Journeys by Design gains multi-year financial visibility with QuickBooks Advanced

Simple, smart accounting software - no commitment, cancel anytime

TAX AND PENSIONS

Deferred tax assets and deferred tax liabilities are opposites of each other.

A deferred tax liability means the company has a tax debt that will need to be paid in the future, and a deferred tax asset is a business tax credit to help with future taxes.

Think of it like paying part of your taxes in advance, or paying additional taxes after.

It’s worth noting that deferred tax is only needed on some financial statements. For example, entities like sole traders (who don’t do financial statements) or companies that prepare micro-entity accounts (due to their size) do not need to calculate deferred tax.

In this article, we’ll cover what deferred tax assets and liabilities mean in the UK:

In accounting, there are different rules for UK tax reporting and financial reporting. A key difference is the timing of recognising payments. You may need to pay taxes on income you expect to receive in the current period, even if you haven’t had the payment yet.

This difference in timing between payments can cause a situation called deferred tax.

To understand the meaning of deferred tax assets and liabilities, you need to understand the difference between financial reporting and tax reporting. These two types of accounting have separate sets of calculations, which can lead to both deferred tax liabilities and assets.

Financial reporting involves the creation of financial statements in accordance with the accounting standards of the UK, such as those set out by the Financial Reporting Council (FRC). The financial reporting statements show detailed information about a business or company’s pre-tax net income, income tax expense, and net income after taxes.

However, tax reporting means sticking to the rules of tax authorities in the UK, such as HM Revenue and Customs (HMRC). It involves preparing and submitting tax returns in compliance with UK tax regulations and laws, rather than FRC’s accounting standards.

There are two types of deferred tax items. One represents money the business owes (deferred tax liability), and the other represents money owed (deferred tax asset).

Again, it’s worth noting that not all companies need to account for deferred tax rules. For example, micro-entity companies who use Financial Reporting Standards FRS105 (as opposed to FRS102) do not have to calculate deferred tax in their accounts.

