Cloud accounting

The future of strategic client advisory – Intuit Intelligence has arrived

Simple, smart accounting software - no commitment, cancel anytime

TAX AND PENSIONS

Cash and accrual accounting are like sibling rivals in the accounting realm—one clashes with the other, but you can definitely see the resemblance. Even if you don’t handle your own financial reporting, it’s vital to know how each one works so you can choose the best bookkeeping practices for your business.

Cash accounting records income and expenses as they are billed and paid. With accrual accounting, you record income and expenses as they are billed and earned.

Why should you choose one over the other? We’ll explain the basics of the cash accounting and accrual accounting methods, as well as the pros and cons of each so that you can make an informed decision.

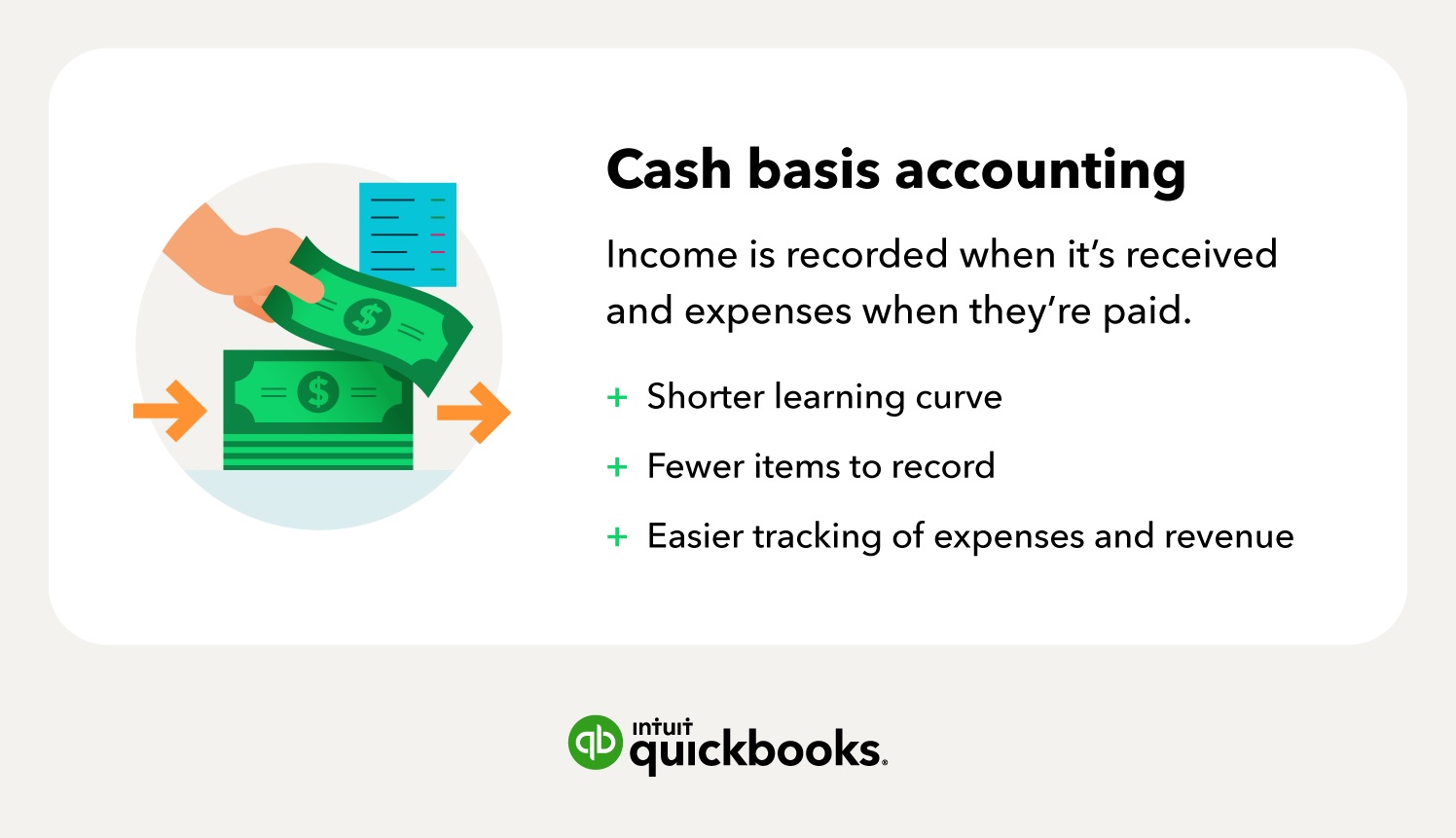

Let’s begin with cash basis accounting. With this method, you record income as it’s received and expenses as they’re paid. Cash basis accounting only records your expenses when money leaves your account to pay suppliers, vendors, and other third parties.

In other words, if you have a small stationery business that purchased paper supplies on credit in June, but didn’t actually pay the bill until July, you would record those supplies as a July expense.

It’s important to note that this method does not take into account any accounts receivable or accounts payable. This is because it only applies to payments from clients—in the form of cash, cheques, credit card receipts, or gross receipts—when payment is received.

Because of its simplicity, many small businesses and sole proprietors use the cash basis method as their primary method of accounting.

Some of the benefits include:

Shorter learning curve

Fewer items to record

Easier tracking of expenses and revenue

If you invoice a client for £1,000 on the 1st of March and receive payment on the 15th of April, you would record the income as received for the month of April, since that’s when you actually had the money in hand. So the breakdown looks like this:

