Making Tax Digital

QuickBooks 90-60-30 MTD Planner

Simple, smart accounting software - no commitment, cancel anytime

FINANCE, BUDGETS AND CASHFLOW

How do you calculate the value of your small UK business, if you want to sell it?

Two words: owner’s equity. It may sound like financial jargon, but calculating your owner’s equity helps show exactly what you own in your business after you’ve paid off your debts.

By subtracting liabilities from assets, you calculate what your business is worth.

Here’s what need to know about equity ownership. From examples of things you own (assets) and things you owe (liabilities), to how owner’s equity impacts your decisions.

Simply put, equity refers to the worth of something. This means the owner’s equity represents the owner’s net worth of a business. It is the total value of a company’s net assets after all liabilities have been deducted.

Owner’s equity is more than just a number. It’s the value you’ve built over time and a key indicator of your business's financial health and potential.

Knowing your owner’s equity can help you make better business decisions.

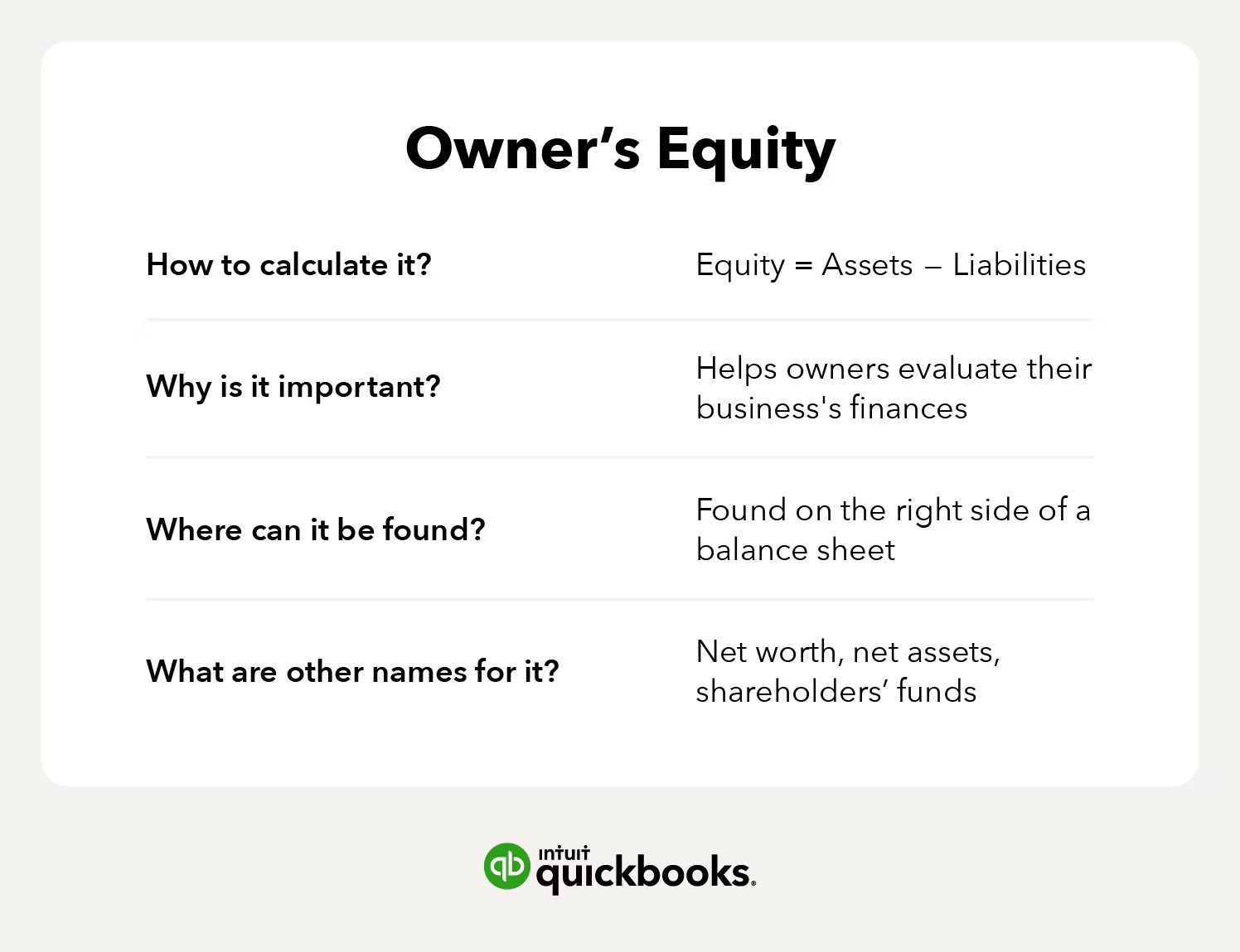

To calculate a business's worth, you need to know its assets and liabilities. The accounting formula required to do this is as follows:

Equity = Assets – Liabilities

The business's assets (resources), minus liabilities (what the business owes others), is equal to the total net worth of the business, also known as owner’s equity.

Here’s a quick explanation of assets and liabilities:

Assets: what your business owns, such as property and equipment

Liabilities: what your business owes, such as loans or bills

This is attributable to one, or multiple owners, depending upon how the business is owned.

Owner’s equity of a business can be found along with liabilities on the right side of the balance sheet, and assets can be found along the left side.

Typically, the items that are included in the owner’s equity on the balance sheet are:

Money invested into the business by the owner

Profits of the business since its inception

Minus money the owner has taken out of the business

Minus money owed to others

Owner’s equity behaves much like a bank account balance, reflecting the ups and downs of financial activity.

Similar to making a deposit into a bank account, owner’s equity grows (or increases) when:

Your business makes money.

You decide to put more money into the business.

Your business assets (for example, property) increase in value.

And much like withdrawals from an account, owner’s equity decreases when:

Your business loses money.

You decide to take money out of the business.

Your business assets decrease in value.

If your owner’s equity is negative, here are some steps to improving it over time.

Focus on boosting revenue and reducing unnecessary expenses to grow your business’s net income, which directly increases owner’s equity over time.

