Small business employment holds steady in Q2-2026

Simple, smart accounting software - no commitment, cancel anytime

The 2025 Intuit QuickBooks Small Business Late Payments Report reveals UK small businesses with unpaid invoices are currently owed more than £21,000 each, on average, and that payment delays could potentially be affecting much more than their cash flow.

The findings below reveal that small businesses with unpaid invoices are more likely to report cash flow problems, difficulty accessing credit, and difficulty hiring and retaining skilled workers.

Key findings:

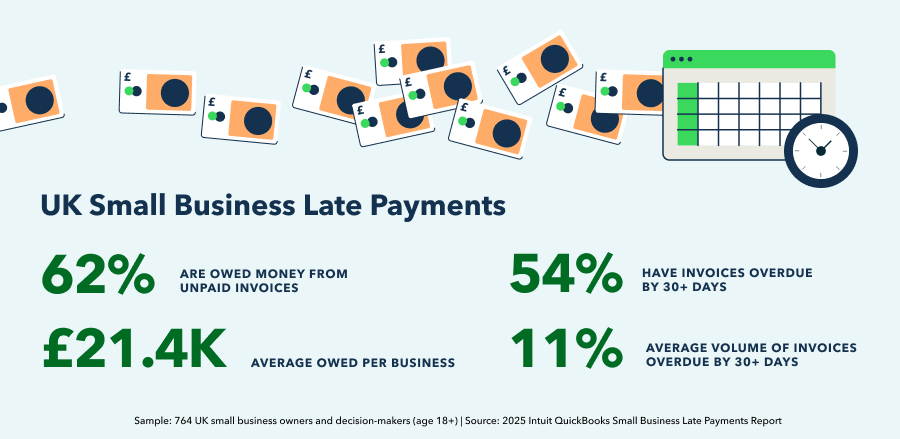

62% of UK small businesses surveyed are owed money from unpaid invoices.

On average, these businesses were each owed £21.4K in unpaid invoices.

54% have at least 1% of their invoices overdue by 30+ days.*

On average, 11% of invoices are 30+ days overdue.

Small businesses with the most invoices overdue by 30+ days were more than 1.5 times more likely to report cash flow problems, more than 3 times more likely to report greater reliance on credit cards, nearly 6 times more likely to report a credit card denial over the last half of 2024, and 1.4 times more likely to report difficulties in both hiring and retaining skilled workers.

Jump ahead:

Three in 5 (62%) UK small businesses surveyed reported grappling with unpaid invoices. This isn't just a minor financial hiccup; these businesses were, on average, owed £21.4K in late payments. Adding to this challenge, over half of these businesses (54%) reported having invoices that were more than 30 days overdue. On average, an estimated 11% of all their invoices fell into this extended overdue category, further complicating their financial burdens and cash flow management.

When overdue invoices pile up, small businesses may find challenges spreading to other areas of their business. More than 3 in 5 (67%) with a higher volume of invoices overdue by 30+ days reported cash flow challenges, making them more than 1.5 times more likely to report cash flow issues than those less affected (43%). This gap in financial stability could affect critical business decisions. For example, they were 1.5 times more prone to dip into cash reserves (45% vs. 30%) and 1.4 times more likely to depend on credit cards to manage their cash flow (34% vs. 24%).

The data also suggests a strong correlation between payment terms and sales growth for UK small businesses. Businesses requesting immediate payment of their invoices reported an average sales revenue growth rate of 5% over the previous quarter. For comparison, those with 90-day terms had just 2% growth—which is 2.5 times lower.

This disparity can also be seen in future projections. Looking ahead, businesses with immediate payment terms projected an 11% average sales revenue increase from the end of 2024 to early 2025, more than double the 5% increase expected by those with longer payment terms. These trends indicate a potential association between shorter payment terms and higher sales growth, suggesting that businesses with more prompt payment structures may also experience more robust revenue increases.

