You could save up to 25% on transaction costs².

Speak with us now to see if you qualify.

Talk to sales 1-800-515-8366

Monday - Friday, 6 AM to 4 PM PT

Table of contents

Table of contents

You're making lots of sales, but you often find that when payroll or a supplier bill comes due, you don't have the cash on hand to settle up. Poor cash flow could be the reason, as it is for 45% of small businesses, according to a recent QuickBooks Small Business Insights survey.

Manage your business cash flow well, and you're better able to cover your costs, hold money back to ride out slow months, and see when there's enough to hire or invest. This article explains what cash flow is, how to calculate and analyze it, and where to start improving it.

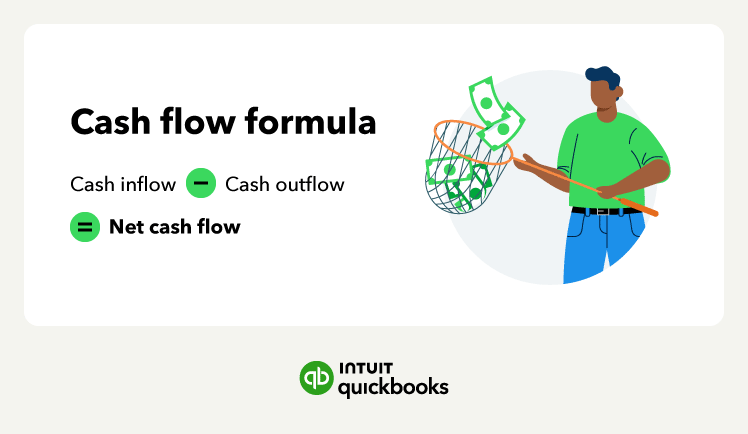

Cash flow is the money that moves in and out of your business over a set period. Cash comes in when customers pay you, and it goes out when you pay rent, restock inventory, or run payroll.

The difference between the two is your net cash flow. Positive cash flow means you’ve taken in more money than paid out, while negative cash flow means the opposite.

Good cash flow management helps you avoid cash shortfalls and make confident decisions based on the money you actually have.

Profit is what's left after you subtract your costs from your revenue, while cash flow is the money that enters and leaves your business.

The difference is in timing. You earn revenue when you make a sale, but only receive the cash when the customer pays up.

Say your business invoices $20,000 in sales on net-60 days. This means the bill is not due to the customer for 60 days from the invoice date. While you wait for money from your customers, you still have to pay your rent, suppliers, and wages.

A business that’s profitable on paper can fail because of poor cash flow timing.

The profit formula is Total Revenue – Total Expenses = Profit. The basic cash flow formula is Cash In – Cash Out = Net Cash Flow.

One measures what you've earned, the other what you've actually received.

There are three types of cash flow—operating, investing, and financing. They account for the different ways your business earns, spends, or raises money.

Operating cash flow (CFO) is the money your business brings in and pays out through everyday trading. That includes receiving payments from customers, buying in stock, covering rent, and meeting your wage bill.

Positive operating cash flow means your business generates enough money from its own operations to keep running without needing outside funding like SBA 7(a) loans.

Calculating your operating cash flow starts with net income. From there, add back noncash expenses like depreciation and adjust for changes in working capital. The formula is:

Operating Cash Flow = Net Income + Noncash Items + Working Capital Changes

Working capital is your current assets, less your current liabilities. This formula adjusts the accrual accounting items—accounts receivable, accounts payable, and inventory—to a cash basis.

Investing cash flow (CFI) is the money your business spends or receives on long-term assets, like equipment, vehicles, and property.

For example, buying a new pizza oven for your bakery is an investing cash outflow. Selling a delivery van you no longer need is an investing cash inflow.

Negative investing cash flow isn't always a bad sign. It often means your business is spending on things that will help it grow, like upgrading machinery or moving to bigger premises.

You calculate it like this:

Investing Cash Flow = Cash Inflows from Investment Activities - Cash Outflows for Investment Activities

Fixed assets, such as a vehicle or machinery, are those you plan to use for a long time. Buying equipment is an investing cash outflow. Selling some of your fixed assets would be an inflow.

Financing cash flow (CFF) is the money that comes in or goes out related to external funding. External funding includes business loans, lines of credit, SBA loans, or investment from a partner or backer.

For example, if you take out a loan to fit out a commercial kitchen for your restaurant, the cash you receive is a financing inflow. The monthly repayments you make are a financing outflow. Positive CFF means you've brought in more funding than you've paid back, while negative means the opposite.

Here’s the formula:

Financing Cash Flow = Cash Inflows from Financing Activities - Cash Outflows from Financing Activities

If you’re applying for finance, lenders look at your financing cash flow to see how your business manages its borrowing and repayments when making a decision.

The quick ratio tells you whether your business has enough cash and near-cash assets (like outstanding invoices and investments you can sell quickly) to pay its short-term bills right now.

The basic formula for working out your cash flow is:

Cash Flow = Cash Inflows − Cash Outflows

How you get to that figure depends on the type of accounting your business uses.

