Late payments are more than just frustrating—they can damage a small business. In fact, 82% of small businesses fail due to mismanaged cash flow.

Businesses need a steady stream of income, and when customers are late on invoices, it can throw a major wrench into operations. You must pay lenders and employees on time. If you don’t have the funds to satisfy your obligations, you risk expensive late fees, compounding interest, labor lawsuits, and a tarnished reputation.

It’s crucial that your customers make timely payments, but what happens when they don’t? If you value their business, you’ll need to be cautious and ensure your attempt to collect payment doesn’t come off aggressive.

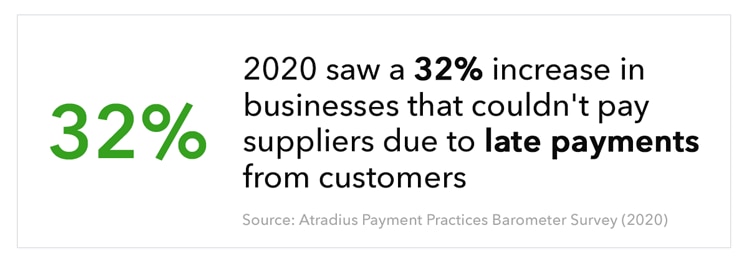

2020 has seen a 32% increase in the number of businesses that could not pay suppliers due to customers’ late payments, says a recent Atradius survey. To avoid adding to the statistic, those with delinquent accounts must know that you’re serious.

If you’re not sure how to ask customers to settle an invoice professionally, use this guide to learn how to collect outstanding payments. Plus, learn how to handle your accounts receivable, so you can better manage cash flow and keep your business in the black.