Small business employment holds steady in Q2-2026

Simple, smart accounting software - no commitment, cancel anytime

FINANCE, BUDGETS AND CASHFLOW

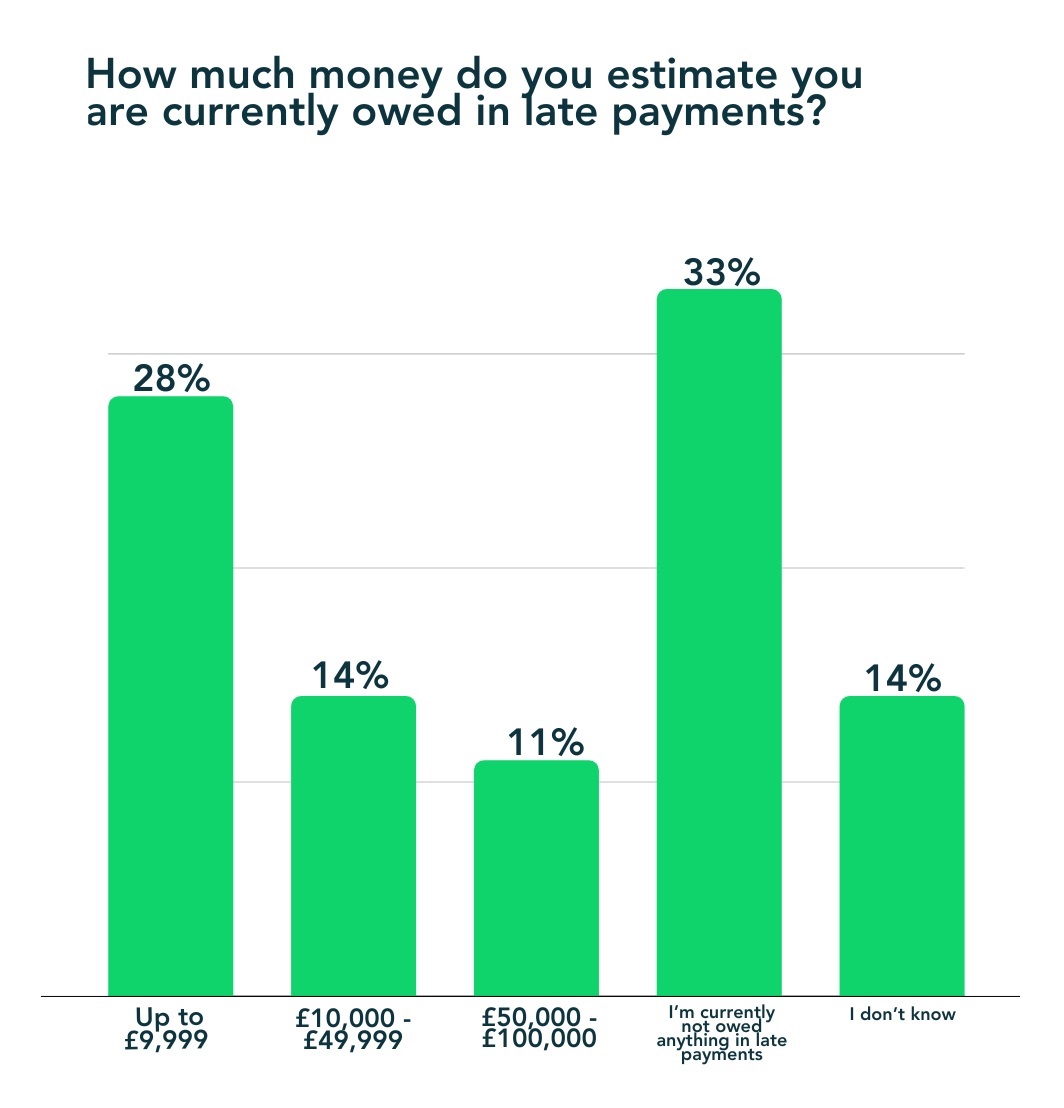

Late payments (Fig. 1) can be a burden for small businesses to bear and are often among the hardest-hit businesses across the UK.

When comparing our 2023 survey about late payments to our previous one in 2021, the average amount SMBs are owed has increased by 27.4% since September 2021.

Shockingly, 80 small and medium-sized business owners from our survey stated that they even had to consider firing staff due to money owed from late payments!

But there are ways for small businesses to protect themselves against the devastating impacts that come with dealing with late payments.

In our guide, we’ll go through some practices business owners may want to adopt to help safeguard their business. Here’s some tips on how to avoid late payments in the first place, using tools like invoicing software, and on how to deal with overdue payments if they occur.