The direct method tracks every dollar in and out as it happens. So, you record customer payments received, rent paid, and wages paid in real time.

The indirect method starts with your net income—your total revenue minus all expenses. You then adjust it to account for:

Either way, you see exactly how much cash came in and went out over a specific period.

Running a statement every week or month helps you spot cash flow issues before they become urgent. QuickBooks can do this automatically by pulling the numbers straight from your bank and sales data.

The direct method is also known as cash accounting, where you record transactions when money changes hands. In accrual accounting, you record income when you invoice and expenses when you receive the bill, regardless of when cash actually arrives.

Say you run a small bakery. In a typical month, you take in $8,000 from customer payments, while your outgoings, including your rent, payroll, ingredients, and utilities, come to around $7,000.

A positive net cash flow of $1,000 means your business has more cash on hand at the end of the month than it started with. A negative result would mean you spent more than came in and need to cover the gap from savings, purchasing on credit, or accessing finance facilities like loans or credit cards.

Bear in mind that $8,000 in sales doesn't always mean $8,000 in cash received. $6,000 may have come from customers who paid at the time of order, with the remainder still outstanding on invoices.

If that's the case, your actual cash flow is lower than your sales figures suggest, so keep an eye on what you’ve invoiced versus what's actually landed in your account.

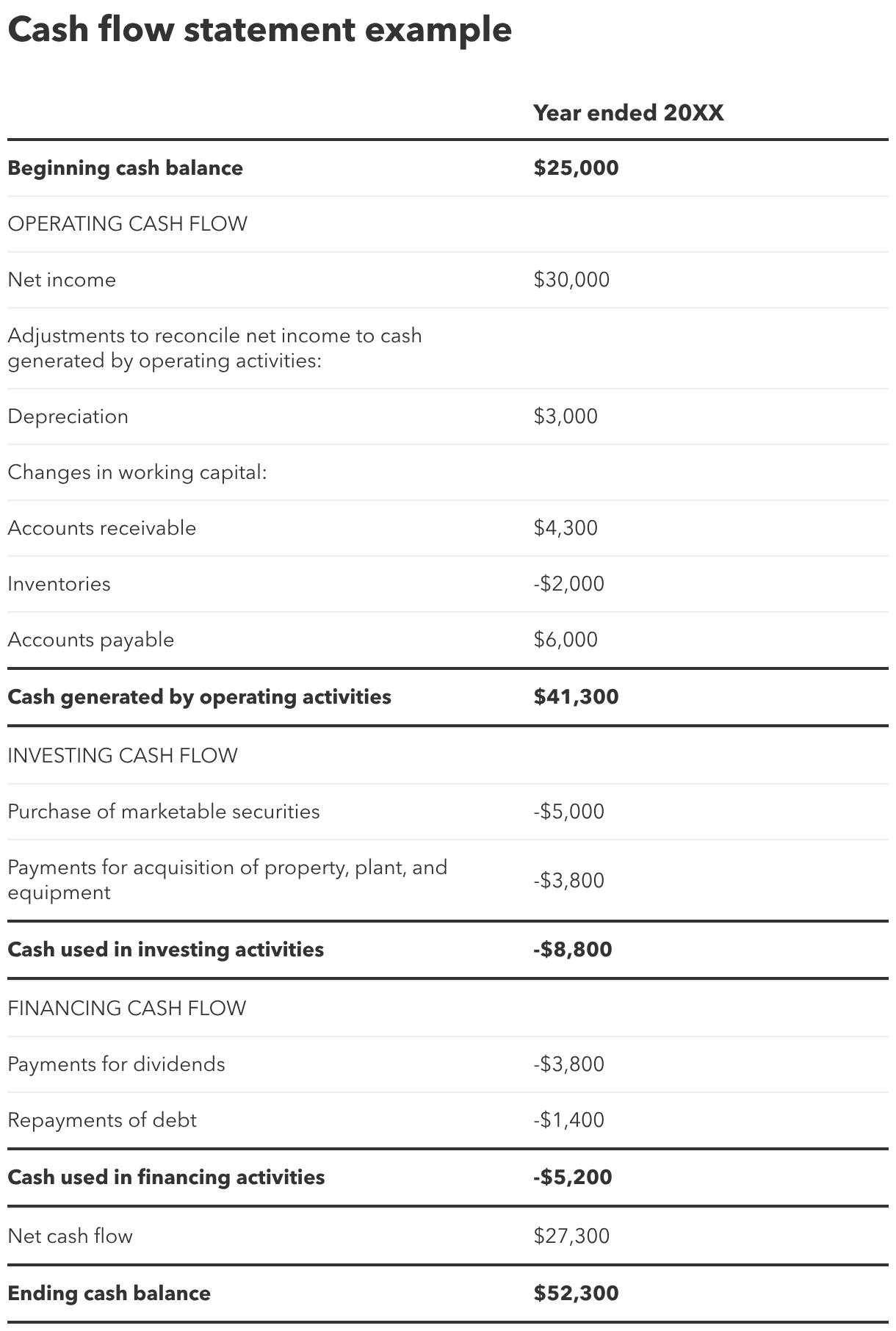

A cash flow statement shows where your money came from and where it went over a set period. You can create a general statement for a high-level overview or break it down by operating, investing, and financing. It's one of three key financial documents for your business, alongside the profit and loss statement and the balance sheet.