The invoice is sent for £1,000 in March

You do nothing in March

You receive payment in April

You record the income in April

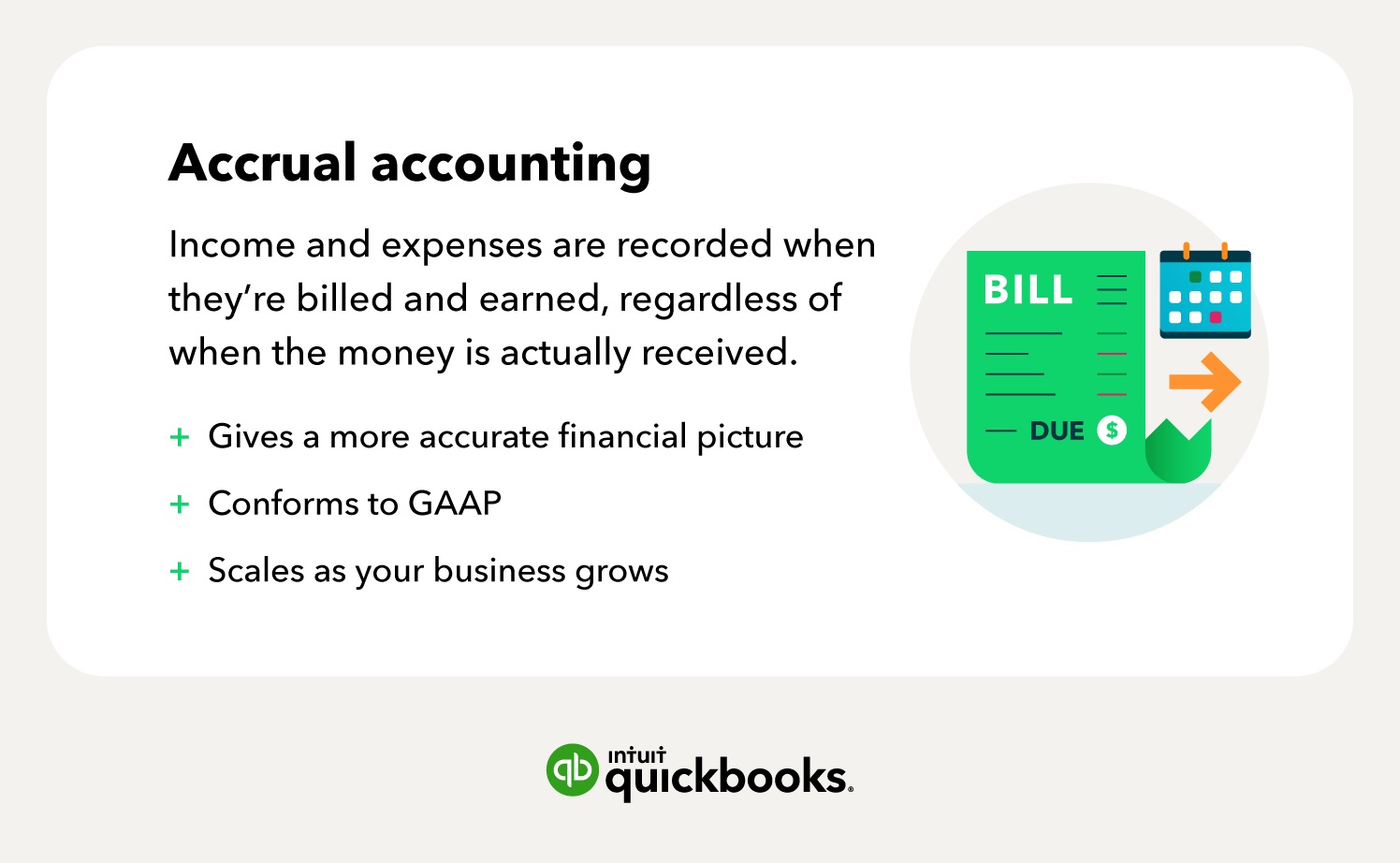

With the accrual accounting method, income and expenses are recorded when they’re billed and earned, regardless of when the money is actually received. In the UK, companies need to submit statutory accounts under UK GAAP or FRS must use the accrual method.

Using the example from above, if a small business bills a client £1,000 on the 1st of March, you would record that £1,000 as income in March’s bookkeeping—even if the funds didn’t clear your account until the 15th of April.

The invoice is sent for £1,000 in March

You record revenue in March

The same holds true for accrued expenses. In this case, if your small stationery business buys paper supplies on a credit card in June, but doesn’t actually pay that bill until July, you would still record that as a June expense. Let’s break this down:

You bought paper supplies in June

You record the expense in June

From 6 April 2024, if you're a sole trader or partner, the default method for calculating income and expenses for your Self Assessment tax return will be the cash basis. This means you'll need to start keeping records using this method for the 2024 to 2025 tax year, unless you either opt for traditional accounting or are ineligible for the cash basis.

Additionally, you can now offset losses against other taxable income, and if you run multiple businesses, you can choose to use either cash basis or traditional accounting for each one. If you prefer traditional accounting, you’ll need to opt out of the cash basis when filing your Self Assessment tax return by ticking the appropriate box.

Keep digital records, submit quarterly updates to HMRC, and finalise your Income Tax at the end of your accounting period with Intuit QuickBooks.

Explore plans & pricing

Accrual accounting is the winner if you’re looking solely at popularity, as it’s the most widely used as well as the most accurate when it comes to portraying a holistic view of a business's financial health. Cash basis accounting is still a popular option, however, due to the simplicity of the overall process.

