenue, and why is it important?

- Marginal cost vs variable cost: what’s the difference?

- The relationship between marginal cost and average cost

- How to use marginal costs in your business