The strain of unpaid invoices may also escalate credit and financing challenges for small businesses. Businesses grappling with a higher volume of invoices overdue by 30+ days were 3 times more likely to identify financing as their primary obstacle, with 19% citing it compared to just 6% of those less affected. This financial pressure appears to be related to difficulties accessing credit; these businesses were nearly 6 times more likely to report being denied a credit card over the last half of 2024. Similarly, while 25% of businesses less impacted by long-overdue invoices reported not needing financing, this number dropped to just 6% among those heavily affected. This increased need manifests in higher usage of various financing options, including loans (28% vs. 15%), lines of credit (22% vs. 8%), and both business (46% vs. 21%) and personal credit cards (26% vs. 13%). The challenges posed by extended payment delays reveal an urgent need for effective strategies that prevent businesses being overwhelmed by outstanding debts.

As highlighted in the 2025 Intuit QuickBooks Small Business Index Annual Report, access to credit and financing can mean the difference between flourishing and stunted growth for small businesses, particularly in periods of high interest rates. The report found credit card financing can boost growth in the short-term but may also carry longer-term risks for small businesses.

Those risks could grow when small businesses aren’t paid quickly. For example, businesses with 90-day payment terms showed greater use of credit cards, using them to pay for 32% of monthly expenses on average compared to 27% for those with shorter terms. Those reporting the most overdue invoices allocated an average 34% of their expenses to credit cards, in contrast to the 24% among those experiencing fewer delays.

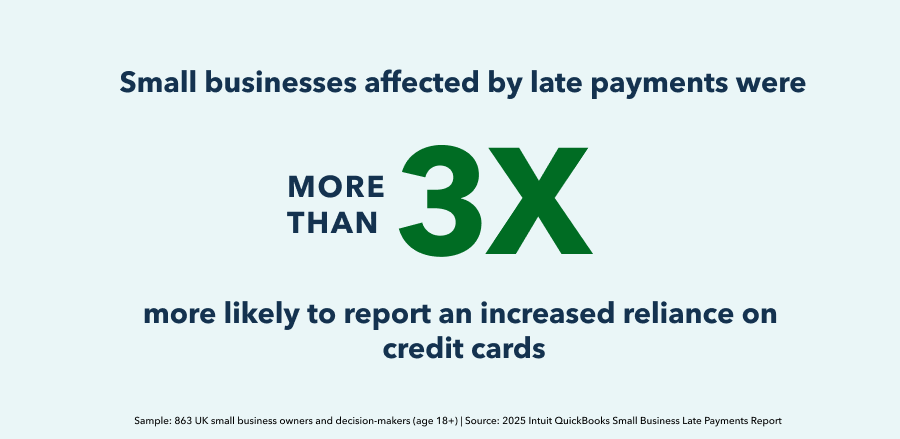

The survey data also shows small businesses affected by late payments were more than 3 times as likely to report an increased reliance on credit cards. Among those with the most overdue invoices, 47% reported greater reliance on credit cards over the past year compared to 15% of less impacted businesses. Similarly, they reported carrying an average 31% of their credit limit on their balance, compared to 15% for those experiencing fewer delays.

The correlations uncovered in the survey data extend to the very backbone of small businesses: their workforce. Businesses struggling with a higher volume of overdue payments were more likely to report challenges in both hiring and retaining skilled employees. Those more impacted were 1.4 times more likely to report difficulties in hiring skilled workers, with 44% experiencing these issues compared to 31% of those less affected. This struggle to attract talent is compounded by retention challenges; while 23% of businesses with a lower volume of overdue invoices reported difficulties holding onto staff, this figure jumped to 34% for businesses heavily burdened by late payments.

These challenges underscore that late payments can cast a long shadow, potentially impacting both the financial and human capital of UK small businesses, making it essential to address payment delays for their overall health and sustainability.

Intuit QuickBooks Small Business Insights is an international, quarterly survey of small business health, opinions, and priorities commissioned by Intuit QuickBooks every three months since its launch in September 2021. Each wave has been fielded among small businesses in the US, Canada, and the UK. In April 2024, the survey was expanded to include small businesses in Australia as well.

