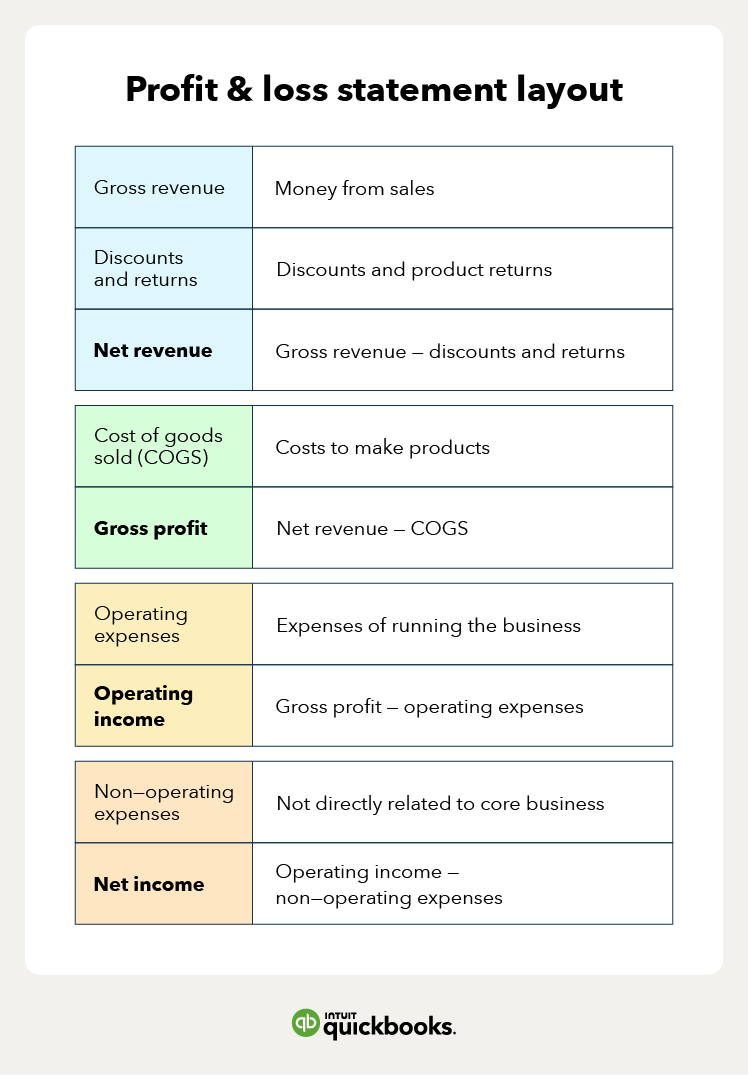

Revenue

Revenue is the money your business makes from selling goods or services. It’s the very first line on the profit and loss statement. For example, if you sell 1,000 products for $200 each, your total revenue is $200,000.

Gross revenue vs. net revenue

Gross revenue is the total amount you made before accounting for any discounts, returns, or expenses.

Gross revenue is also known as:

- Total revenue

- Total sales

- Gross sales

Net revenue is the money you make after deducting discounts and returns. Net revenue is also known as net sales.

Net revenue = gross revenue - discounts and returns

For example, if you sold $200,000 in merchandise—your total revenue—but you ran a sale and had some returns. The sale discounts were $10,000, and there were $5,000 in returns.

Your net revenue is:

Net revenue = Gross revenue - discounts and returns

Net revenue = $200,000 - $15,000

Net revenue = $185,000

Cost of goods sold (COGS)

Cost of goods sold (COGS) are the cost of materials and labor a company uses to make a product or service. It’s also known as cost of sales. The costs can include raw materials or direct wages for employees. But also certain overhead costs, such as utilities.

Gross profit

Gross profit is the money you make from sales after subtracting your cost of goods sold.

Gross profit = net revenue - cost of goods sold

For example, you make $185,000 in net revenue, but it takes you $125,000 to make all the products.

Your gross profit is:

- Net revenue: $185,000

- Cost of goods sold: ($125,000)

- Gross profit: $60,000

Expenses

Expenses of a business include all the costs to generate revenue. COGS are expenses that show up on the top part of the P&L before gross profit. Other expenses can be operating or non-operating.

Operating expenses

Operating expenses are the costs of running your business. While COGS are for making a product, operating expenses are the costs to support that process.

Operating expenses include:

- Rent

- Marketing costs

- Salaries for admin staff

- Depreciation

- Licensing fees

Non-operating expenses

Non-operating expenses are costs not part of your core operations. These include taxes, fines, legal fees, and interest. Non-operating expenses include anything that’s unlikely to happen again. For example, losses due to shutting down a business operation.

Income

Income is how much money you make in your business. There are two key types of income—operating and net income.

Operating income

Operating income is a business's income from its core operations. It excludes non-operating expenses, such as taxes or interest expenses. This type of income measures how well a company generates money from its main business.

Operating income = Gross profit - operating expenses

For example, your business has the following operating expenses:

- Rent: $10,000

- Salaries: $5,000

- Marketing $2,500

- Total: $17,500

Your gross profit was $60,000, and thus your operating income is:

- Gross profit: $60,000

- Operating expenses: ($17,500)

- Operating income: $42,500

Net income

Net income is your bottom line—the last item on your P&L. It's the money left after subtracting all expenses.

Net income = revenue - COGS - operating expenses - non-operating expenses

Net income comes after both operating and non-operating expenses on the P&L. It’s a measure of the money left over for shareholders or owners.

For example, you have $42,500 in operating income, $2,500 in tax expenses, and $5,000 in interest expenses.

Your net income is:

- Operating income: $42,500

- Taxes: ($2,500)

- Interest expenses: ($5,000)

- Net income: $35,000

How do you create a profit and loss statement?

The P&L will include three key components—revenue, expenses, and income. There are three key steps to making a profit and loss statement.