Cash vs Accrual Accounting? What are the main differences a business should know in 2026

Your accounting method has a significant impact on your small business, including your cash flow, tax management, and overall financial health. For many, the choice boils down to two primary methods: cash basis accounting and accrual accounting.

While these may sound similar, the difference between cash accounting and accrual accounting is significant, and picking the right one may even help you save money.

In fact, a 2025 QuickBooks survey revealed that 45% of small business owners believe they've lost at least $10,000 in profits due to low financial literacy, highlighting the importance of being well-informed.

This guide will help you navigate both accounting methods and understand why you should choose one over the other. We’ll explain the basics of the cash accounting and accrual accounting methods, as well as the pros and cons of each, so that you can make an informed decision.

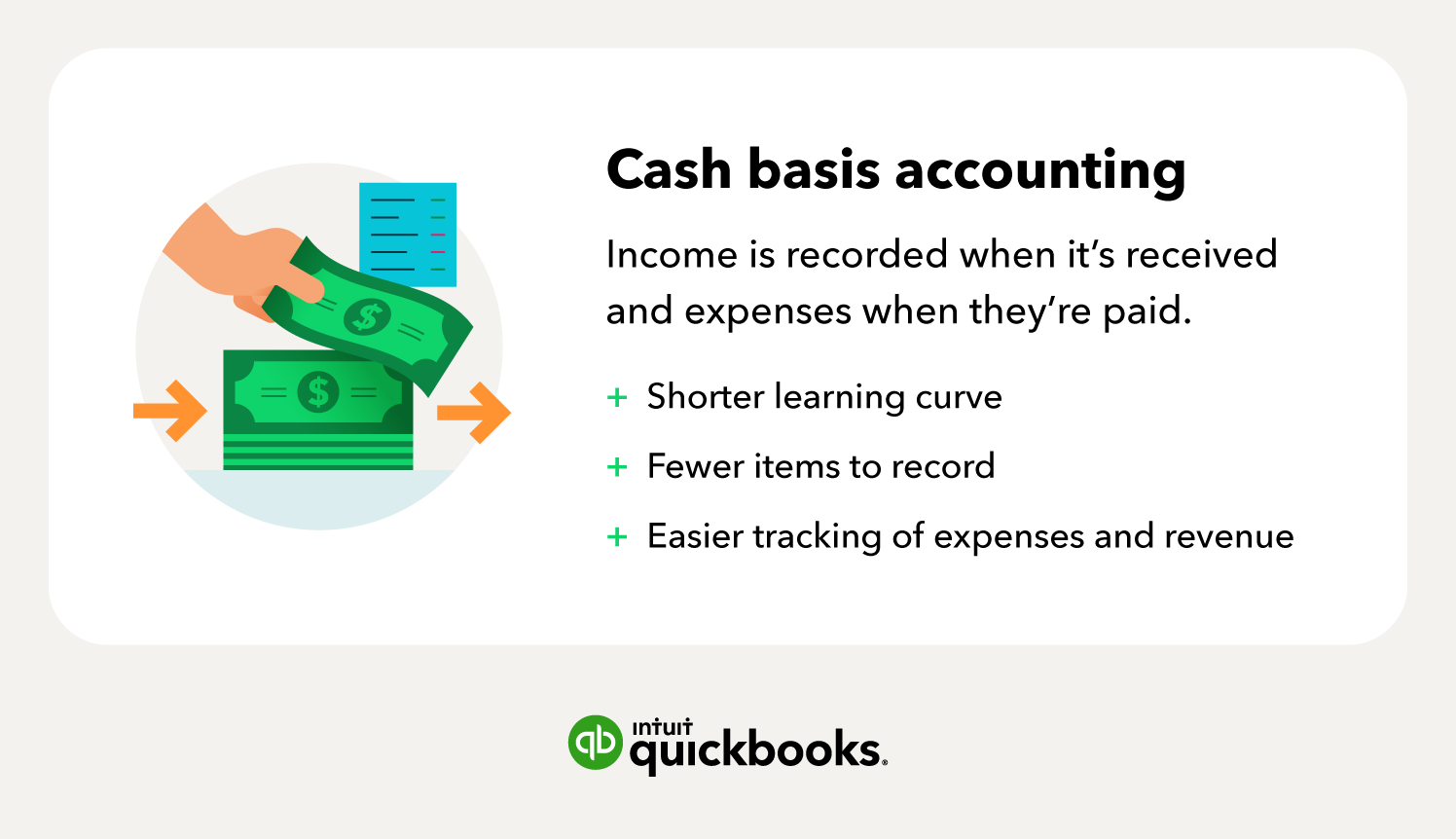

What is cash basis accounting?

