You could save up to 25% on transaction costs².

Speak with us now to see if you qualify.

Talk to sales 1-800-515-8366

Monday - Friday, 6 AM to 4 PM PT

Table of contents

Table of contents

What is an income statement?

To build an income statement for your business, first add up all your sales for the quarter. You might get a figure of $80,000. That looks healthy but when you add up your rent, payroll, supplies, and insurance, that comes to $85,000. Your income statement is telling you you lost $5,000.

Without this key financial report, you might not spot that loss in time before your payroll or taxes become due. Below, find out why income statements are important for small businesses and how to build one for your company.

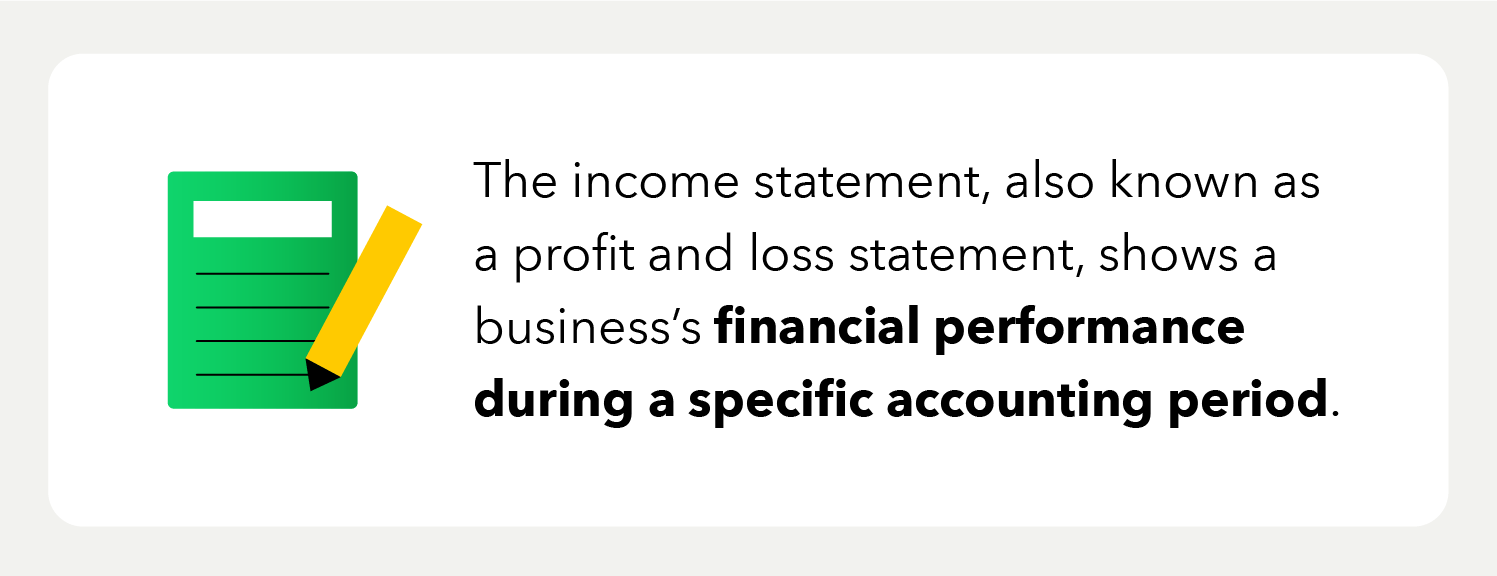

The income statement, also known as a profit and loss statement, shows how well a company has done during a specific financial accounting period. It reports net income by detailing a business’s revenues, gains, expenses, and losses. Put simply, an income statement follows this equation:

Total Revenue – Total Expenses = Net Income

You can also download our free income statement template to streamline the process or partner with a live bookkeeper to help you understand your company’s finances.

Business owners use income statements to tell them whether their business is making or losing money. Use quarterly or annual income statements to help you:

The income statement should be used in tandem with the balance sheet and cash flow statement. With insights from all three of these financial reports, you can make informed decisions about how best to grow your business.

