How to calculate the bad debt expense

Calculating your bad debts is an important part of business accounting principles. Not only does it parse out which invoices are collectible and uncollectible, but it also helps you generate accurate financial statements.

There are two ways you can calculate bad debt expenses for your business:

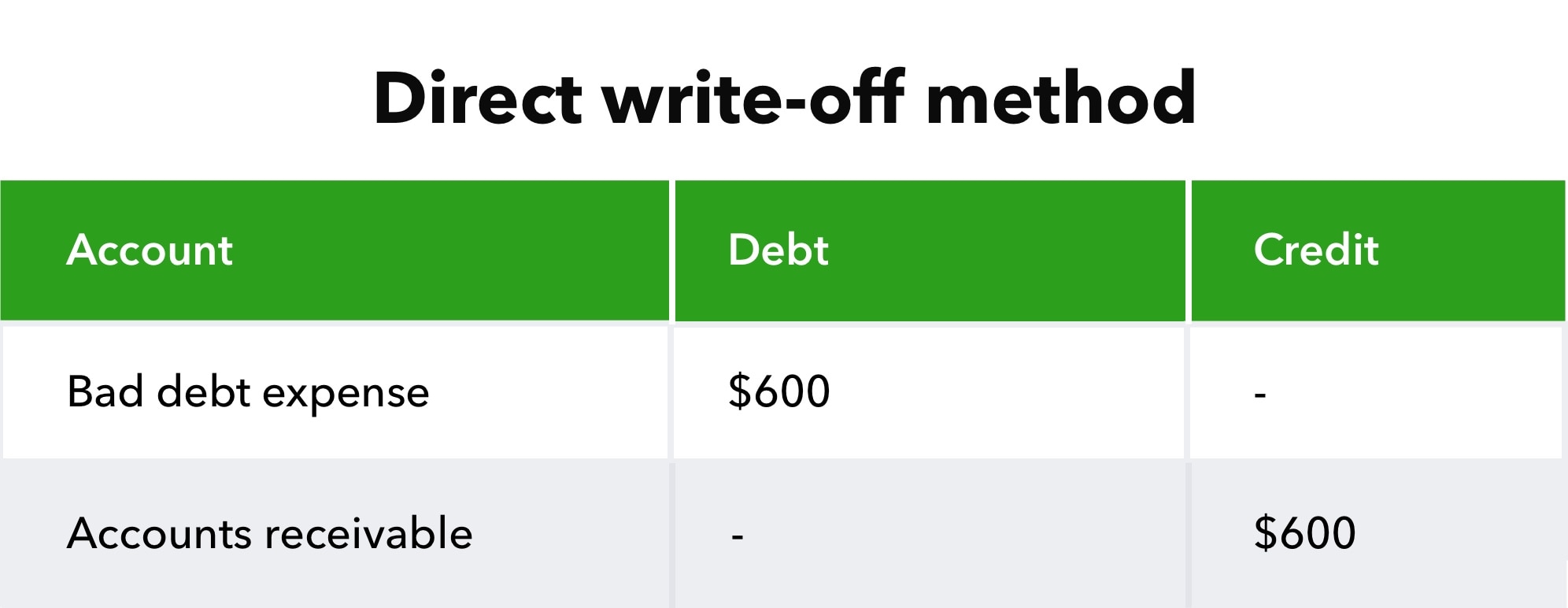

1. Direct write-off method: If most of your customers fulfil their credit payments, and you don’t have many bad debts, you may decide to write them off individually. It may be time to write off bad debts after an invoice has long surpassed its deadline and you’ve taken several steps to try to collect the outstanding balance.

