According to a QuickBooks survey, only 16% of new small business owners have a business degree or similar qualifications. The rest of us learn as we go, which makes good advice all the more valuable.

Whether you’re starting as a solopreneur or you’ve secured backing and are ready to start building your team, this guide will help you grow your business with confidence.

Below, check out our comprehensive, user-friendly checklist of 17 essential steps you need to know to start up a successful business.

Jump to:

- 1. Define your vision + AI ethics statement

- 2. Research your market opportunity

- 3. Write a business plan

- 4. Create and register your business name

- 5. Perfect your multi-channel pitch

- 6. Determine your business structure

- 7. Investigate your legal requirements

- 8. Apply for permits and business licenses

- 9. Understand your startup cost

- 10. Open a small business bank account

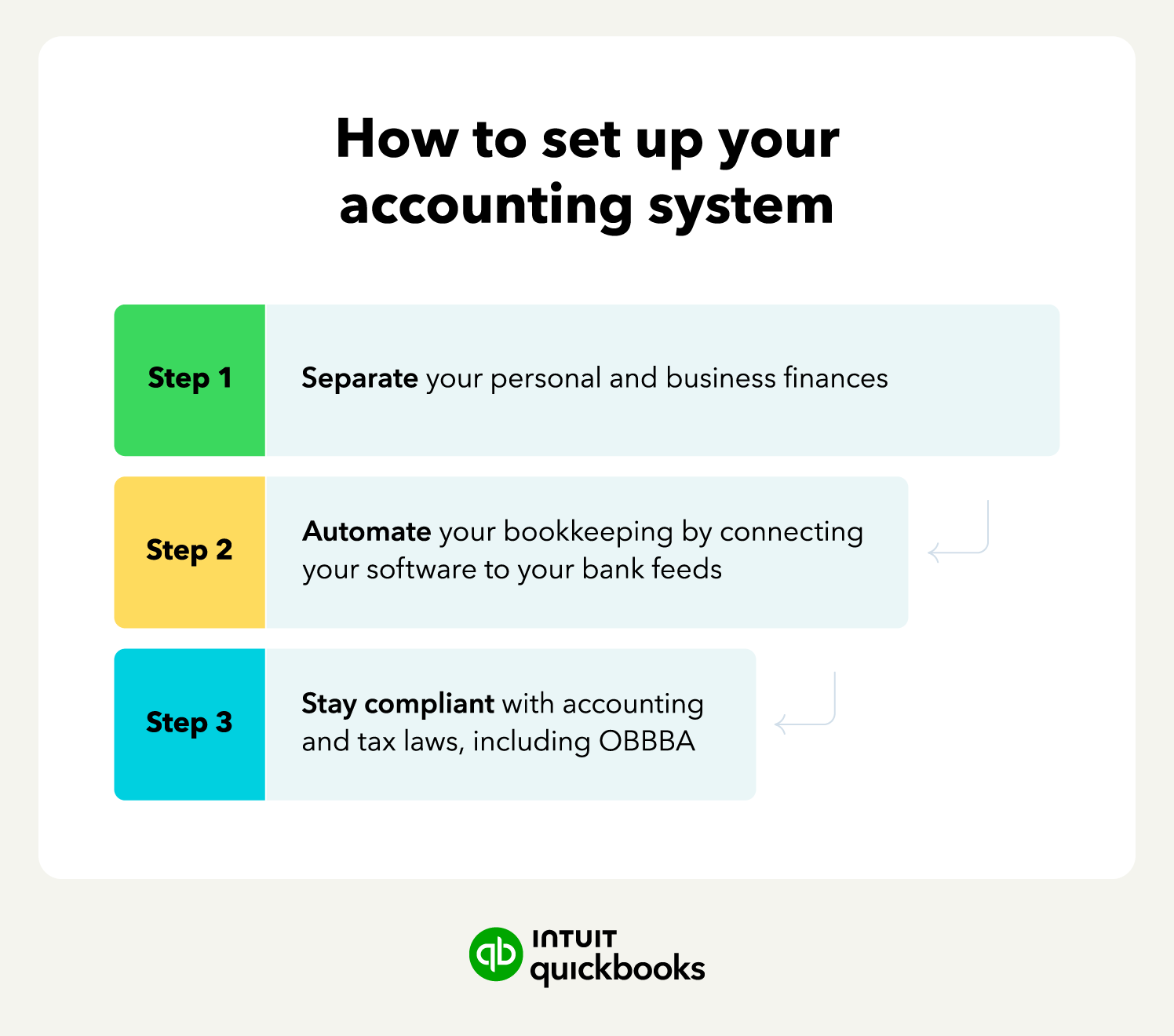

- 11. Set up OBBBA-compliant accounting systems

- 12. Activate your accounting AI agent

- 13. Outsource essential functions

- 14. Learn how to pay employees

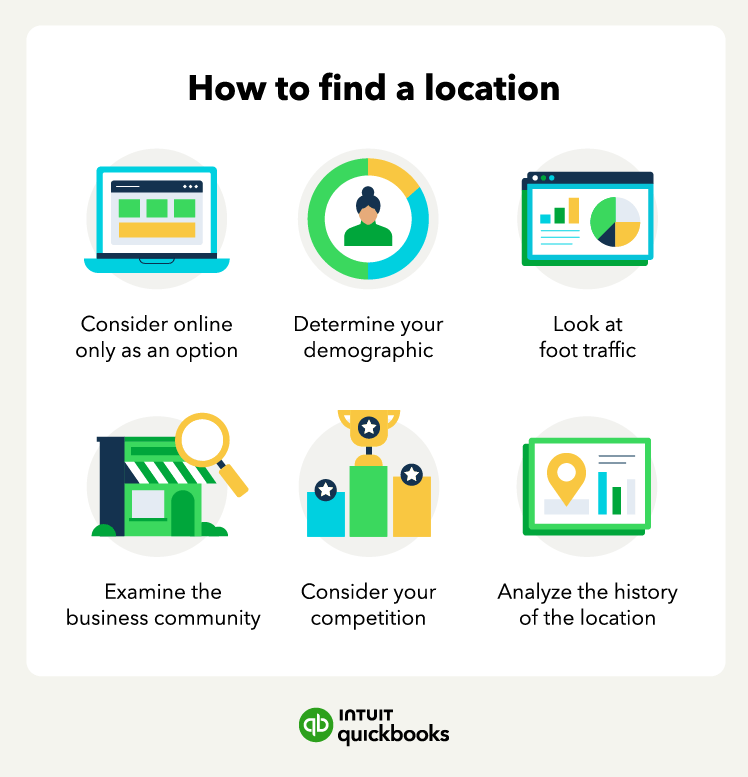

- 15. Find a business location

- 16. Launch a community-first website and ecosystem

- 17. Market via authentic human voice video

- Start your business with confidence