Comparing income statements from different periods shows you whether your business performance is improving or declining. Place several statements side-by-side to spot seasonal patterns, measure the results of any changes you've introduced, and spot developing problems before they get serious.

Compare your company against other businesses in your industry to know how well you are doing. Your income statement shows what percentage of your revenue you keep as profit. If similar companies keep 40 cents of every dollar and you only keep 25, start looking at your pricing, your costs, or how you deliver your services to find out why..

Ask your accountant if they know your industry benchmarks or request published averages from your trade association. The IRS also releases industry-specific data through its Statistics of Income program.

Ask your accountant if they know your industry benchmarks or request published averages from your trade association. The IRS also releases industry-specific data through its Statistics of Income program.

An income statement provides a clear picture of your business’s financial position. There are several ways to use periodically generated income statements to more efficiently manage your business.

By generating income statements and other financial reports on a regular basis, you can analyze the statements over time to see whether your business is turning a profit. You can use this information to make financial projections and more informed decisions about your business.

Your bottom line shows whether you made a profit, but profit doesn't always mean you’ve got cash in the bank. You could have a profitable quarter and not have enough to pay your bills if customers are not paying you fast enough. Tracking your cash flow helps you avoid spending money your business has earned but not yet received.

Many small businesses need financial statements to apply for credit or to provide financial information to a potential lender. Using an income statement to demonstrate a consistent history of income and profitability can make this process easier.

Accurate accounting ledgers and records of expenses, revenues, and credits are required for tax purposes and can help keep you in compliance with tax regulations.

