Intuit QuickBooks Small Business Index, April 2026

Simple, smart accounting software - no commitment, cancel anytime

TAX AND PENSIONS

From 6 April 2025, the monetary size thresholds for UK companies will rise, altering the determining factors of whether a company is classed as small, medium, or large.

This blog will explore what this change means for each company size and those crossing over into different thresholds. It’ll also discuss the impact on financial aspects for the new tax year, such as reporting requirements, compliance measures, tax planning, and administrative tasks.

Currently, the classification of a company as a micro, small, medium or large enterprise is determined by the company and corporate group thresholds set out in the Companies Act 2006. This classification then determines the reporting, auditing and tax requirements for a company.

The government is increasing these thresholds by 50% from 6 April 2025 to reflect the rising economic inflation and to future-proof the thresholds moving forward.

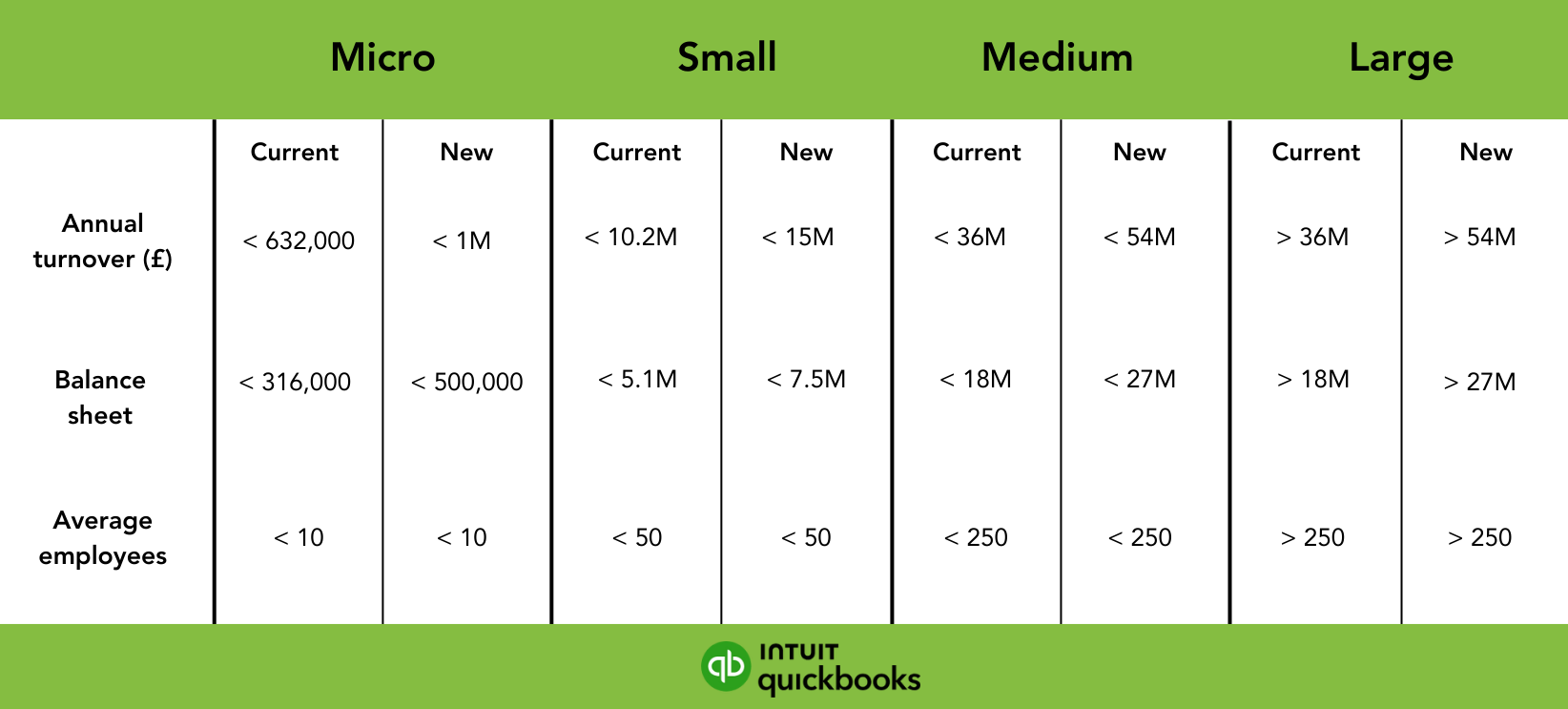

The threshold changes are as follows:

The increased thresholds will also apply to limited liability partnerships (LLPs) via amendments to the regulations that govern them.

The most affected businesses are likely to be small businesses moving to micro businesses. This is important because companies that are able to move down a size category will be entitled to the accompanying reduction in reporting and audit requirements, reducing their compliance costs.

Micro-entities are very small companies. There are a range of factors that classify companies as micro entities. From April 2025, businesses must have two of the below to be considered a micro entity:

10 employees or less

A turnover of £1m or less (from April 2025

£500,000 or less on its balance sheet (from April 2025)

Different sized companies will be impacted differently by these threshold changes, with Small to Micro businesses seeing the largest impact.

Keep digital records, submit quarterly updates to HMRC, and finalise your Income Tax at the end of your accounting period with Intuit QuickBooks.

Explore plans & pricing

For medium businesses moving into the small business threshold or small businesses moving to the micro business threshold, the impact will be significant.

These businesses will be exempt from the requirement to have a statutory audit of their annual accounts, which usually requires a group membership or annual fee, and they will also be exempt from producing an annual Strategic Report.

They will also be able to take advantage of simpler accounting requirements. Those moving to the micro entities regime will additionally be exempt from producing a Directors’ Report.