Let’s begin with cash basis accounting. With this method, you record income as it’s received and expenses as they’re paid. Cash basis accounting only records your expenses when money leaves your account to pay suppliers, vendors, and other third parties.

In other words, if you have a small stationery business that purchased paper supplies on credit in June, but didn’t pay the bill until July, you would record those supplies as a July expense.

It’s important to note that this method does not take into account any accounts receivable or accounts payable. This is because it only applies to payments from clients—in the form of cash, checks, credit card receipts, or gross receipts—when payment is received.

Who uses cash basis accounting?

Because of its simplicity, many small businesses and sole proprietors use the cash basis method as their primary method of accounting. If your business makes less than $25 million in annual sales and does not sell merchandise directly to consumers, the cash basis method might be the best choice for you.

Some of the benefits include:

- Shorter learning curve

- Fewer items to record

- Easier tracking of expenses and revenue

Example of cash basis accounting

If you invoice a client for $1,000 on March 1 and receive payment on April 15, you would record the income as received for April, since that’s when you had the money in hand. Under this method, the timing of the payment, not the invoice date, determines when you record the income.

So the breakdown looks like this:

- The invoice is sent for $1,000 in March

- You do nothing in March

- You receive payment in April

- You record the income in April

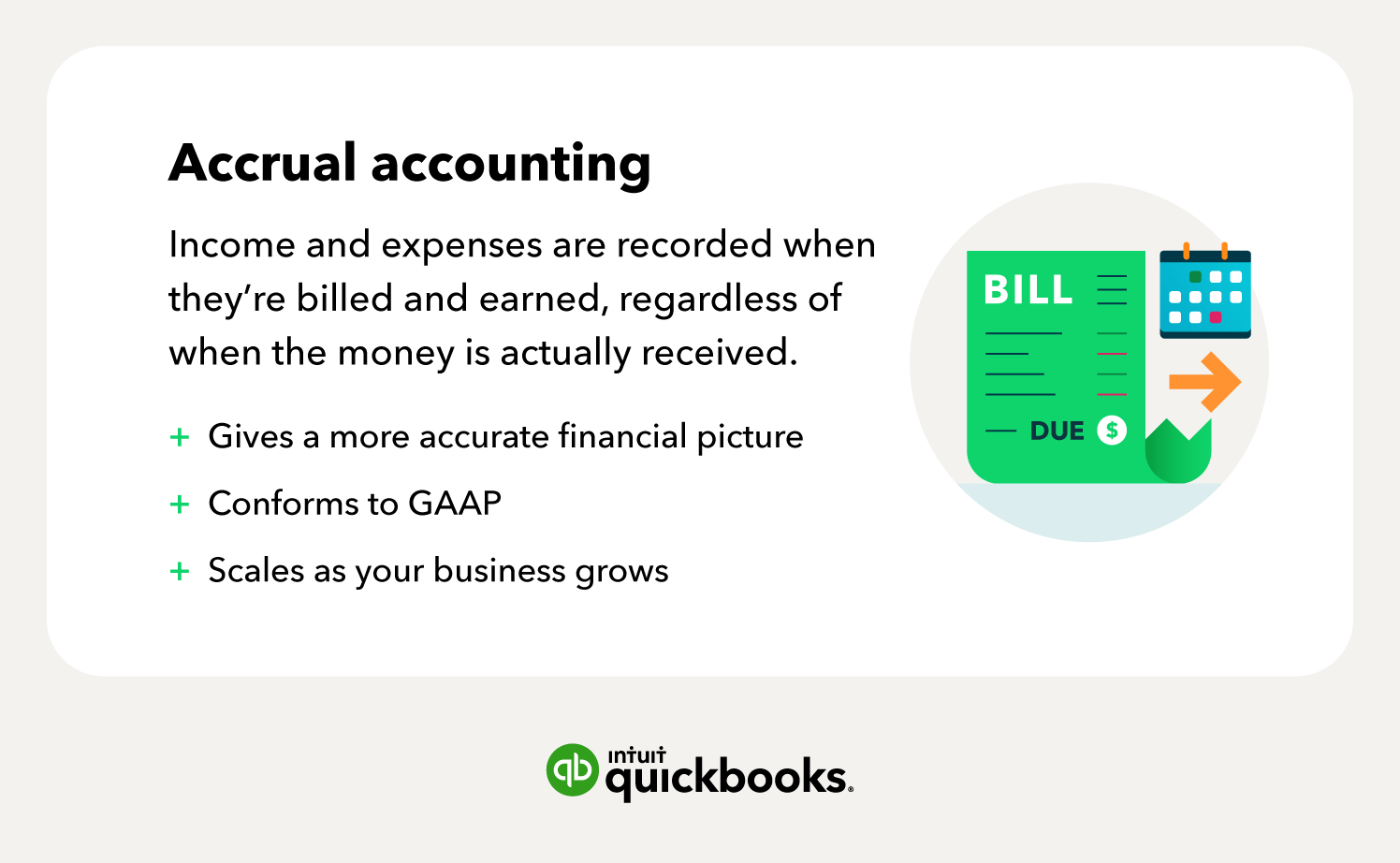

What is the accrual method of accounting?

With the accrual accounting method, income and expenses are recorded when they’re billed and earned, regardless of when the money is actually received. Accounting standards outlined by Generally Accepted Accounting Principles (GAAP) stipulate the use of accrual accounting for financial reporting, as it provides a clearer picture of a company’s overall financial position.

Who uses accrual accounting?

While it’s perfectly acceptable for small businesses to use accrual accounting as their primary method of accounting, it’s not required.

However, according to GAAP regulations, any business that is either publicly traded or produces over $30 million in sales revenue over a three-year period is required to use the accrual method.

Example of accrual accounting

Using the example from above, if a small business bills a client $1,000 on March 1, you would record that $1,000 as income in March’s bookkeeping—even if the funds didn’t clear your account until April 15.

- The invoice is sent for $1,000 in March

- You record revenue in March