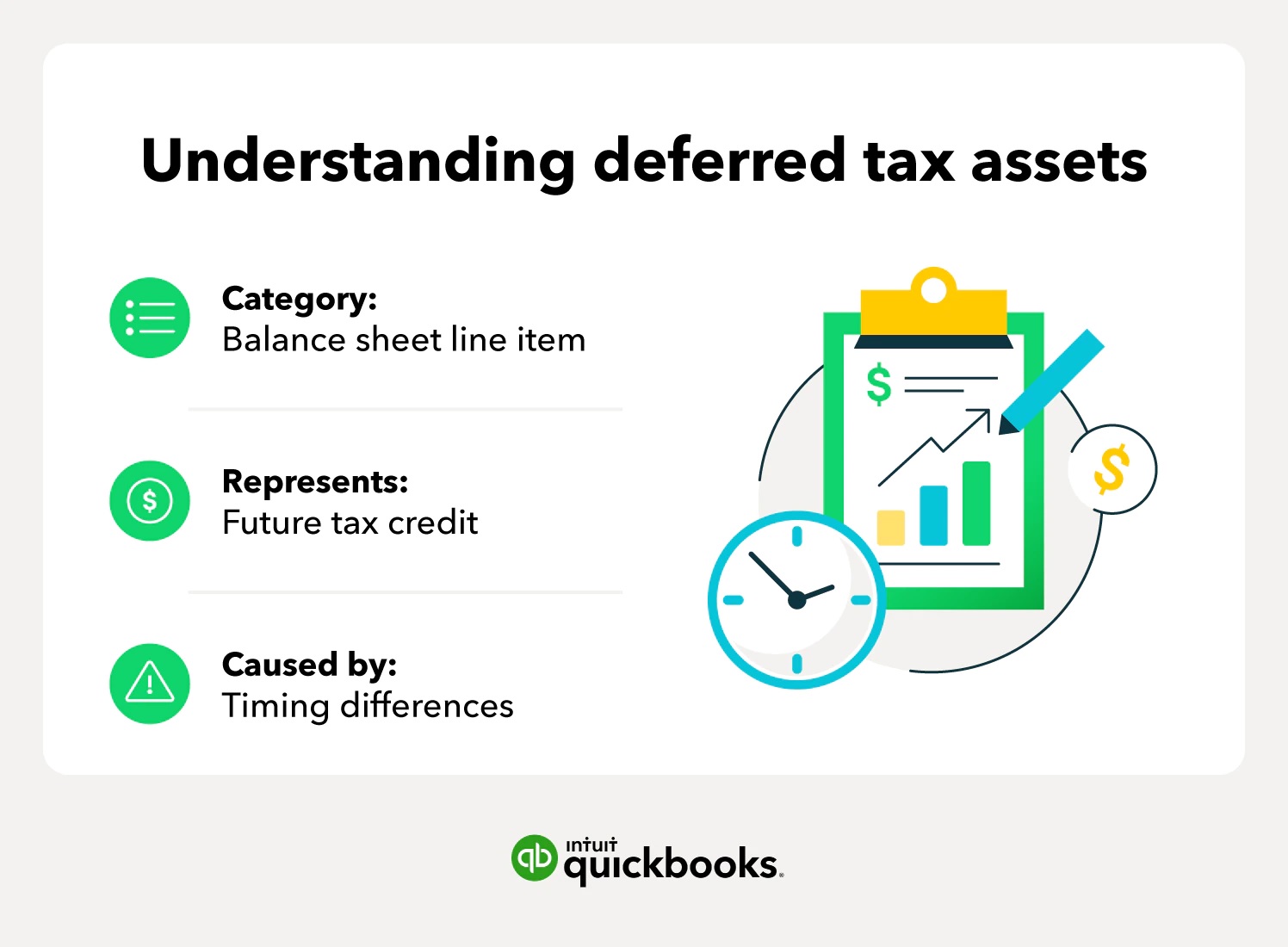

A deferred tax asset or DTA is an entry on the balance sheet representing the difference between taxes owed and the company’s internal accounting.

For example, if a business paid its taxes in full but later received a tax deduction for that period, the unused deduction can be carried forward and utilised as a deferred tax asset in the business’ future tax filings.

In the UK, there have been various changes to corporate tax rates and regulations over the years. If tax rates change, this can cause a business to overpay or underpay their tax.

What type of asset is a deferred tax asset? A deferred tax asset is thought of as an intangible asset because it is not a physical object like equipment or buildings. It only exists on the balance sheet.

Is a deferred tax asset a financial asset? Yes, a DTA is a financial asset because it represents a tax overpayment that can be redeemed in the future. In some cases, deferred tax assets may be classified as a separate category of assets within the financial statements.

Where are deferred tax assets listed on a balance sheet? In the UK, deferred tax assets are typically presented as "non-current assets" on the balance sheet. This means they are classified as assets expected to be realised or used beyond one year.

When does a deferred tax asset have to be used? Deferred tax assets do not have an expiry date and can be used when it is most convenient for the business.

Note: While deferred tax assets can always be carried forward to future tax filings, they cannot be applied to tax filings in the past.

Deferred tax assets happen when there is a discrepancy between taxable income reported in the tax return and income recorded in the company's records (known as book income).

As an example, think of if you bought a train ticket and the train got delayed, and the company gave you £50 as a voucher. If you’d planned to spend £50 on train fares the next month, you could change your budget as you have a voucher cancelling out the expense.

The voucher represents your deferred tax asset in the UK. Although you haven’t used it yet, you recognise its future value and can change your upcoming financial plans around it.

Net operating loss: The business incurred a financial loss for that period.

Tax overpayment: You paid too much in taxes in the previous period.

Business expenses: When expenses are recognised in one accounting method but not the other.

Revenue: Instances where revenue is collected during one accounting period, but recognised in another.

Bad debt: Before an unpaid debt is written off as uncollectible, it’s reported as revenue. When the unpaid receivable is finally recognised, that bad debt becomes a deferred tax asset.