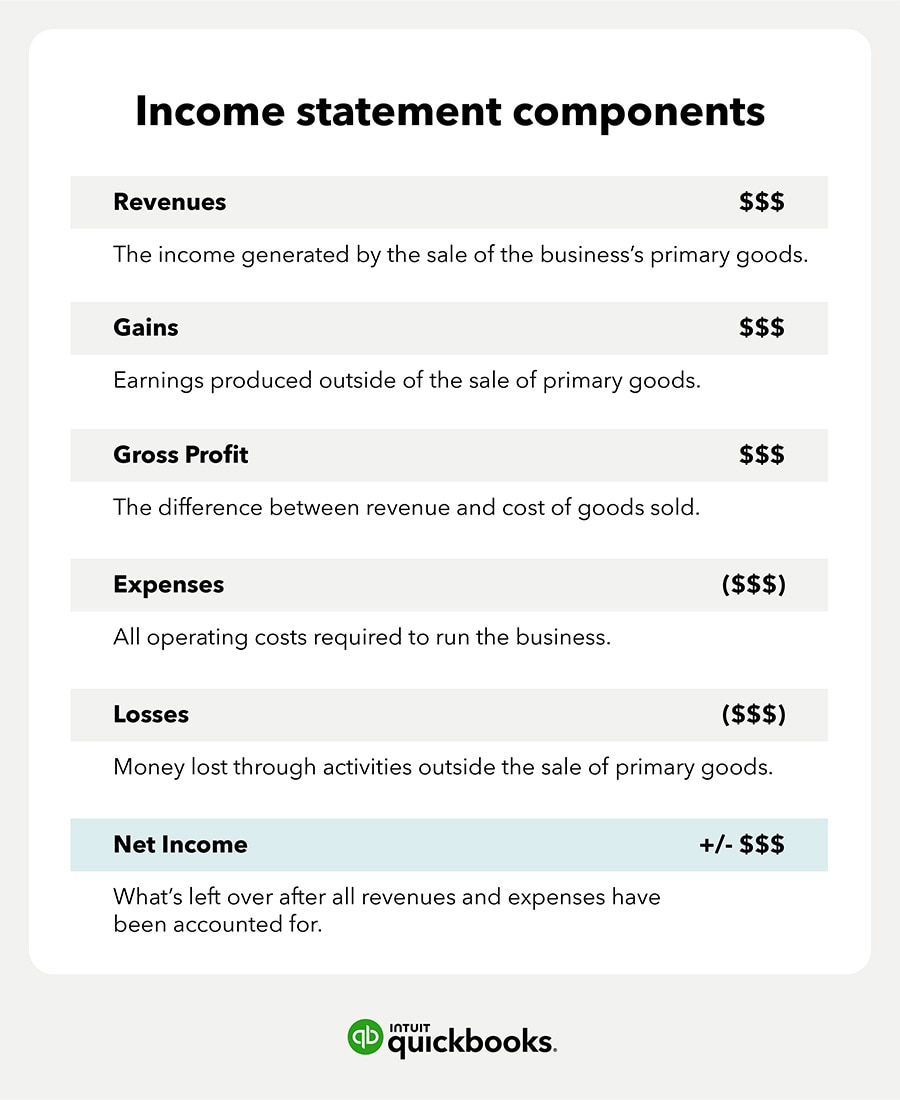

The elements of an income statement include revenues, gains, gross profit, expenses, losses, and net income or loss.

Revenue is all income generated by the sale of your goods or services. Revenue may also be referred to as the “top line,” because it is the first line on the income statement.

Gains are the earnings produced outside of the sale of your main goods or services. For example, selling off an asset can be categorized under gains.

Cost of goods sold is what your business pays to make or buy the products and services it sells. For a retailer, that means the wholesale price of your inventory. For a service business, it includes the labor and materials that go directly into delivering the work.

Gross profit is what's left of your revenue after deducting the cost of goods sold (COGS)—the direct costs related to producing goods or providing services.

Revenue – COGS = gross profit

Expenses are what your business spends to keep operating, separate from the direct cost of making or buying what you sell.

There are three types of an income statement:

The costs associated with producing your goods or providing services are not included in the expenses section of the income statement.

Losses include money lost through activities outside of transactions for your primary goods or services. For example, paying out a lawsuit settlement is considered a loss.

Net income—or loss—is what is left over after all revenues and expenses have been accounted for. If there is a positive sum (revenue was greater than expenses), it’s referred to as net income. If there’s a negative sum (expenses were greater than revenue during that period), then it’s referred to as a net loss.

Net income = (total revenue + gains) – (total expenses + losses)

Not sure if a cost is COGS or operating expenses? Ask yourself whether you would still have to pay it if you made no sales that month. If the answer is yes, it's an operating expense. If no, it's probably COGS.

Preparing financial statements can seem intimidating, but it doesn’t have to be an overwhelming process. We’ve broken down the steps for preparing an income statement, as well as some helpful tips.