Instead of withdrawing all profits, reinvest some earnings into the business to fund growth, improve operations, or invest in new assets.

Reduce liabilities by paying off loans and avoiding unnecessary debt. Lower liabilities mean higher equity, making your business financially stronger.

Accounting software can help you track your expenses, assets, and liabilities in real-time, create clear financial statements, and see your business’s value at a glance.

Make smarter decisions, manage debt, and plan for growth with QuickBooks.

Keep digital records, submit quarterly updates to HMRC, and finalise your Income Tax at the end of your accounting period with Intuit QuickBooks.

Explore plans & pricing

A statement of owner’s equity reflects these increases and decreases in owner’s equity over a specific period.

Usually prepared after the income statement, the owner’s equity statement (also known as the statement of changes in owner’s equity) focuses on a specific reporting period (often a year). It starts with an opening balance — the initial amount in the capital account at the beginning of the period being documented — and then tracks:

Any increases from capital contributions (the owner’s additional investments) and business profits

Any decreases from capital distributions (withdrawals made by the owner) and business losses

It concludes with a closing balance, which must match the owner's equity figure on your balance sheet for the same period.

As noted above, this statement will reflect an increase in owner’s equity for the operating income generated by the business. It will also include the decreases from the distribution of wages to fund the owner’s lifestyle.

Therefore, these financial statements record all contributions and incomes, as well as withdrawals and expenses of the business. Other statements include the:

Balance sheet

Profit and loss statement

Cash flow statement

Creating this statement relies on the accurate recording and analysis of your business’s balance sheets. Accounting software can help your small business do this. With the QuickBooks reporting feature, create professional-looking balance sheets, covering assets and liabilities, to gain a clear picture of your business’s equity.

Generally, equity begins with the original contribution to the organisation by way of assets, typically cash and, or assets used within the business.

For example, suppose the owner of a limited company contributed £100 of cash and a machine that cost £200 for his product’s manufacturing. In that case, the company’s assets would be £300, and the equity would be £300 as well.

Net income increases equity over time. Equity fluctuates as the business operations generate net income or loss. Net income is the excess amount of a company’s revenue over expenses for a specific period.