The findings in this analysis are based on the November 2024 survey of 1,063 UK small businesses with 0-100 employees. The research focused on understanding the impact of payment and invoicing practices on various aspects of business health.

All findings presented demonstrate statistical significance. This indicates that observed results are highly unlikely to have occurred by random chance, suggesting a genuine relationship or effect.

The data was analyzed in two main ways:

Payment Terms: The first analysis compared how different payment terms (Immediate, Within 30 days, Within 90 days, and Other) influenced financing, cash flow, sales, financial health, digitisation, workforce, hiring, and retention.

Overdue Invoices: The second analysis examined the relationship between the percentage of overdue invoices (categorized as 0%, 1-19%, 20-39%, 40-59%, 60-79%, and 80-100%, then grouped into 0-19% and 20-100%) and the same business aspects mentioned above.* “54% have invoices overdue by 30+ days” is the aggregated number of respondents who didn’t choose “0%” in response to this question.

Participants are small business owners and decision-makers from two sources:

Dynata panel: minimum 3,350 survey respondents per wave. Of these, at least 1,500 are from the US, at least 600 are from Canada, at least 750 are from the UK, and at least 500 are from Australia. On average, more than 50% of the respondents are small business owners. The remainder are senior decision-makers within small businesses who have a detailed knowledge of their employer's financial performance, workforce strategy, and business priorities. For each wave of the survey, 50% of the sample are repeat respondents who have previously taken the survey to allow opinions and business health to be tracked more effectively over time. Respondents receive remuneration. All responses are anonymous. In the US, Canada, and the UK, all respondents are from small businesses with 0 to 100 employees. In Australia, all respondents are from small businesses with 0 to 50 employees. Every effort is made to make these samples as representative as possible of small businesses in each country but as with all online surveys, there are limitations. To give the largest possible sample size for each wave of the survey, responses from the Dynata panel are combined with responses from the QuickBooks customer panel, described below, whenever possible.

Intuit QuickBooks customer panel: The number of survey participants drawn from the Intuit QuickBooks customer base varies over time but the average is 2,000 respondents per wave. In the April 2024 wave, for example, the total number of QuickBooks customer respondents was 2,300; comprising 1,505 in the US, 405 in Canada, and 405 in the UK. Currently, the survey is not fielded among QuickBooks customers in Australia. Respondents are drawn from a pool of QuickBooks Online subscribers in the US, Canada, and the UK who have been active in their accounts in the past 30 days. As with the Dynata audience panel described above, respondents in the US, Canada, and the UK are typically from small businesses with 0 to 100 employees.

For clarity, percentages have been rounded to the nearest whole number so in some of the stacked column charts shown above, survey responses may not add up to 100% but 99% or 101%, for example, instead. Please also note that all responses to multiple choice questions are shown as a percentage of the total number of respondents, not the total number of responses, to better reflect the number of people who chose each answer option. As a result, in the corresponding grouped column charts shown above, the sum of the percentages will always be greater than 100.

Disclaimer

This content, report and materials are for informational purposes only and should not be considered legal, accounting, financial, investment, or tax advice, or a substitute for obtaining such advice specific to your business. Additional information and exceptions may apply. Applicable laws may vary by state or locality. No assurance is given that the information is comprehensive in its coverage or that it is suitable in dealing with a customer’s particular situation. Intuit Inc., or its affiliates do not have any responsibility for updating or revising any information presented herein. Accordingly, the information provided should not be relied upon as a substitute for independent research. Intuit Inc., or its affiliates do not warrant that the material contained herein will continue to be accurate nor that it is completely free of errors when published. Readers should verify statements before relying on them.

We provide third-party links as a convenience and for informational purposes only. Intuit Inc. or its affiliates do not endorse or approve these products and services, or the opinions of these corporations or organizations or individuals. Neither Intuit Inc. nor its affiliates assume responsibility for the accuracy, legality, or content on these sites.

Share:

Subscribe to get our latest insights, promotions, and product releases straight to your inbox.

9.00am - 5.30pm Monday - Friday