Below, you’ll see a cash flow statement example.

Analyzing your cash flow regularly allows you to spot patterns over time. One good or bad month doesn’t mean your business is healthy or unhealthy. Think of it more as tracking the direction of your business over several months.

These key metrics help you assess how your business is performing:

Free cash flow is the money left over after you've covered your running costs and paid for any big purchases like equipment or vehicles.

To calculate free cash flow, the formula is:

Free Cash Flow = Operating Cash Flow – Capital Expenditures

Say your bakery brings in $5,000 in operating cash flow this month and you spent $1,500 on a new display counter. Your free cash flow is $3,500, which you can save, put back into the business, or pay yourself with.

Operating cash flow ratio tells you whether the cash coming in from everyday trading will cover bills that are due or coming up soon.

To work out your operating cash flow ratio, the formula is:

Operating Cash Flow Ratio = Operating Cash Flow ÷ Current Liabilities

Above 1 means you're covered, but below 1 means you may need to borrow or use your savings.

For instance, your bakery generates $5,000 in operating cash flow and the upcoming bills, like utilities, supplier invoices, and loan repayments, total $4,000. Your ratio is 1.25, so for every $1 you owe, you’re bringing in $1.25.

Cash flow margin is the amount of cash you keep for every dollar in sales, after you've covered day-to-day costs.

Here’s how to work it out:

Cash Flow Margin = Operating Cash Flow ÷ Net Revenue × 100

For example, your bakery takes $20,000 in sales (or net revenue) a month and has $4,000 left in operating cash flow. Divide $4,000 by $20,000 and multiply by 100, and this gives you a cash flow margin of 20%.

That means you keep 20 cents for every $1 in sales. Track this month by month to see whether you're keeping enough of what you sell, or whether bills, stock, or late-paying customers are eating into your cash.

Comparing this with your income statement, which shows your total revenue and expenses over the same period, helps you see which costs are taking the biggest share.

Even small changes in how you run your business can free up more cash to grow your company, pay your bills, and get through slower months. Try these cash flow management tips:

The sooner you send an invoice after you've delivered goods or services to a customer, the sooner you get paid. QuickBooks' AI-powered invoice generator can create and send professional invoices in seconds, so you can get paid faster.

Every time a client orders, make sure they know the payment terms upfront so they know when the bill is due. Offer multiple payment options, such as credit and debit card, AutoPay, and ACH, so customers can pay whichever way is easiest for them.

If a customer is late paying up, QuickBooks' payments AI agent can send reminders automatically, so it does the chasing for you..

Review your recurring expenses every quarter and cancel any subscriptions or services you're no longer using.

It’s also a good idea to check your inventory management strategy too, to make sure you’re not tying up cash you could use somewhere else in excess stock. Try negotiating better payment terms with vendors. Paying in 45–60 days instead of 30 keeps cash in your account for longer.

The key is cutting costs that free up more cash without hurting your ability to grow. Dropping an unused software subscription is good, but cutting your marketing budget generally isn’t, unless it’s on campaigns that don’t bring in enough customers.

Cash flow forecasting means projecting what your inflows and outflows will be over a period of time, like one month to one quarter. This forward look gives you the chance to spot shortfalls before they happen.

You can plan for large upcoming expenses like equipment purchases or tax bills, and decide whether you can afford to hire.

QuickBooks Cash Flow Planner can build a forecast from your existing data, so you don't have to start from scratch with a spreadsheet. Some versions also include AI-assisted insights to help you see what's coming.

A cash reserve of 3 to 6 months of operating expenses gives you a buffer for slow periods, so you don't have to take on high-interest debt or max out a credit card to cover any shortfall.

Set up an automatic monthly transfer into a dedicated savings account and build it up gradually. Even a small amount each month adds up over time.

Real-time visibility matters. Catching a cash gap two weeks out gives you time to act, but catching it the day of payroll is a crisis.

Connecting your bank accounts to your accounting software gives you a live view of your cash position without having to log into your bank account multiple times a day to check your balance.

The QuickBooks dashboard puts your cash flow, outstanding invoices, and upcoming bills in one place. You can see at a glance what's been paid, what's overdue, and what's coming up.

Good inventory control means knowing exactly what you have, what's selling, and what's sitting on the shelf. Stock up on the lines you know customers want and be cautious when testing new products, as unsold inventory is cash you can’t put to work.

Cash flow problems often start small, but late invoices and unexpected expenses can build up over time. This can leave you short when a payroll or a supplier bill comes due. Take control of your cash flow so you have the funds to cover your bills, expand your business, and see it through leaner periods.

QuickBooks Money lets you send invoices clients can settle instantly by card, ACH, or digital wallet, and you receive the funds the minute they pay. Start your free trial now.

Call Sales: 1-800-285-4854