Intuit QuickBooks Small Business Index, March 2026

Simple, smart accounting software - no commitment, cancel anytime

FINANCE, BUDGETS AND CASHFLOW

Nothing sums up British inflation like the rising price of a Freddo bar.

But what do rising costs mean for small businesses? Inflation can have profound effects on your business decisions, from your pricing strategy to what you pay your employees.

Read on to learn how to protect your business from inflation in the UK.

Inflation is the rise of prices over time, which reduces the value of money. This is why your weekly shop will cost more each year, despite the quality of produce staying the same.

An inflation ‘rate’ describes how quickly costs for bills, products, and services are rising.

In simple terms, inflation happens when there’s more money available than the economy can keep up with. If a lot of money is added to the system, but businesses aren’t producing more goods or services to match, the value of each pound drops and prices rise.

It is influenced by supply and demand – for example, popular goods may cost more. Government borrowing, changing interest rates, and global events also play a part.

Inflation is a concern for small businesses in the UK, and with good reason.

The Bank of England aims to keep inflation at around 2%, but in October 2022 it hit 11%. This was the highest inflation rate in over 40 years, and was caused by a mix of factors:

COVID-19 – it’s been difficult for businesses to meet post-pandemic demand

Brexit – has affected supply chains and made international trade more expensive

War in Ukraine – has pushed up energy prices for businesses and households

Food prices – are affected by supply chains, energy costs and climate change

In October 2024, UK inflation was at 2.3%. Prices are still rising, but more slowly. But what does this mean for businesses in the UK, and how can you tackle rising inflation?

Inflation disproportionately affects small businesses because of the limited resources they have to combat rising costs.

Inflation forces small businesses to use more creativity to stay competitive during rising inflation, as they typically can’t fall back on a cash reserve to get through difficult times.

Here are some common challenges small businesses might face during rising inflation and some strategies for going about them.

Increased costs is one of the drivers for the majority of challenges that come with high inflation.

Higher prices make it more expensive to obtain the necessary resources a business requires to stay profitable - leading to difficult decisions like raising prices and laying off employees.

When you notice operating expenses creeping up, take a hard look at your expenses and see what non-essential costs you can cut. Other considerations in this audit could be diversifying your shipping sources for efficient costs, looking into a lower-cost office space, and categorising costs into essential and non-essential.

If you have the resources, bringing in a financial advisor or an accountant can help in getting the best possible financial advice.

With inflation rising in the UK in recent years, one of the biggest challenges that small businesses face is staying profitable. Small business owners must adjust pricing to stay competitive and profitable over the long term.

While the definition of “profitable” differs from industry to industry, the problem typically stems from a lack of purchasing power, which the majority of industries experience during high inflation.

Many small businesses raised their prices over the last year to keep up with rising inflation. With expenses increasing from all directions, it’s increasingly difficult to find ways to stay profitable during periods of high inflation without raising prices.

When inflation rises, it profoundly affects small business owners and their employees. In periods of high inflation, workers’ take-home pay is lower than it would be in more normal circumstances.

As a result, many workers seek new jobs if their previous employer doesn’t raise their pay to align with rising costs.

In most small businesses, your people are an asset that you can’t cut.

Small businesses may also expand employee benefits alongside larger-than-usual pay increases in an effort to attract and retain workers and slow the pace of rising labour costs.

But, due to inflation, benefits are currently less attractive and important to employees than pay. Some small businesses have had backlash from workers who would prefer to get higher pay increases instead of these benefits.

To curb inflation, governments sometimes increase interest rates in an effort to slow down the economy. While this makes sense in principle, it presents a new set of challenges for small businesses, as many take out loans to afford costly raw materials and finance growth.

With interest rates rising at the rate they are, it’s increasingly more difficult and expensive for small businesses to pay off outstanding loans - on top of affording the necessary operating expenses to keep the lights on.

Keep digital records, submit quarterly updates to HMRC, and finalise your Income Tax at the end of your accounting period with Intuit QuickBooks.

Explore plans & pricing

If your small business relies on loans to finance growth plans, it may be best to wait until the market reaches a more normal state before putting those plans into action.

While start-ups and entrepreneurs can often fall back on venture capital and personal savings, small businesses typically don’t have that luxury and have to rely on grants or loans for growth. The best course of action for small businesses is to dock any growth plans until the market levels out.

Due to supply chain disruptions expedited by rising inflation, small businesses faced the challenge of receiving and affording the necessary raw materials to service customers. In some cases, this led to small businesses adjusting their inventory entirely, in turn causing them to create new internal processes as well.

Making inventory adjustments during periods of high inflation can actually be a positive opportunity for small businesses.

When assessing current inventory costs, look for ways to save money by stripping down to the bare minimum. Sometimes, there’s also the opportunity to source locally rather than paying extreme shipping costs.

While the rising cost of supplies presents an immediate threat to small businesses during periods of high inflation, getting people in the door can often be of equal concern.

Like we said, inflation dramatically affects businesses, but also people. And with most businesses raising their prices to stay competitive, consumers are more hesitant to spend liberally.

Innovative marketing strategies like loyalty programs and promotions can often be what it takes to get consumers back into the marketplace.

While inflation deters consumers from spending, it can also be an opportunity to attract consumer segments you hadn’t previously seen – if you use the right strategies to get them in the door.

Rising inflation is a huge concern for small businesses in the UK.