Unlike cash basis accounting, which provides a clear short-term vision of a business's financial situation, accrual basis accounting gives you a more long-term view of how your business is faring.

This is because accrual accounting gives an accurate picture of how much money you earned and spent within a specified time period, providing a clearer gauge of when business speeds up and slows down over the course of a business quarter or a full year.

Businesses using accrual accounting may find it easier to comply with tax regulations as it gives a more complete financial picture throughout the year. Accrual accounting is required for companies and for those required to comply with the Financial Reporting Standards (FRS), which is the framework most UK businesses follow.

Creates a more accurate financial picture: It can give small business owners a more realistic idea of income and accrued expenses during a certain period of time. This can provide you (and your accountant) with a better overall understanding of consumer spending habits and allow you to plan better for peak months of operation.

Conforms to UK accounting standards (FRS): Because the accrual method conforms to FRS, it is required by UK companies. Smaller businesses may choose this method to provide a more accurate financial overview.

Scales with your business: You may not be there now, but in a few short years you could change your business structre, pushing you within the requirements of cash basis accounting. If you already use the accrual accounting method, there’s no need to change—it simply grows with you.

More resource-intensive: Many small business owners view it as more complicated and expensive to implement due to complexity and extra paperwork. Since a business records revenues before they actually receive cash, the cash flow has to be tracked separately to ensure you can cover bills from month to month.