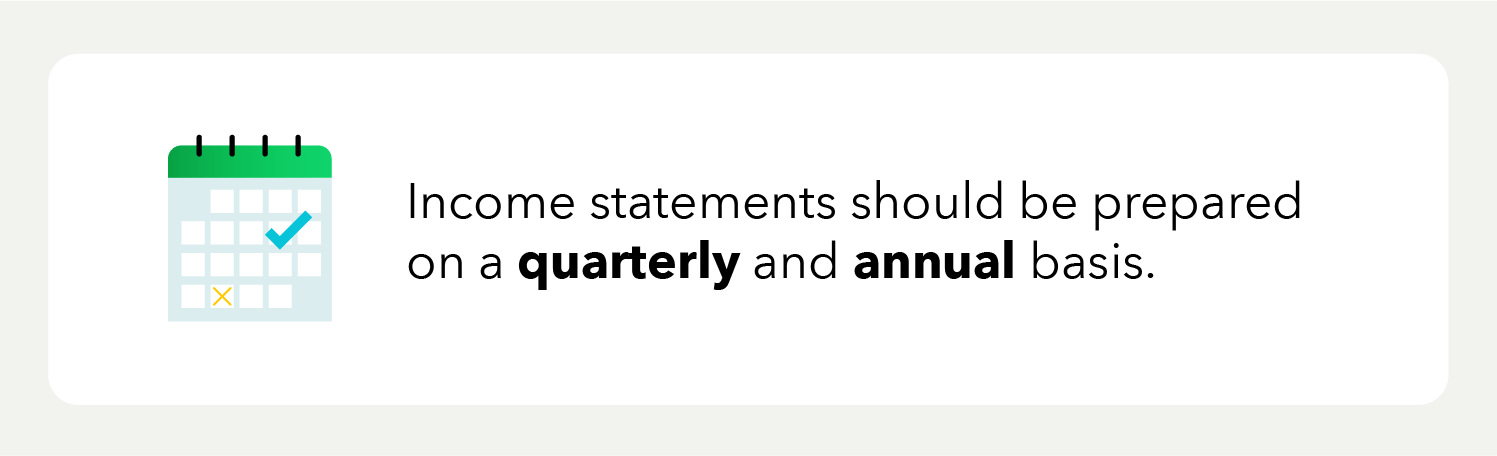

Income statements can be prepared monthly, quarterly, or annually, depending on your reporting needs. Larger businesses typically run quarterly reporting, while small businesses may benefit from monthly reporting to better track business trends.

A balance report details your end balance for each account that will be listed on the income statement and provides all of the end balances required to create your income statement. This can be done with accounting software, like QuickBooks Online.

You can begin your free QuickBooks Online trial today. You can also look at QuickBooks Online subscription levels and see a comparison of QuickBooks vs. Xero accounting software.

Add all your sales together for the reporting period to get your revenue. For the cost of goods sold, sum up all the direct costs of producing or buying everything you sold over the same period.

Every line on the income statement you are building from this point on depends on these two numbers being accurate.