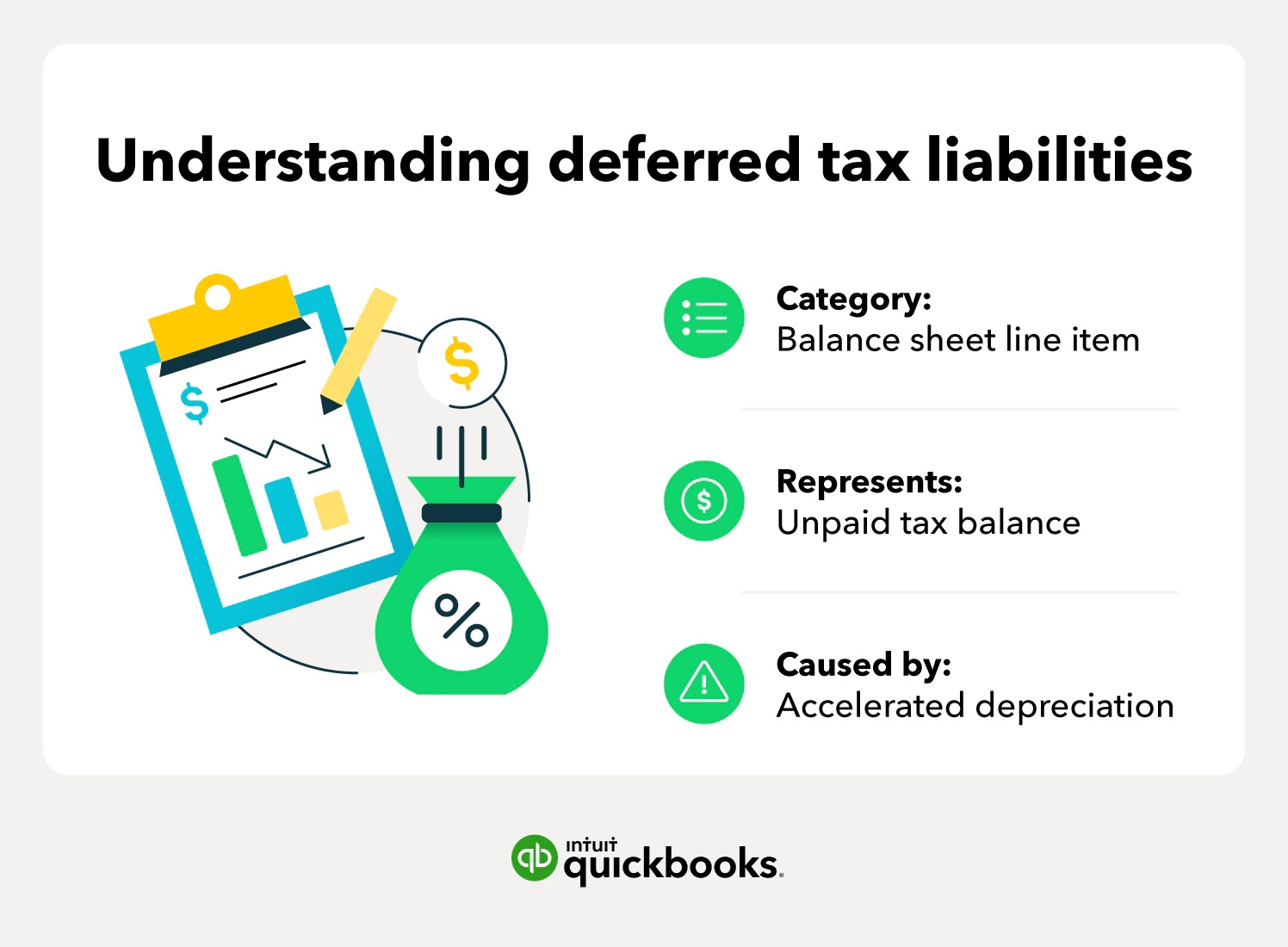

The meaning of deferred tax liability (DTL) is a tax payment a company has listed on its balance sheet but does not have to pay until a future tax filing.

