Hey Exclusive12,

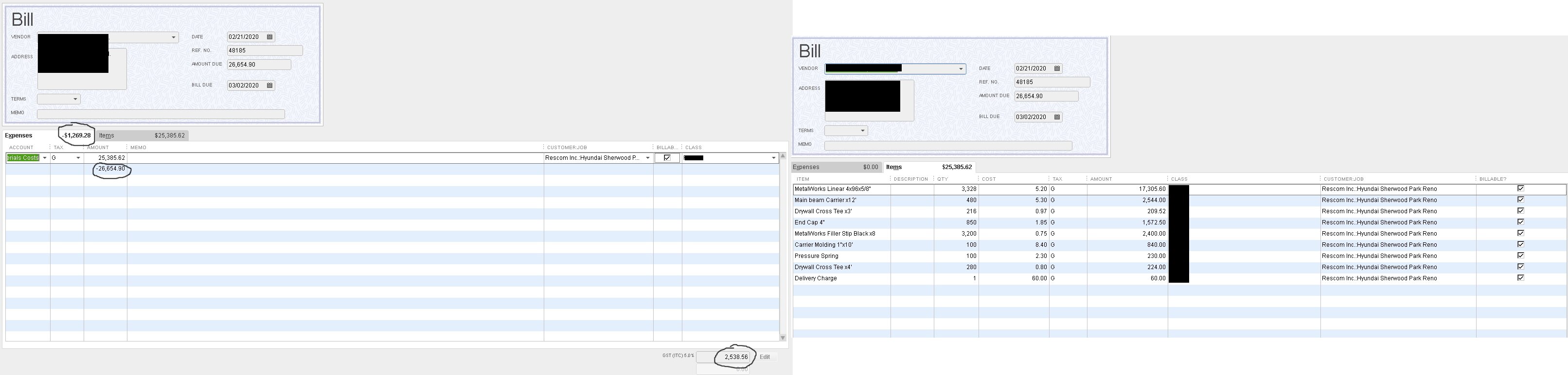

It's awesome to see you're taking full advantage of the powerful options available in QuickBooks to elevate your accounting. The system includes advanced inventory tracking, so you can rest assured you'll always know your cost of goods sold. The intuitive jobs management makes it simple to organize your income and expenses based on various projects, unlocking additional insight into your business' profitability. Your description was not too confusing at all, and the image helped a lot. I'll be happy to help make sense of this.

The behaviour you've described is perfectly normal, as inventory items incur costs of goods sold once you create an invoice for them. Entering a purchase in the Items section is similar to recording a transfer between two asset accounts. Instead of spending money, think of it as converting money into inventory. Once that inventory is sold, the asset account gets credited by the cost of goods sold automatically to keep everything balanced. If you want the expense to be recorded on the bill date, make sure you're selecting a non-inventory item or entering the information in the Expenses tab.

The reason you're seeing your taxes doubled is because there is a tax rate selected on the positive amount, but not the negative amount. Selecting the same rate on both amounts would cause the taxes to cancel each other out. I don't recommend this approach, as the expense would appear as duplicate in your Profit and Loss by Job report once the item is sold.

Let me know if this helps!

{kind=link}