The same principle applies to accrued expenses. In this case, if your small stationery business buys paper supplies on a credit card in June, but doesn’t actually pay that bill until July, you would still record that as a June expense. Let’s break this down:

- You bought paper supplies in June

- You record the expense in June

This method matches revenues and expenses in the period they occur, providing a more accurate view of your business's financial performance for that specific time frame. A financial accounting AI Agent can further streamline this process, as the AI analyzes your financial data to automatically create forecasts and highlight variances to help you stay on track to your goals.

Accrual vs. cash basis: Which is better?

Accrual accounting is the winner if you’re looking solely at popularity, as it’s the most widely used as well as the most accurate when it comes to portraying a holistic view of a company's financial health. Cash basis accounting remains a popular option, primarily due to its simplicity.

Advantages and disadvantages of accrual accounting

Unlike cash basis accounting, which provides a clear short-term vision of a company’s financial situation, accrual basis accounting gives you a more long-term view of how your company is faring.

This is because accrual accounting provides an accurate picture of how much money you earned and spent within a specified time. This offers a more precise gauge of when business activity speeds up and slows down for a business quarter or a full fiscal year.

Additionally, it conforms to nationally accepted accounting standards, so your accounting method won't need to change as your business grows.

Advantages:

Accrual accounting offers several key benefits that can help businesses, particularly those with an eye on growth, manage their finances more effectively.

- Creates a more accurate financial picture: It can give small business owners a more realistic idea of income and accrued expenses during a certain period of time. This can provide you (and your accountant) with a better overall understanding of consumer spending habits and allow you to plan better for peak months of operation.

- Conforms to GAAP principles: Since the accrual method adheres to GAAP, it must be used by all companies with revenue that exceeds a certain threshold. Since the $30 million sales revenue mark can be high for most small businesses, most will only choose to use the accrual accounting method if their bank requires it.

- Scales with your business: You may not be there now, but in a few short years you could double or triple your revenue, pushing you over the $25 million mark. If you already use the accrual accounting method, there’s no need to change—it simply grows with you.

Disadvantages:

Accrual accounting also has its drawbacks, which can pose challenges for smaller businesses.