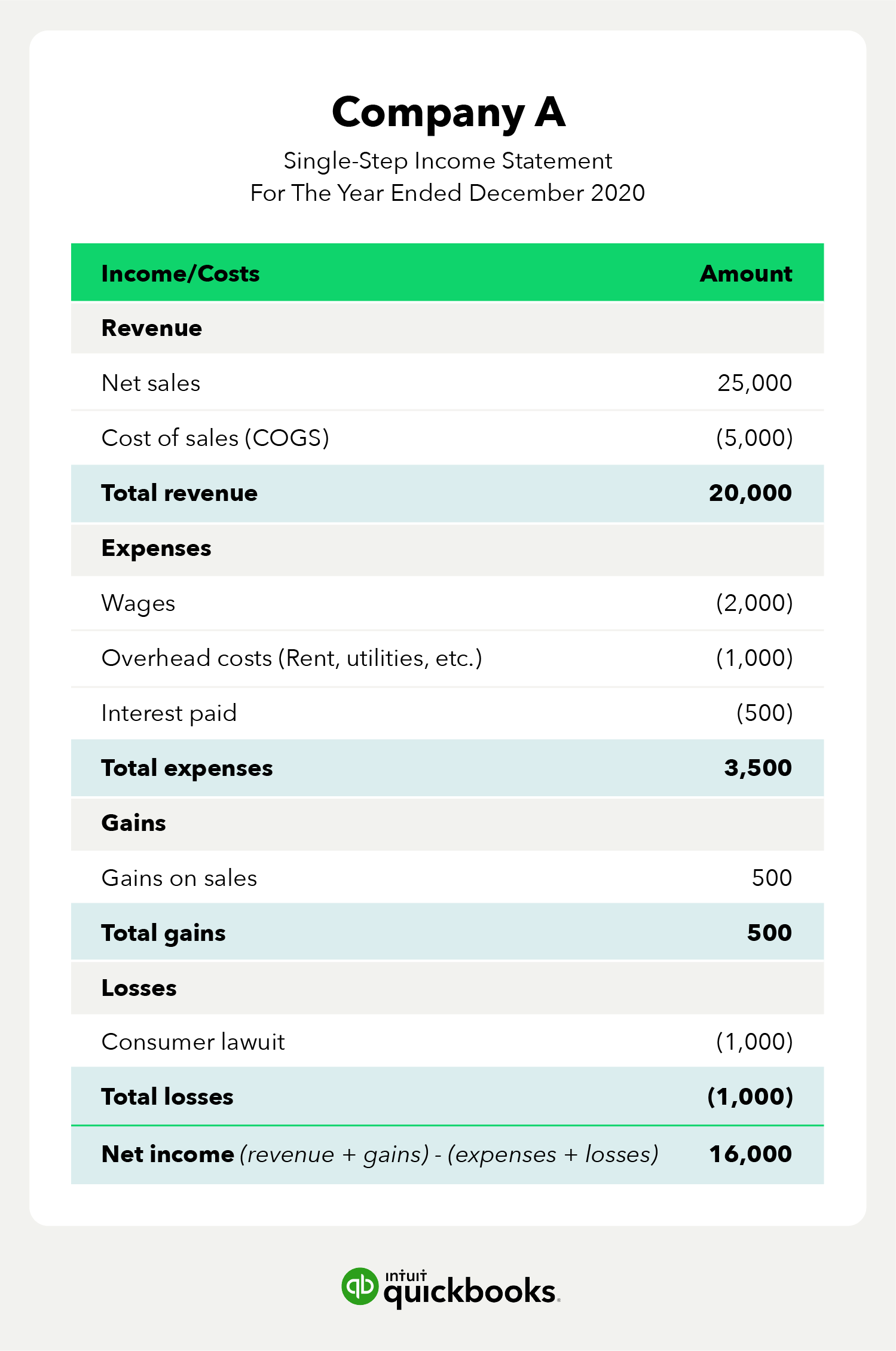

Single-step income statements can be used to get a simple view of your business’s net income. These take minimal time to prepare and don't differentiate operating versus non-operating costs.

