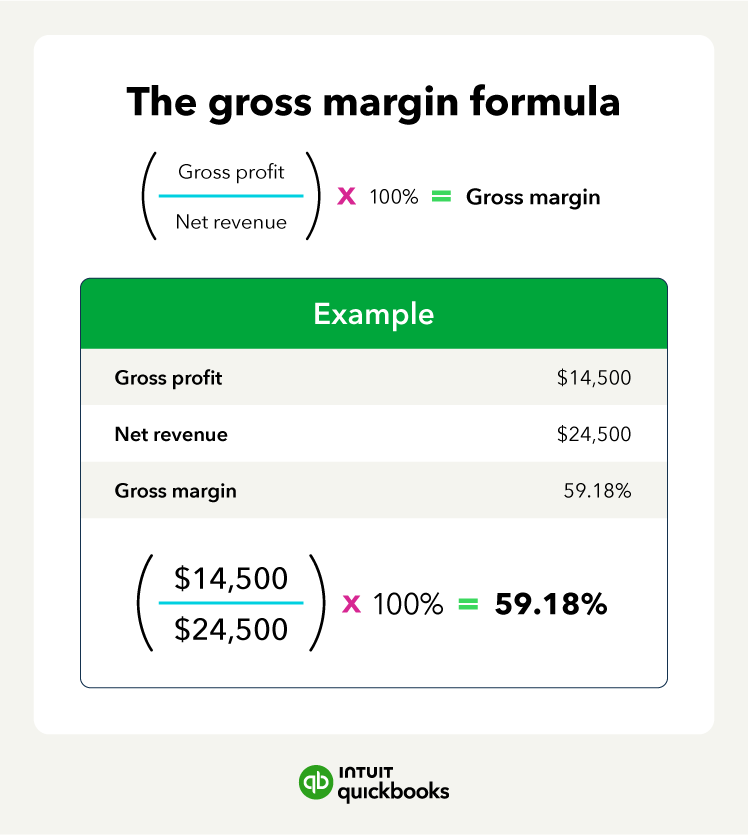

Gross margins can be thought of as Wholesome Bean Coffee Co.’s “efficiency score” for their core product: how effectively they are turning revenue into profit. The higher the gross margin, the higher the efficiency, and the higher the profit.

Generally speaking, gross margins between 50% and 70% are ideal and achievable.

3. Manage operating expenses

Now that the gross margin calculation is complete, Wholesome Bean Coffee Co. needs to return to the gross profit calculation ($14,500) to figure out its operating income.

Operating income is the amount left over after fixed and variable costs, such as rent, marketing expenses, and insurance fees, are deducted from gross profit.

Let’s say that Wholesome Bean Coffee Co. pays $3,000 in rent each month, spends $1,000 toward marketing, and pays $4,000 for insurance.

First, Wholesome Bean Coffee Co. will add its individual fixed costs together to find its total fixed cost.

Formula:

Fixed Cost A + Fixed Cost B + Fixed Cost C… ect. = Total Fixed Cost

$3,000 + $1,000 + $4,000 = $8,000

Then they will subtract total fixed costs from gross profit to find operating income.

Formula:

Gross Profit - Total Fixed Costs = Operating Income

$14,500 - $8,000 = $6,500

This number shows the owner whether their business is sustainable, excluding large, one-off expenditures such as taxes or loan repayments.

4. Arrive at net income

Finally, Wholesome Bean Coffee Co. is ready for the moment of truth: calculating net income. To find the actual take-home pay the owner received in March 2026, the last thing that needs to be deducted are the non-operating expenses.

As with fixed costs, Wholesome Bean Coffee Co. will add together its other monthly expenses. For example, $300 in interest on an equipment loan and $1,200 in estimated taxes.

Formula:

Expense A + Expense B… ect. = Total Non-Operating Expenses

$300 + $1,200 = $1,500

This total is then subtracted from the operating income to reveal Wholesome Bean Coffee Co.’s net income for the month.

Formula:

Operating Income - Total Non-Operating Expenses = Net Income

$6,500 - $1,500 = $5,000

This $5,000 in net income is how much the owner of Wholesome Bean Coffee Co. made in March. In effect, it is the amount of money they can pay themselves and take home that month, or reinvest in their business. If the owner can live comfortably on that amount while meeting their growth targets, the business is in good shape.