One type of DTL is a payroll tax holiday, which allows businesses to put off paying payroll taxes until a later date. It represents a benefit for the company right then, but a liability to the business later financially.

Similarly, certain tax incentives or deductions, such as depreciation expenses on company vehicles, can create temporary differences between accounting and tax reporting. These differences can give rise to deferred tax liabilities in the UK, representing the future tax obligations associated with those deductions or incentives.

Is deferred tax liability a debt? A deferred tax liability journal entry represents a tax payment that, due to timing differences in accounting processes, the payment can be postponed until a later date.

Where are deferred tax liabilities listed on the balance sheet? They are listed on the balance sheet as “non-current liabilities.”

Are deferred tax liabilities good or bad? A deferred tax liability is neutral or good, depending on your situation. It means you owe money, but don’t have to pay it right away. The downside is that your business needs to have money set aside in order to pay this debt off in the future.

Any temporary difference between the amount of money owed in taxes and the amount of money that is required to be paid in the current accounting cycle creates DTL.

Keep digital records, submit quarterly updates to HMRC, and finalise your Income Tax at the end of your accounting period with Intuit QuickBooks.

Explore plans & pricing

Imagine you purchase an annual membership to a fitness club and pay the full amount upfront. However, due to unforeseen circumstances, the fitness club temporarily closes down for renovations. As a result, the club cannot provide the services covered by your membership for a few months. They acknowledge the situation and agree to extend your membership for an additional few months once the renovations are complete.

In this scenario, the amount you prepaid for the membership represents a deferred tax liability. The fitness club owes you services for the remaining months of your membership that have not been utilised yet. While they have received the payment upfront, they have an obligation to provide the services at a later date, resulting in a deferred liability.

Similarly, in the UK, a deferred tax liability can arise when a company recognises a tax obligation in its financial statements but does not need to pay the corresponding tax until a future period. It represents a timing difference where the tax payment is postponed until a later point in time.

It's important to note that specific circumstances and regulations may vary, so consulting the latest UK tax laws or seeking professional advice is recommended for accurate information on deferred tax liabilities in the UK.

Depreciation of assets: In the UK, a deferred tax liability can arise from the difference between the accounting depreciation of assets and their tax depreciation. The tax rules for asset depreciation may differ from the accounting rules, resulting in temporary differences and the recognition of deferred tax liabilities.

Tax underpayment: If a company has not paid the full amount of tax owed in a previous tax period in the UK, it may have a deferred tax liability. The company will be required to make up for the underpayment in the subsequent tax cycle.

Timing differences in revenue recognition: Certain transactions, such as instalment sales or long-term contracts, may result in timing differences between revenue recognition for accounting purposes and revenue recognition for tax purposes in the UK. These timing differences can give rise to deferred tax liabilities, as the tax payment will be deferred to future periods when the revenue is recognised for tax purposes.

It is important to note that the examples provided are intended to illustrate the general concept of deferred tax liabilities within the UK context.

It can be hard to determine when, and if, you’ll be able to take advantage of a deferred tax asset. The balance isn’t hidden because it’s reported in the financial statements. Analysts can take deferred tax balances into account, so there’s no distortion of the financial picture.

A significant type of deferred tax are net operating loss carryforwards. These are when a business has a net loss but isn’t able to deduct all of the loss in the current year. The loss’ remaining balance is taken forward until the business has a high enough net income.

However, you can’t predict what years you’ll be able to use the carryforward, or if you can use them all before the tax law stops you from carrying the loss forward to future years.

You’ll want to understand the following equation when evaluating deferrals:

Income tax expense = taxes payable + deferred tax liability – deferred tax asset

Understanding this equation can help you better understand your income statement.

