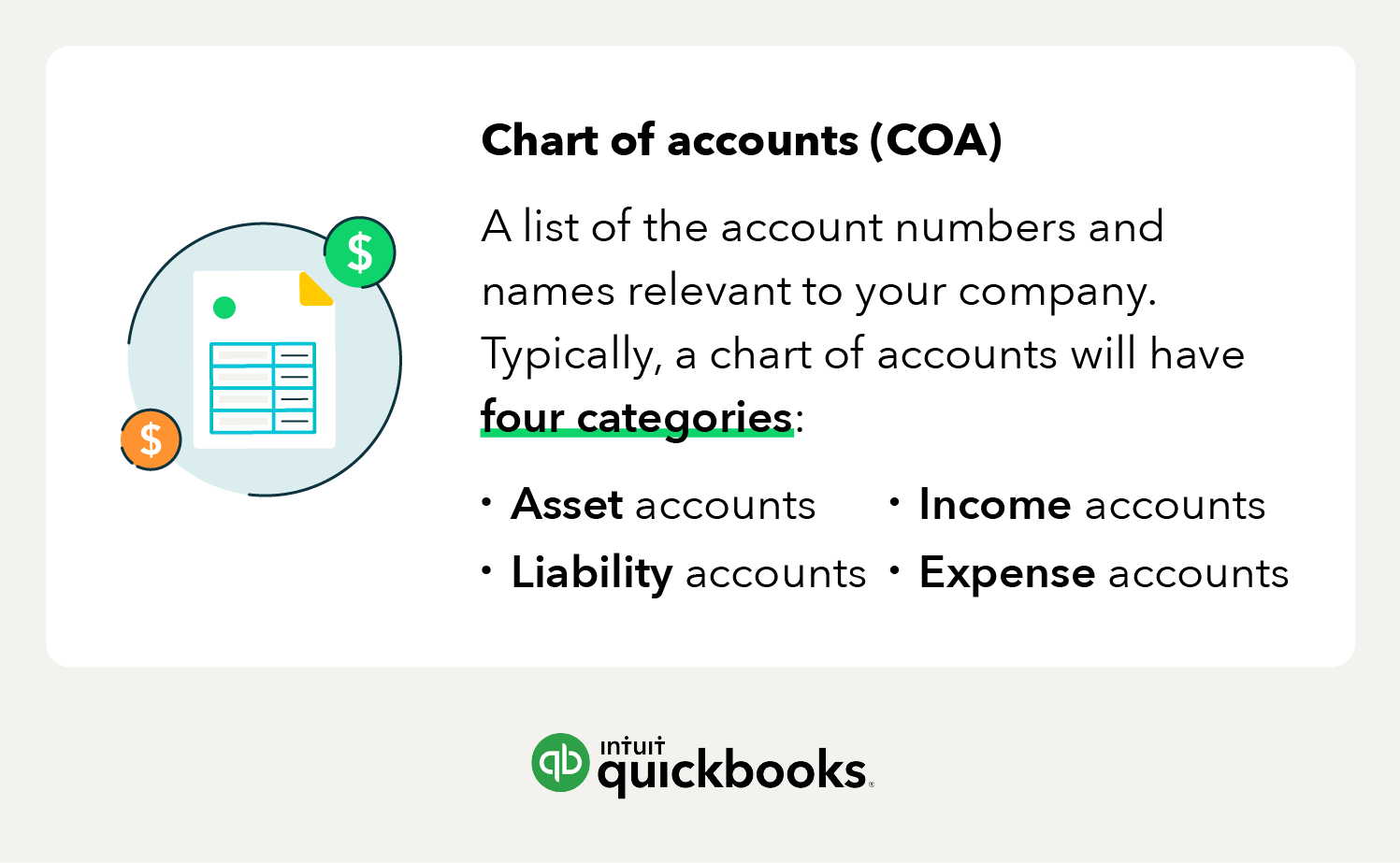

The four main account types in a chart of accounts list

1. Asset accounts

Your asset accounts could include anything you own that has value, such as:

- Buildings

- Land

- Equipment

- Vehicles

- Valuables

- Inventory

- Cash

- Accounts receivable

- Notes receivable

2. Liability accounts

Your liability accounts include things like:

- Accounts payable or bills

- Payroll taxes

- Income taxes payable

- Bank loans

- Credit card balances

- Mortgages

- Deferred tax liabilities

- Personal loans

Current liabilities are classified as any outstanding payments that are due within the year, while non-current or long-term liabilities are payments due more than a year from the date of the report.

When entering a loan into your company’s chart, follow these tips:

- Log just the principal loan amount and exclude the interest owed.

- When you make each monthly payment, enter the payment in your accounting system.

- Split the payment into an amount subtracted from what you owe, and an amount of interest paid, which should go into an expense account.

3. Income accounts

Income tends to be the category that business owners underutilise the most. Below are the most common types of revenue or income accounts:

- Sales income

- Rental income

- Dividend income

- Contra income

Most new owners start with one or two broad categories, like “sales” and “services.” While some types of income are easy and cheap to generate, others require considerable effort, time, and expense. It may make sense to create separate line items in your chart of accounts for different types of income.

4. Expense accounts

Expense accounts represent any money that you’ve spent. For instance, if you rent, the money moves from your cash account to the rent expense account. Expense accounts allow you to keep track of money that you no longer have.

Below are more examples of expense accounts to your business may use:

- Cost of sales

- Advertising expense

- Interest expense

- Depreciation expense

- Salaries or wages

- Interest expense

- Depreciation expense

It’s also a good idea to break up expenses into separate accounts. For instance, if you ship a lot of products, you may want to track your costs from different shipping carriers separately. Within each line account, you can create sub-categories for the various expenses associated with each carrier.