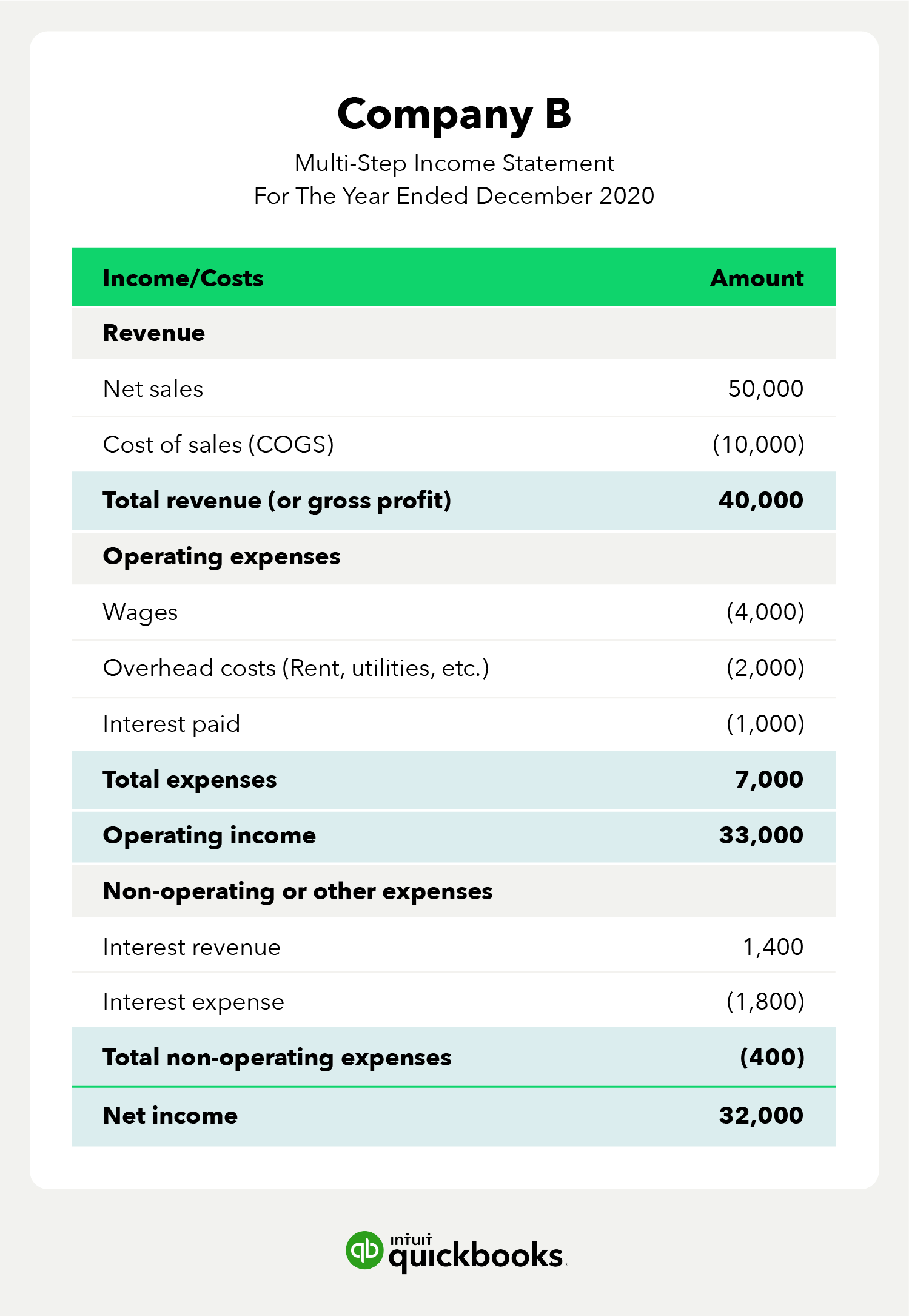

A multi-step income statement calculates net income and separates operational income from non-operational income—giving you a more complete picture of where your business stands.

Give your statement a final QA either manually or using an automated platform. Using software allows you to automatically track and organize your business’s accounting data so you can access and review income statements.

You can use Intuit Expert to get help generating income statements and other key financial reports.

**Products and features

**QuickBooks Free: Free is currently available at no charge and may be offered for a limited time. Features and availability, are subject to change or discontinuation at any time, with or without notice. If the Free plan is discontinued, we will notify you in advance and provide you with comparable options to transition to another QuickBooks plan that meets your business needs. Certain add-on products may be eligible for use with the Free plan. To utilize any add-on products, you must agree to additional terms and conditions, and limitations and fees for and any selected add-ons will apply.

Terms, conditions, pricing, special features, service and support options are subject to change without notice.

When deciding how you’d like to report your net income, it’s important to consider the pros and cons of both single-step and multi-step income statements.

Single-step income statements are the simplest and most commonly used by small businesses. But multi-step income statements are great for small businesses with several income streams.

For small businesses with few income streams, generating single-step income statements on a regular basis has three clear advantages:

If you have more than a few income streams or a complicated financial landscape, a multi-step income statement gives you a better view of your profits and losses. There are several ways it can benefit your small business:

Switch to a multi-step income statement when you need to see how each part of your business is doing on its own. That could be when you start selling different types of products or services, or a lender or investor wants to see a more detailed breakdown of your revenues.

The numbers behind your business are identical on both a single-step and a multi-step income statement. The only difference is how much detail you see.

A single-step income statement is a simplified approach to viewing your net profit or loss. Single-step income statements include revenue, gains, expenses, and losses, and they strictly show operating costs.

For single-step income statements, you need only one calculation: net income. To determine net income, you simply subtract all your expenses from total revenue.

Net Income = (Revenues + Gains) - (Expenses + Losses)

A multi-step income statement uses a more complex method of calculating net profit or loss.

It breaks your income into stages, so you can see your gross profit and operating income before you get to the bottom line. To prepare one, follow these three steps:

Subtract your cost of goods sold from your total sales to work out your gross profit. This shows you how much money you keep from revenue before any operating costs come out.

Gross profit = net sales – COGS

Subtract your operating expenses from your gross profit for your operating income, which is what your business earns from its day-to-day operations before interest costs and taxes.

Operating income = gross profit – operating expense

Add any non-operating income, like interest or investment returns, to your operating income. The result is your net income, which is the final measure of whether your business made or lost money for the period.