If you have deferred tax assets and liabilities in the UK, it is highly likely that lenders, investors, or potential buyers will be interested in understanding them. Prior to engaging with important stakeholders regarding financial matters, it is advisable to consult your chartered accountant (CA) or tax advisor with the following types of inquiries:

Of the netted figure on the balance sheet, what is the breakdown between deferred tax assets and deferred tax liabilities?

What comprises the assets and liabilities? What events caused them?

When do you expect the business to realise the tax assets and liabilities?

How likely do you think it is that the business will be able to recognise the tax assets and liabilities? Is it inevitable, very likely, or only somewhat likely?

The FRC sets the accounting standards and requirements in the UK. The FRC requires disclosure of deferred tax balances in the financial statements, which can be found in the relevant reporting standards and guidelines provided by the FRC.

In the UK, tax accounting and financial accounting have separate sets of rules and regulations. The revenue and expenses reported in a company's financial statements may not always align with the income and deductions recognised for tax purposes.

As a result, the taxable income calculated for tax reporting in the UK may differ from the net income reported in the financial statements. This is primarily due to variations in the rules and principles governing the recognition and measurement of revenues, expenses, and deductions in tax accounting compared to financial accounting.

Temporary tax differences in the UK arise due to timing variations in recognising income, expenses, and deductions between tax accounting and financial accounting. These differences result in certain items being recognised earlier or later for tax purposes compared to their recognition in the financial statements.

For example, certain income or expenses may be recognised in the financial statements in a particular accounting period but are taxable or deductible in a different period for tax purposes. This creates temporary timing differences.

Deferred tax assets and liabilities in the UK are associated with these temporary timing differences. A deferred tax asset indicates that a business has accumulated future deductions or losses, which can be used to offset taxable income in subsequent periods, resulting in a positive cash flow.

On the other hand, a deferred tax liability represents a future tax obligation that will arise due to the timing differences between taxable income and accounting income.

In the UK, businesses may use different ways of calculating depreciation for financial accounting purposes and tax purposes. As an example the business may choose to use an accelerated depreciation method for tax purposes – this results in higher depreciation expense in the early years of an asset’s existence and lower expense in later years.

The disparity between the depreciation expense claimed on the tax return and the depreciation expense recorded in the company's accounting records is temporary. Over the asset’s life, the total amount depreciated stays the same. Differences happen due to the timing of recognising the depreciation expense each year.

With deferred tax assets in the UK, if a company incurs a loss on the sale of an asset and can recognise the loss on a future tax return, it can be considered a deferred tax asset.

For UK businesses, deferred tax liabilities are netted against deferred tax assets and disclosed on the balance sheet. But for pass-through entities like S corporations, sole proprietorships and partnerships, the net amount of deferred tax assets and liabilities could be reported on a supporting schedule in the company’s tax return.

In the UK, companies follow specific depreciation rules and methods outlined in the applicable accounting and tax regulations. The depreciation policies and rates may differ based on the nature of the assets and the accounting standards followed.

After learning the definitions and examples of deferred tax assets and deferred tax liabilities, we can better understand our balance sheet with regard to these future tax credits or debits. To avoid tax filing errors related to these topics, use reliable accounting software, and discuss any deferred tax balances with a tax preparer.

As a new small business owner, deferred tax assets and expenses are one example of a complex subject that could easily confuse business owners, complicating matters in future periods.

If you would like to know more about how deferred assets and liabilities impact your small business, be sure to contact your trusted accountant or tax professional. Doing so will help ensure you follow proper accounting standards while receiving the maximum tax benefit.

The information on this website is provided free of charge and is intended to be helpful to a wide range of businesses. Because of its general nature the information cannot be taken as comprehensive and they do not constitute and should never be used as a substitute for legal, accounting, tax or professional advice. We cannot guarantee that the information applies to the individual circumstances of your business. Despite our best efforts it is possible that some information may be out of date. Any reliance you place on information found on this site or linked to on other websites will be at your own risk.

Share:

Subscribe to get our latest insights, promotions, and product releases straight to your inbox.

9.00am - 5.30pm Monday - Thursday

9.00am - 4.30pm Friday