Jump to a section in our guide:

An overdue or late payment is simply an invoice that hasn’t been paid yet.

A payment is classed as late if it’s not paid by the deadline agreed between a client and customer. If you haven’t agreed on a date, it’s usually considered late 30 days after the invoice has been received, or 30 days after you provided the product (whichever is later).

Overdue payments can have serious effects on small businesses, which we’ll cover later.

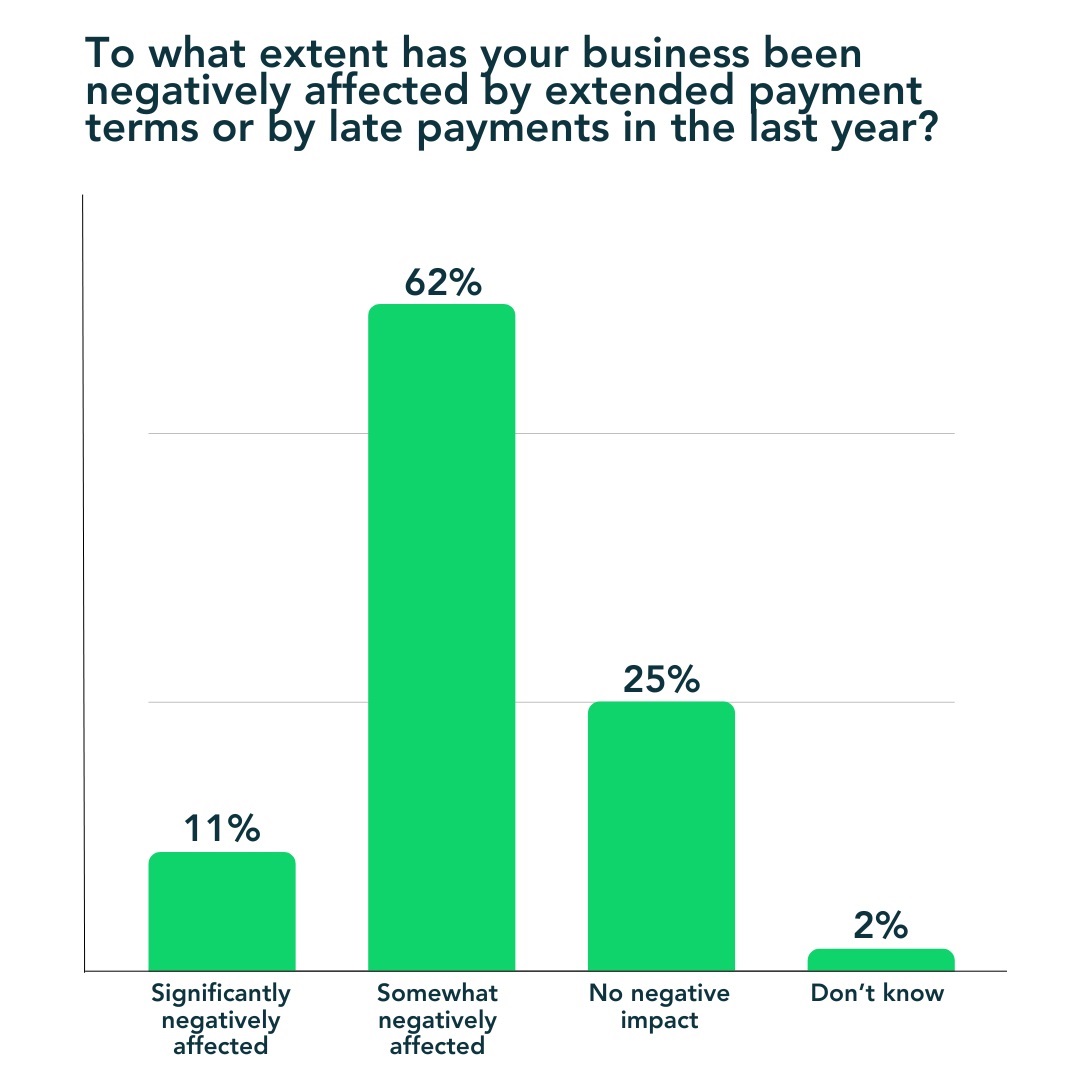

According to QuickBooks’ 2023 business survey, late payments are common. In fact, over 70% of SMBs were impacted by extended payment terms or late payments in the last year.

62% somewhat negatively affected

11% significantly negatively affected

Late payments can harm cash flow, growth, and employment, and around 40% of SMBs even fear potential closure if late payments persist. 52% of SMB owners were more affected by late payments in 2023, possibly due to the cost of living crisis causing cash flow issues.

