How to improve your working capital

If your working capital analysis reveals problems, don't panic. There are several strategies you can implement to strengthen your position.

Increase current assets

Boosting the assets side is usually the quickest way to improve liquidity. The goal is to bring more cash in (or free it up) without adding new short-term pressure.

Start by speeding up collections. Send invoices right away, follow up on overdue accounts, and consider an early-payment discount if it helps customers pay faster.

Next, look at inventory. If you have slow-moving stock, trimming it down and improving turnover can unlock cash you didn’t realize was stuck on the shelf.

You can also convert other assets to cash. Selling unused equipment or excess inventory can give you an immediate boost.

Finally, increase sales while keeping margins in mind. Revenue growth helps most when it’s profitable and doesn’t create a bigger cash gap.

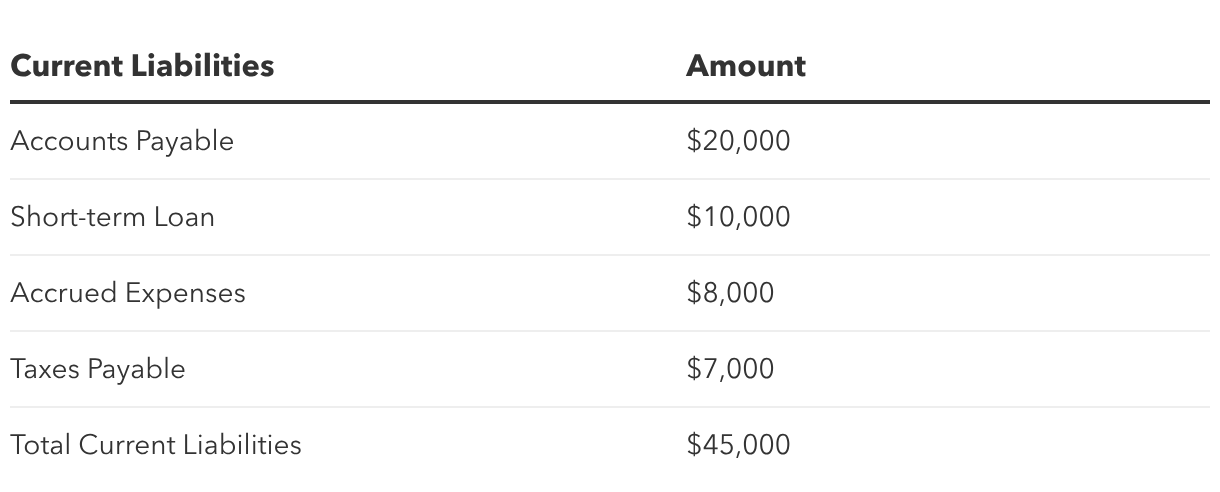

Decrease current liabilities

Managing what you owe matters just as much as managing what you own. Here, the goal is to reduce near-term pressure without damaging relationships or credit.

One lever is better payment terms. If you can move from net 30 to net 45 or net 60, you give yourself more room to operate.

You can also refinance short-term debt when it makes sense. Shifting payments into a longer-term structure can lower monthly strain (even if the total cost changes).

Another step is to pay strategically. Pay bills on time, but avoid paying early unless there’s a discount worth taking.

And if expenses are creeping up, look for ways to cut operating costs without hurting quality or delivery.

Improve cash flow management

Working capital problems usually show up first in cash flow. Proactive cash flow management helps you spot issues early, not when you’re already behind.

Start with cash flow forecasting. Even a basic weekly or monthly forecast can help you see shortfalls coming and plan ahead. It also helps to have a line of credit in place before you urgently need one. It can be a backstop for slow seasons or unexpected expenses.

Also, don’t forget pricing. A quick pricing review can confirm your margins are strong enough to cover costs and still generate real cash.

Lastly, automate billing and collections where you can. Reminders, recurring invoices, and easier payment options can reduce delays and smooth out cash coming in.