Those moving from the large to the medium-sized category will be able to take advantage of exemptions from certain Strategic Report requirements, including a statement on how directors have had regard to stakeholder interests known as the Section 172(1) statement.

The changes to the thresholds are in an effort to decrease the UK’s administrative burden, particularly with non-financial reporting; the new regulations also remove any obsolete or overlapping requirements that businesses previously had to report on.

For the purposes of payroll and taxes, a company’s size is determined by its previous financial year and previous tax year. Therefore, the company size threshold changes will have no practical impact on payroll until 6 April 2026 at the earliest.

There are many ways in which a business might want to prepare for the company threshold changes, especially if you know your company will be moving into a smaller or larger threshold as of April 2025.

As a business owner, you should constantly be assessing whether crossing into a new threshold is financially beneficial to your company or not. It is wise to be continuously planning strategically for this crossover so that you are prepared for the changes when they occur.

Reviewing your tax planning and strategies in light of a potential higher tax payment is a wise idea, whilst also leveraging any potential investment reliefs and allowances ahead of crossing thresholds could grant you will put you in the best position when your business crosses that size threshold.

As well as preparing for tax changes, you may also want to prepare for any new changes in compliance or reporting responsibilities to ensure you can find all of the correct documentation ahead of the threshold crossover.

As with any business change, it is good to feel prepared and have all of your documentation gathered and ready for reporting when needed. It is no different for the business size threshold changes — ensure you are well-organised and start looking at how your taxes and reporting may change after April 2025.

The information on this website is provided free of charge and is intended to be helpful to a wide range of businesses. Because of its general nature the information cannot be taken as comprehensive and they do not constitute and should never be used as a substitute for legal, accounting, tax or professional advice. We cannot guarantee that the information applies to the individual circumstances of your business. Despite our best efforts it is possible that some information may be out of date. Any reliance you place on information found on this site or linked to on other websites will be at your own risk.

Share:

Subscribe to get our latest insights, promotions, and product releases straight to your inbox.

9.00am - 5.30pm Monday - Thursday

9.00am - 4.30pm Friday