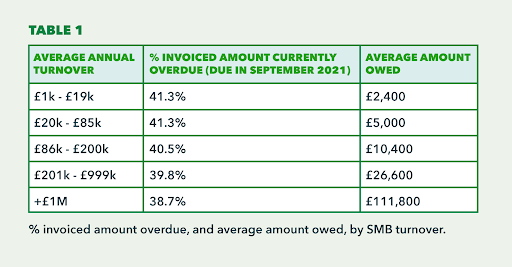

Larger businesses, especially those with a turnover of £100 million and 50 to 250 employees, reported the highest incidence of late payments, especially among companies ten years old or older. Our survey also shows that the manufacturing industry has encountered the greatest frequency of late payments over the past year.

Late and overdue payments can have significant negative impacts, particularly if you’re a small business. Here’s why it’s important to avoid or deal with late payments fast:

Cash flow issues: Late payments can damage your business’s financial health or even its survival. If you have a limited amount of cash coming in, you may not be able to manage essentials like paying your rent, your suppliers, or your taxes.

Increased borrowing costs: If you can’t pay essentials like the above due to late payments, your business may need to rely on loans or borrowing. This can add further strain on your business, and you’ll need to pay interest just to borrow.

Strained relationships: Businesses relying on timely payments may not be able to pay suppliers if those payments are late. This can cause reputational damage too, with unhappy customers if your products or services become delayed too.

Operational challenges: With a lack of cash, you may not be able to afford the essentials to run your business. You may struggle to pay your employee salaries or purchase materials or inventory, effectively grinding your business to a halt.

Missed growth opportunities: Your business can’t take advantage of opportunities to grow without some surplus cash. Marketing or investments might need to take a break until your customers can pay their late payments.