These are the main disadvantages to consider:

- More resource-intensive: Many small business owners view it as more complicated and expensive to implement due to complexity and extra paperwork. Since a company records revenues before they actually receive cash, the cash flow has to be tracked separately to ensure you can cover bills from month to month.

- Inaccurate short-term view: The cash method gives you a better picture of the funds in your bank account. If you don’t have careful bookkeeping practices, the accrual accounting method could be financially disabling for a small business owner. Your books could show a large amount of revenue when your bank account is completely empty.

Advantages and disadvantages of cash basis accounting

The cash method of accounting certainly has its benefits, including ease of use and improved cash flow. While the cash basis method of accounting is definitely the simpler option of the two most common accounting methods, it has its drawbacks as well.

Advantages:

Cash basis accounting has a number of clear advantages that make it a popular choice for many small businesses.

- Simplified, familiar process: Cash basis accounting is a simplified bookkeeping process that is similar to how you might track your personal finances. It’s easy to track money as it moves in and out of your bank accounts because there’s no need to record receivables or payables.

- Income taxes: For tax purposes, you don’t have to pay taxes on any money that has not yet been received. For instance, if you invoice a client or customer for $1,000 in October and don’t get paid until January, you won’t have to pay taxes on the income until January the following tax year. This can be crucial to keeping your business afloat when cash flow is restricted.

Disadvantages:

Despite its simplicity, the cash method of accounting also has significant drawbacks that can impact a business's long-term health.

- Inaccurate financial picture: Since it doesn’t account for all incoming revenue or outgoing expenses, the cash accounting method can lead you to believe you’re having a very high cash flow month when in actuality, it’s a result of a previous month’s work.

- No accounts receivable or accounts payable records: Because the method is so simple, it does not require your CPA or bookkeeper to keep track of the actual dates corresponding to specific sales or purchases. In other words, there are no records of accounts receivable or accounts payable, which can create difficulties when your company does not receive immediate payment or has outstanding bills.

- Doesn’t conform to GAAP: If your business were to grow to exceed $30 million in sales soon, you might consider opting for the accrual accounting method when you’re setting up your accounting system.

How to choose the right option for your business

For small companies that do business primarily through cash transactions and do not maintain large inventories of products, the cash accounting method can be a convenient and reliable way to keep tabs on revenue and expenses without the need for a great deal of bookkeeping.

However, for the most accurate and updated accounting view of your financial health, accrual accounting might be the better choice. There are also some other factors to keep in mind.

The complexity of your business

Depending on your industry and the complexity of your books, one accounting method may be more sustainable than the other. For example, a business with multiple accounts, hundreds of employees, and various LLCs will probably want to stay away from cash basis accounting because it won’t give the company the big picture view it’s looking for when it comes to financials on the income statement, balance sheet or cash flow statement.

Sales revenue

Another reason to choose one over the other would be based on your sales revenue. According to GAAP, if you exceed a specific average annual revenue, then you are required to use the accrual method. For many small businesses, this isn’t an issue at the moment, but it may be in the future, so it’s something to keep in mind.

Publicly Traded

Having a publicly-traded company or one that may go public is another stipulation of the GAAP guidelines. Publicly traded companies have a duty to report an accurate view of their financial well-being to shareholders. The best method for this is the accrual system of accounting.

Inventory

If your business carries inventory, you'll need to use the accrual method. The Internal Revenue Service (IRS) requires companies that sell goods and maintain an inventory to track their inventory using accrual accounting to calculate the cost of goods sold accurately. This matches inventory cost with revenue in the same period.

Obtaining financing

When seeking a loan or other financing, a lender will almost always require you to provide financial statements prepared using the accrual method. Lenders use these statements to get a more complete and accurate picture of your company's financial health, including its assets, liabilities, and long-term profitability.

Streamline your accounting with QuickBooks

No matter which accounting method you choose, the key is to stay consistent and keep accurate records. And the best way to do that is by choosing a system that helps you spend less time on the books and more time growing your business.

QuickBooks can help you automate your accounting, manage cash flow, and simplify tax prep, so you can. The right accounting software can make a huge difference, helping you save time and stay organized.

Whether you've started a small business or are self-employed, bring your work to life with our helpful advice, tips and strategies.

Call Sales: 1-877-866-5232