If a business is making money, it is generating net income. Like owner investment, net income causes the owner’s equity in the enterprise’s assets to increase.

Capital reflects the sources of financing needed to acquire assets for a business. Equity and debt are two forms of capital.

Suppose the previously discussed UK entrepreneur who possesses £300 in equity, decides to buy a second machine. However, he does not have the funds to do it himself, so he asks the bank for a loan. This loan is a debt of the company.

Once he receives the £200 loan and buys the second machine, his assets increase to £500, but his equity remains the same £300. At the same time, he takes on liabilities of £200.

With two machines, he generates twice the amount of operating profit, doubling his operating earnings, minus interest on the loan, allowing him to grow his equity account.

If the owner’s equity is the owner’s share of assets in a company, then the debt is other peoples’, or the bank’s, capital deployed in the business.

A decrease in owner’s equity is when the owner, or entrepreneur, withdraws some of those earnings to support himself while operating the business, such as his wage.

The legal organisation of a business is often driven by the number of parties owning the business. Sole Trader refers to a business type owned by one person.

In contrast, multiple owners of a business are legally organised into business types such as partnerships or corporations. The worth of a business reflects the aggregation of all (one or more) owner’s equity.

Find out more about different business structures in our blog exploring sole traders vs limited companies.

A partnership refers to a business with two or more owners/partners. As a result, the owner’s equity appears as an aggregation of all partner’s equity.

Each partner, or owner, possesses a separate capital account, including the partner’s investments, withdrawals, and corresponding share of the business’s net income or net loss from operations.

Generally speaking, net earnings will be divided between the partners depending on the percentage of the business they own. There are a number of different partnership business types in the UK - general partnerships, limited partnerships and limited liability partnerships.

Similar to partnerships, corporations are often formed with multiple equity owners. However, corporations differ from certain partnerships types in that they provide legal liability protection to the owners which facilitates transferability of ownership interests. These numerous owners of a corporation are referred to as shareholders.

Shareholders are the investors who have purchased shares of stock in a company, thus becoming owners of said company. There can be between one and a limitless number of shareholders, depending on the corporation’s size. Therefore, the owner’s equity of a corporation is referred to as the aggregate shareholder’s equity.

Once the shareholders have been paid their dues at the end of an accounting period, what is left over is known as retained earnings, which can then be funnelled back into the corporation to keep it growing.

Whether you’re planning for expansion, assessing the impact of a new product line, or preparing for market shifts, understanding owner’s equity lets you evaluate your business's financial position accurately and plan for sustainable growth.

Navigating the intricacies of your business’s financial statements can be a complex task — but it doesn’t have to be. Streamline your financial management with QuickBooks' intuitive accounting software to demystify your financial reporting and experience the ease of having your financial information accurately calculated and readily accessible.

When one person or sole trader owns a business, it is known as the owner’s equity. However, when a company, or corporation, is owned by multiple people, or shareholders, it is referred to as shareholder’s equity.

Capital refers to the funding sources that are used by the owners to acquire the assets used to run a business. There are two main types of capital, equity capital and debt capital. Equity capital is the funding of a business by investors, while the owner’s equity capital is the funding of the business by the owner. Debt capital refers to funds loaned to the business from a bank to fund purchase of assets used in the business.

If you decide to sell your business, your net worth may be a different figure from what is offered by a buyer. Other factors are taken into account, such as your brand’s strength, any valuable intellectual property, or whether your business is in trouble financially.

In the UK, the term "sole trader" is used, while in the US, "sole proprietor" is more common. Both refer to a self-employed individual who owns and operates their business alone, with no legal distinction between the person and the business.

The information on this website is provided free of charge and is intended to be helpful to a wide range of businesses. Because of its general nature the information cannot be taken as comprehensive and they do not constitute and should never be used as a substitute for legal, accounting, tax or professional advice. We cannot guarantee that the information applies to the individual circumstances of your business. Despite our best efforts it is possible that some information may be out of date. Any reliance you place on information found on this site or linked to on other websites will be at your own risk.

Share:

Subscribe to get our latest insights, promotions, and product releases straight to your inbox.

9.00am - 5.30pm Monday - Friday