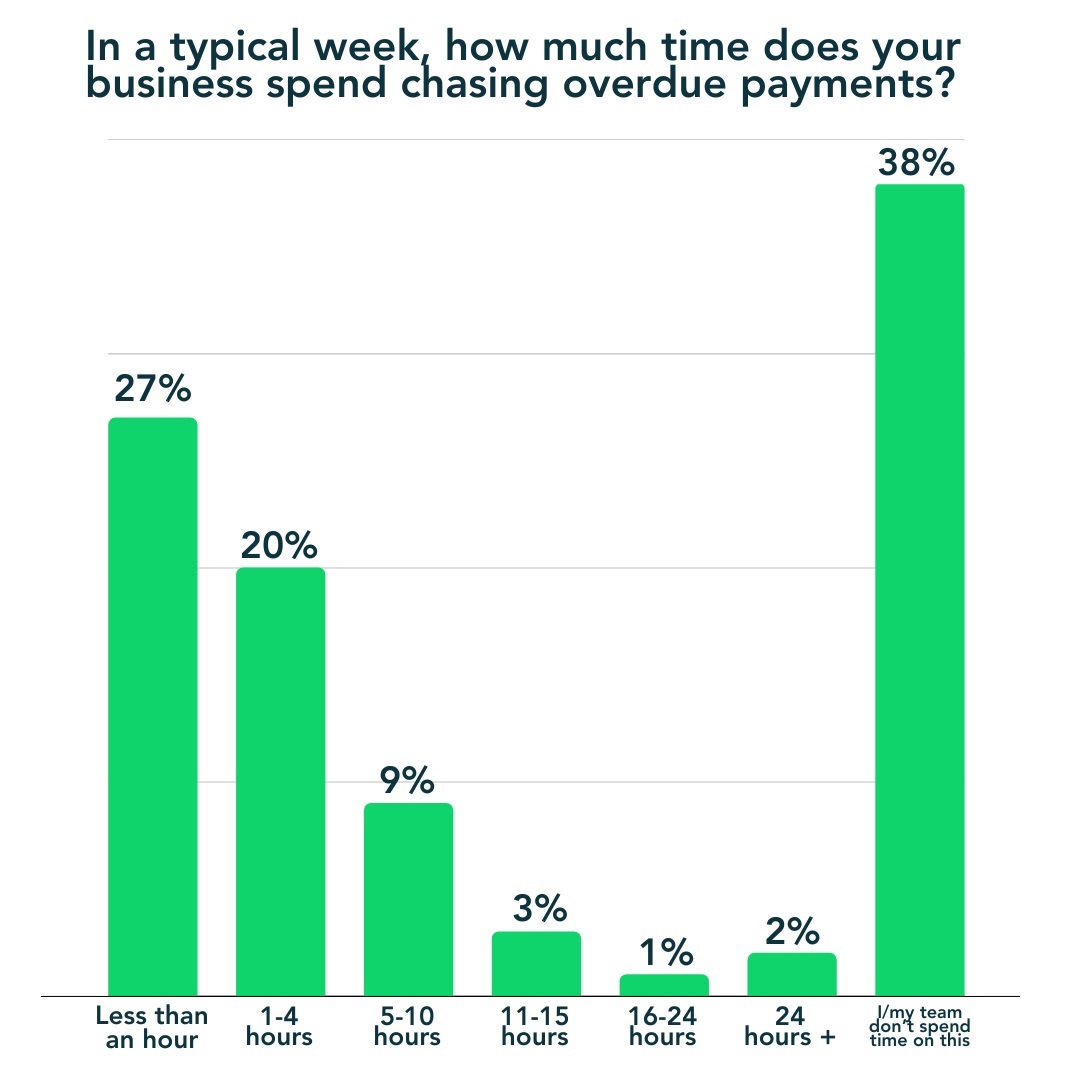

Increased admin time: Chasing late payments takes time and stress when you could be doing other things in your business. This could include sending emails, making phone calls, or even getting legal action involved if nothing works

Amazingly, our 2023 survey revealed that some small businesses spend over 24 hours chasing late payments in a week! This is valuable time that could be used for other work.

In summary, late payments from customers can cause damage to your business, leading to letting your other customers, suppliers, or employees down due to lack of funds.

So if you’re in the position of chasing a late payment, what can you do about it?

Chasing payments can be tricky because you want to maintain good relationships.

Late payments from customers can damage your business, but what can you do if a customer hasn’t paid after the date you agreed? First, try all of these tips below:

Ensure invoices are as clear as possible, showing customers exactly what they’re being charged for, multiple ways of paying, and what to do if they can’t pay

Send polite reminders before and on the due date of payments – a friendly reminder can prompt clients to prioritise your invoice and pay on time

Give a discount for paying early! This can be a win-win situation for both client and business, helping ensure your cash flow isn’t in trouble due to late payments

Clearly state your late payment policy in terms and conditions, and add to your invoices if needed. This can act as a deterrent for any consistent late payers

If a client is struggling, consider compromising with a payment plan – you’ll still get the full amount, just in monthly instalments over an agreed period of time

Escalate gradually, with friendly email reminders at first to more frequent communication or phone calls. Stay professional and try to seek a resolution

Here are some email templates you can use to chase late payments.

If the above doesn’t work, it is legal to start charging interest or add a late fee. This may incentivise them to pay quicker, but there are laws on how much to charge.

As a last resort, the small claims court may be able to help if nothing else has worked.

Keep digital records, submit quarterly updates to HMRC, and finalise your Income Tax at the end of your accounting period with Intuit QuickBooks.

Explore plans & pricing

So how much can a small business charge for late payments? The Late Payment of Commercial Debts (Interest) Act 1998 provides guidelines for businesses struggling with late B2B payments. The act gives a legal framework for getting compensation and interest:

It allows businesses to charge interest for late payments on commercial B2B transactions. For consumer, any late payment interest charges must be agreed in advance to the contract of purchase being signed.

It establishes a statutory interest rate, typically above the Bank of England base rate.

It gives an automatic right to claim interest on payments, without a prior agreement.

It provides a default payment time of 30 days (unless a different time is agreed).

It also allows businesses to claim compensation for costs, as well as just interest.

It allows creditors to enforce their rights through legal proceedings when necessary.

The statutory interest rate is set at 8% above the Bank of England base rate. The interest is calculated daily. Here's an example of how interest might be calculated:

Let's assume:

The Bank of England's base rate is 0.5%.

The statutory interest rate is 8% above the base rate.

The total interest rate would be 8.5% (0.5% base rate + 8% statutory rate).

Calculate Daily Interest Rate:

8.5% / 365 days = 0.0233% (rounded)

Calculate Interest on Late Payment:

If the invoice amount is £1,000 and the payment is 10 days late:

£1,000 * 0.0233% * 10 days = £2.33

In this example, the business could charge £2.33 as interest for the 10-day late payment. However, it’s important to check any contractual agreements between both parties.

As well as charging interest on late payments, small businesses can claim reasonable compensation. This is designed to manage associated admin and debt recovery costs.