Inaccurate short-term view: The cash method gives you a better picture of the funds in your bank account. If you don’t have careful bookkeeping practices, the accrual accounting method could be financially disabling for a small business owner. Your books could show a large amount of revenue when your bank account is completely empty.

The cash method of accounting certainly has its benefits, including ease of use and improved cash flow. While the cash basis method of accounting is definitely the simpler option of the two most common accounting methods, it has its drawbacks as well.

Simplified, familiar process: Cash basis accounting is a simplified bookkeeping process that is similar to how you might track your personal finances. It’s easy to track money as it moves in and out of your bank accounts because there’s no need to record receivables or payables.

Income taxes: For tax purposes, you don’t have to pay taxes on any money that has not yet been received. For instance, if you invoice a client or customer for £1,000 in October and don’t get paid until January, you won’t have to pay taxes on the income until January the following tax year. This is known as paying tax on a 'receipts basis,' which allows businesses to pay tax only on what they’ve received. For individuals and extremely small businesses, this can be crucial to keeping your business afloat when cash flow is restricted.

Inaccurate financial picture: Since it doesn’t account for all incoming revenue or outgoing expenses, the cash accounting method can lead you to believe you’re having a very high cash flow month when in actuality, it’s a result of a previous month’s work.

No accounts receivable or accounts payable records: Because the method is so simple,there are no records of accounts receivable or accounts payable, which can create difficulties when your business does not receive immediate payment or has outstanding bills.

Doesn’t conform to FRS: If your business were to grow larger than the limits set for cash basis accounting, you would need to update your accounting practices to the accrual method to comply with FRS and other regulatory requirements.

For small businesses that do business primarily through cash transactions and do not maintain large inventories of products, the cash accounting method can be a convenient and reliable way to keep tabs on revenue and expenses without the need for a great deal of bookkeeping.

However, for the most accurate and updated accounting view of your financial health, accrual accounting might be the better choice. There are also some other factors to keep in mind.

Depending on your industry and the complexity of your books, one accounting method may be more sustainable than the other. For example, a multi-national company with multiple accounts, hundreds of employees, and various limited companies as subsidiaries, it will probably want to stay away from cash basis accounting because it won’t give the company the big picture view it’s looking for when it comes to financials on the income statement, balance sheet or cash flow statement.

Having a publicly-traded company or one that may go public is another stipulation of accounting guidelines. Publicly traded companies have a duty to report an accurate view of their financial well-being to shareholders. The only method for this is the accrual system of accounting.

Cash basis accounting is an option for small businesses, particularly sole traders and partnerships. This method allows you to record income and expenses when the money actually changes hands, making it simpler to manage cash flow and avoid paying tax on money you haven't yet received. However, it may not be suitable if you hold large amounts of stock or need a more detailed view of your finances.

If you're unsure whether cash basis accounting is right for your business, accounting software like QuickBooks can help simplify your bookkeeping and give you better insight into your tax situation. QuickBooks lets you easily switch between cash and accrual accounting, making it easier to stay on top of your financials and Self Assessment returns.

Ready to streamline your tax return preparation? Try QuickBooks today with a free 1 month trial.

Before moving along through your small business accounting checklist, understanding which accounting method to use is, without a doubt, an imperative decision for your business. That’s not to say it can’t be changed later—only that it’s harder to switch once you get comfortable with one way or the other. Accounting software and tools like QuickBooks can help with either method, with virtual accountants available to help you every step of the way.

Bottom line, whether you choose cash or accrual accounting, remember to understand both options and stay within compliance with UK accounting regulations.

The information on this website is provided free of charge and is intended to be helpful to a wide range of businesses. Because of its general nature the information cannot be taken as comprehensive and they do not constitute and should never be used as a substitute for legal, accounting, tax or professional advice. We cannot guarantee that the information applies to the individual circumstances of your business. Despite our best efforts it is possible that some information may be out of date. Any reliance you place on information found on this site or linked to on other websites will be at your own risk.

Share:

Subscribe to get our latest insights, promotions, and product releases straight to your inbox.

9.00am - 5.30pm Monday - Friday