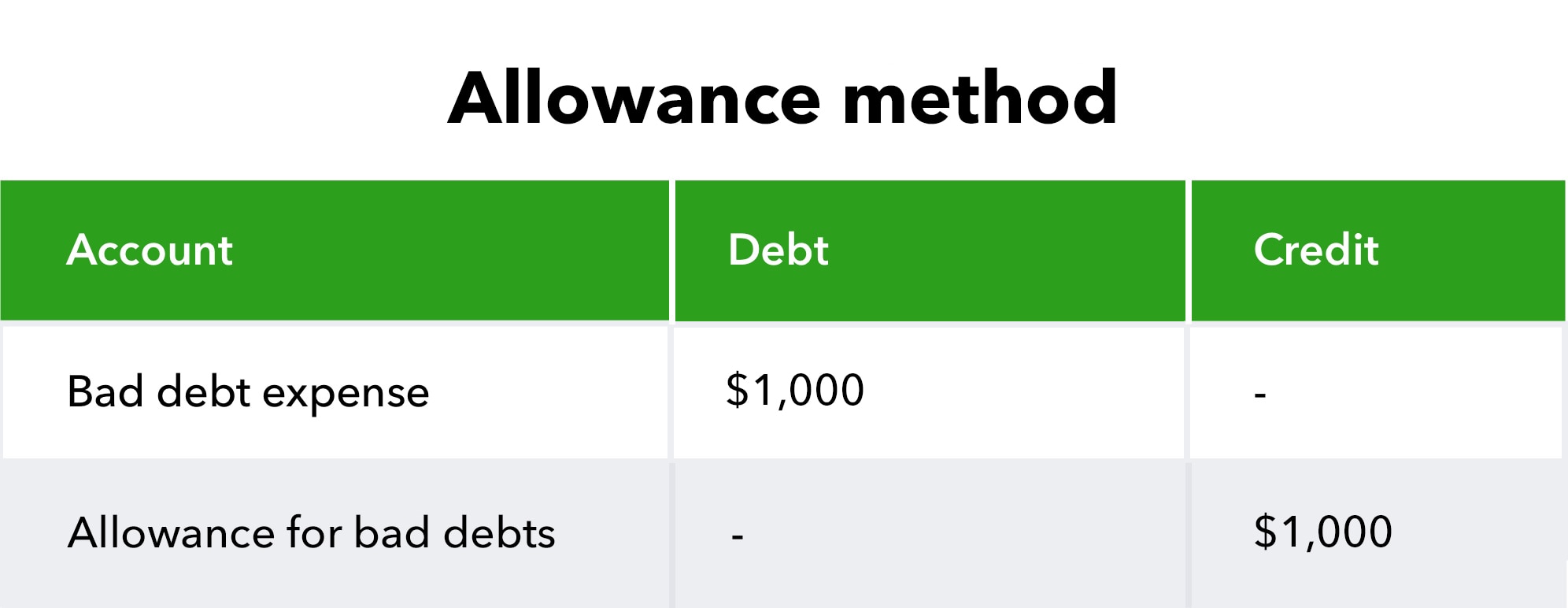

2. Allowance method: Businesses that conduct most sales on credit are usually more likely to encounter bad debts. In this case, it may be helpful to plan ahead for uncollectible payments using the allowance method. Also called the allowance for doubtful accounts, this option preemptively labels a certain portion of your total credit sales as doubtful debts. This way, you can plan ahead for bad debts and budget accordingly.

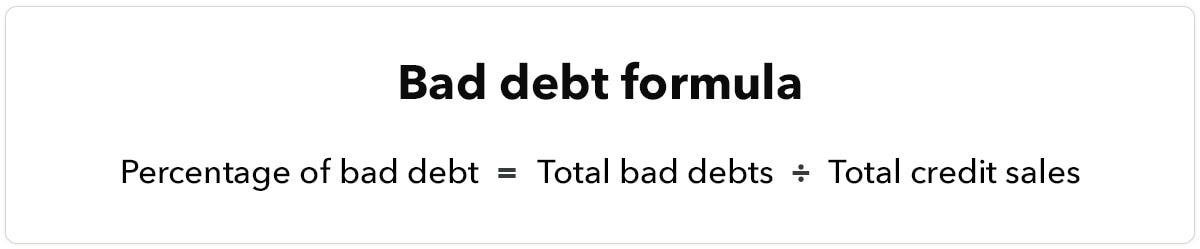

To estimate bad debts using the allowance method, you can use the bad debt formula. The formula uses historical data from previous bad debts to calculate your percentage of bad debts based on your total credit sales in a given accounting period.

Percentage of bad debt = total bad debts / total credit sales