The 1998 Act gives fixed sums for the size of the debts, as stated below:

Debt up to £999.99 - Fixed sum: £40

Debt from £1,000 to £9,999.99 - Fixed sum: £70

Debt of £10,000 or more - Fixed sum: £100

Businesses waiting for late payments should clearly add interest charges and any fixed compensation charges to each invoice. Interest for late payments is calculated daily, so the new invoice should be sent with the day’s correct calculation of interest.

For small businesses to survive despite late payments, they should look at tightening their payment terms and keeping a close eye on their invoices and payments.

It’s also a good idea to make paying invoices as easy and seamless as possible by utilising digital invoicing software.

Automating your payment process can be the difference between success and suffering with cash flow problems.

Accounting software can automatically track paid, opened and outstanding invoices. This means you can easily see the status of your invoices, giving you more control over your finances. The real-time alerts offered by digital accounting means you’re not left manually keeping track of each invoice, giving you more time to spend on other areas of your business.

The invoice tracking software offered by QuickBooks also gives you the option to send automatic reminders to your suppliers, meaning you don’t need to spend time chasing up late payments.

If suppliers and clients are offered various ways to pay invoices, the payment process can be drastically sped up. Whether this is contactless card readers, direct debit collection or even PayPal for electronic payments, offering as many ways to pay means you’re not limited in how you can accept payment. This also increases the chance that the way you collect payment aligns with how your clients prefer to pay invoices.

QuickBooks financial management software integrates with GoCardless, which is ideal for recurring payments and direct debits. Your clients will only need to input their card details the first time and payments are then collected automatically.

You may also choose to use PayPal for payments - and your clients don’t even need a PayPal account. Make collecting payments even easier by including a ‘pay now’ button on your invoices, meaning you don’t need to share bank details with your clients. This can speed up the payment process while keeping your details private and secure.

We know that chasing unpaid invoices takes time and can leave you feeling stressed and even a little awkward. So why not remove that stress with customisable automated reminders? By keeping track of each invoice status, you can easily send regular reminders to any unpaid invoices, ensuring your clients are reminded about paying you.

Take control over the frequency of these reminders so you’re not left waiting for unpaid invoices. And if your clients are reminded regularly, they’ll be more inclined to pay you faster.

Ensuring your invoices are paid on time is crucial to the success of your business. Investing in digital accounting software can make this process much easier, and take the burden of chasing clients away from you. By automating invoicing as much as possible, you can spend more time focused on other areas of your business.

1 Late payments are either: 1. invoices that were paid in full but paid after the due date or 2. still currently unpaid, or not paid in full

2Anonymised aggregated data from Intuit QuickBooks’s entire UK customer base. A snapshot of the late payments issues faced by SMBs in the UK today.

3 For SMBs in the private sector only. Government business population statistics state there are 5,583,245 private sector SMEs (0-249 employees) in the UK, with an average turnover of £2.3 trillion (£2,309,836,000,000). The average annual turnover is therefore £413,709. Dividing this by 12 gives the average monthly turnover of £34,475.75.

Using QuickBooks can help small businesses manage and deal with late payments. However, here are some good principles to follow to avoid them in the first place.

Establish clear payment terms: From the beginning of your business relationship, clearly communicate payment dates and how to pay. Have an honest conversation about any worries about payment and any suitable alternatives.

Conduct credit checks: When working with a new client and entering into a business relationship, you may want to check their credit rating. This can help you assess their financial stability and make informed business decisions.

Consider partial or staged payments: For large transactions, consider asking for partial payments at different stages of a project. This ensures your cash flow stays healthy, and reduces the impact a delayed payment can have on your business.

Maintain open communication: Build a strong relationship with your clients. This can help them prioritise paying your invoices on time, and be upfront with you about any potential concerns about late payments – before they happen.

By following these tips, you can avoid the impact of late payments on your small business and create a more stable future for your business, without the risks of a lack of cash!

With invoicing software and good relationships, late payments can be avoided.

Feel better about getting your invoices paid on time? Know what you’re owed and give customers more ways to pay.

Discover an easier way to manage payments with QuickBooks.

This content is for information purposes only, is provided free of charge and it is intended to be helpful to a wide range of businesses. Because of its general nature the information cannot be taken as comprehensive and they do not constitute and should never be used as a substitute for legal, accounting, or tax advice. Additional information and exceptions may apply. No assurance is given that the information provided is comprehensive, accurate or free of errors. Intuit does not have any responsibility for updating or revising any information presented herein. Any reliance you place on information found on this site or linked to on other websites will be at your own risk. You should consider seeking the advice of independent advisers and always check your decisions against your normal business methods and best practice in your field of business.

Share:

Subscribe to get our latest insights, promotions, and product releases straight to your inbox.

9.00am - 5.30pm Monday - Friday