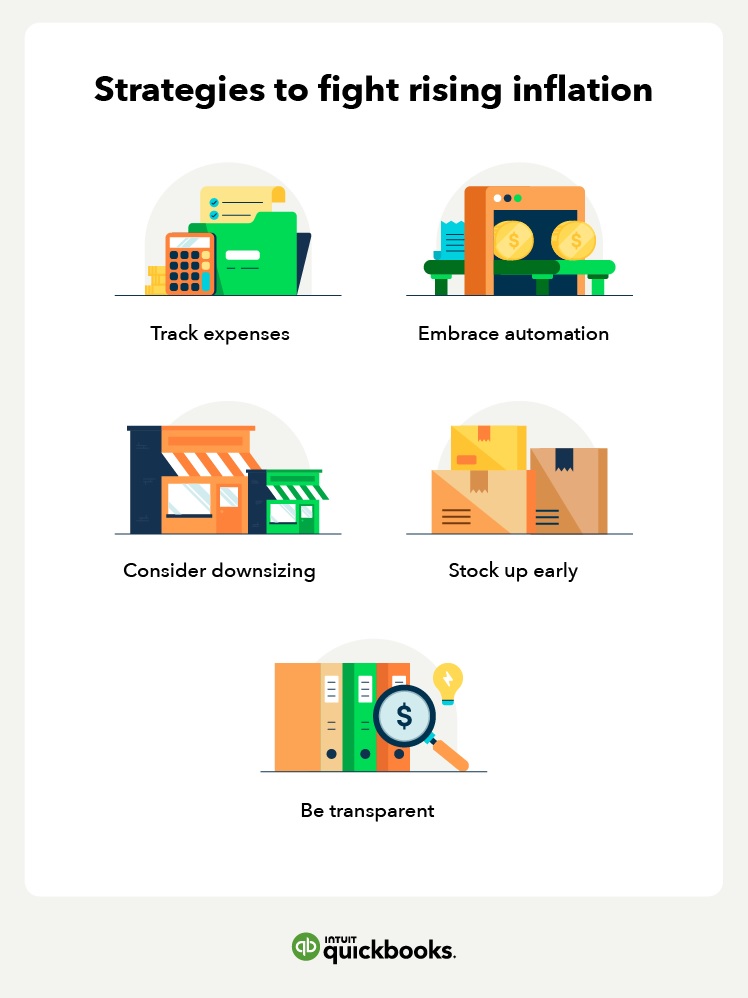

However, they can put different strategies into practice to soften the blow and sometimes come out more efficient and profitable. Here are a few strategies small business owners can put into practice in order to spin rising costs into more streamlined systems and greater profits.

Tracking expenses can be a proactive solution to prepare for rising inflation. You can do this in a couple of different ways.

First and foremost, it’s certainly helpful to have some familiarity with different accounting reports, like cash flow statements, income statements, and balance sheets. These reports paint a more holistic picture of expenses and profits, giving you a jumping-off point in case costs need to be cut.

In more pressing times, you may want to hire a professional to consult with you on your finances. Be it a tax accountant, financial advisor, or just a close friend who works in the financial sector, there’s no harm in getting a professional’s input when looking at expenses. A professional may even open your eyes to long-term cash-saving solutions.

Using expense tracking software is another great solution that eliminates human error from the equation. This type of software offers a clear dashboard to see your expenses and help you predict cash flow throughout the year.

In times of high inflation, efficiency is key and finding ways to automate processes to save time and money is an effective tactic to weather the storm and also come out stronger.

Automating processes additionally gives employees more bandwidth, which can be pivotal in supporting and retaining staff members during difficult times.

While automation will look different from industry to industry, simple things like maintaining an online presence or using tools to automate payroll can keep you dedicated to running your business, rather than managing bills.

If economists are predicting that inflation will continue to rise over a certain period of time, then it’s not a bad idea to stock up early to get ahead of rising shipping and inventory costs.

Supply chain disruptions that happen as a result of inflation can set your business back tremendously, so it’s best to overorder rather than be scrambling for supplies to meet consumer demand. Suppliers often offer discounts if you order in bulk as well.

Reducing office space is much easier for some industries than others; however, if it’s a viable option for you, it’s certainly something to consider.

If going fully remote isn’t an option for your small business, evaluating your current space and seeing if there’s an opportunity to downsize can still be an effective tactic for reducing overhead costs.

The overwhelming percentage of small businesses that raised their prices due to inflation is evidence that this is a decision that almost all small business owners already have or will have to face.

If you do go the route of rising prices, it’s important to be transparent with customers and clients that it’s for the purpose of staying competitive during tough financial times.

This can be as much as hanging a sign on the storefront, putting a banner on your e-commerce site, or sending an email to your client list. Regardless, it’s always best to let your clientele know your decision is being made, so you can continue to serve them in the future.

While inflation is certainly difficult for small businesses, “survival” isn’t necessarily the only option.

Knowing there’s still a large market, the need to remain competitive can inspire small businesses to adopt new processes that make them more efficient.

If small businesses continue with new processes like strategic marketing, automation, and smarter expense tracking in periods of normal inflation, they’ll thrive in their market. Inflation opens the door to new consumer segments that small businesses can capitalise on if they play their cards right.

To find new ways to streamline your processes and stay on top of cash flow, try QuickBooks for small UK businesses to track income and expenses.

The information on this website is provided free of charge and is intended to be helpful to a wide range of businesses. Because of its general nature the information cannot be taken as comprehensive and they do not constitute and should never be used as a substitute for legal, accounting, tax or professional advice. We cannot guarantee that the information applies to the individual circumstances of your business. Despite our best efforts it is possible that some information may be out of date. Any reliance you place on information found on this site or linked to on other websites will be at your own risk.

Share:

Subscribe to get our latest insights, promotions, and product releases straight to your inbox.

9.00am - 5.30pm Monday - Thursday

9.00am - 4.30pm Friday