Net income = operating income + non-operating income

For EBITDA, add back depreciation and amortization to your operating income. Lenders and investors use it as a proxy for operational earning power, making it easier to compare profitability across businesses. Though it doesn't capture the full picture of cash generation since it excludes items like taxes, debt obligations, and capital expenditures.

Operating Income = Gross Profit – Operating Expenses

EBITDA = Operating Income + Depreciation + Amortization

Your income statement is one of three crucial financial statements your business needs, including the balance sheet and the cash flow statement. They serve different purposes:

The profit or loss on your income statement goes straight onto your balance sheet, and it appears as the starting point on your cash flow statement. A change in any one of them affects the other two.

Example: Your income statement might show a $20,000 profit for the quarter. But if your customers pay you on 60-day terms, your cash flow statement could show only $8,000 in cash coming in. Without checking both, you may take on a new member of staff or commit to a purchase you don’t have the money to cover yet.

No single statement gives you the whole picture of your business performance. You could be making a profit but running out of cash, or have money in the bank but be deeper in debt than you realize.

Example: Your income statement records a $10,000 profit for the quarter, increasing the retained earnings on your balance sheet. But your cash flow statement might show that $4,000 of it is available, as the rest is still in accounts receivable.

Start with your income statement first because it tells you whether your revenue is covering your costs. Then check your cash flow statement next to make sure the cash is there when payroll and bills come due. Finally, review your balance sheet to see what your business has and what it owes.

Income statements follow the same structure in every industry and sector, but what you include under revenue, COGS, and expenses depends on the type of business you run.

Service businesses like consulting firms and agencies generally have high gross margins because people are their main costs.

Sales revenue comes from fees earned or project-based billing. Because there's little or no inventory required when supplying customers, the cost of services replaces COGS on the income statement.

Key expenses include labor costs, software subscriptions (SaaS), and professional liability insurance.

Track your income statement by client or project to find out which work you actually make money on. It could be that your highest-grossing client has much higher labor costs, meaning the work is not as profitable as you might believe.

For retail and e-commerce businesses, COGS is the most important line on the income statement because it directly determines your gross profit margin.

Revenue is typically product sales, broken down by category, so you can see which products perform best. COGS calculations typically include raw materials, freight-in, and manufacturing labor.

Other important costs are shipping and fulfillment costs, marketplace fees to platforms like Amazon and Shopify, and advertising spend (ROAS).

Give marketplace fees their own line in your income statement. If they take 15% of your revenue and your margin is 20%, then check your competitors' pricing to see if there's room to increase what you charge to boost profits.

Manufacturing and construction businesses have more complex income statements because of overhead allocation and work in progress (WIP).

Their revenues may come from progress billings or completed contract sales, depending on when firms recognize revenue across what can be long-term projects. COGS includes direct materials, direct labor, and factory overhead, often calculated using absorption costing.

Key expenses in manufacturing and construction include equipment depreciation, maintenance, and safety compliance costs.

Review your work in progress at the end of each quarter. If you've billed a customer for 60% of a project but only completed 40% of the work, your income statement will look healthier than it is. When the bills catch up with the work, you could finish the project at a loss.

SaaS and subscription businesses track recurring revenue, split into monthly recurring revenue (MRR) and annual recurring revenue (ARR).

Key costs include:

R&D costs tend to run higher in tech businesses than in other industries, and depending on how a company structures its reporting, they may appear as an operating expense or separately after operating income.

Compare how much you spend on advertising to get a new customer in. If your CAC is $500 but you only charge $50, it will take 10 months to earn that back in revenue. If your profit margin is 50%, only $25 of each payment is profit, and it will actually take 20 months.

An income statement is a valuable tool for guiding your business’s financial decisions. While you can prepare income statements on your own, accounting software can help provide simplicity and accuracy.

With Intuit Expert Assisted Bookkeeping,you get on-demand coaching from bookkeeping experts on the best ways to manage your finances, cash flow, and taxes. Use their insights to make more confident decisions as your business grows.

Call Sales: 1-800-285-4854