1. Browser-based mobile payments

You might also hear this referred to as a web-based payment or even an online payment. With this type of mobile payment, customers enter their payment information into a website on their mobile phone.

Some websites have a built-in payment system (Shopify sites, for example), while others use payment options on external systems (like Amazon Pay and PayPal). The latter option directs customers to a separate browser window where they complete their transaction.

In either case, the entire checkout and payment process is happening within their browser.

Example: Marcy has an e-commerce site for her pottery business where she sells her handmade coffee mugs. On her site, customers can add items to their cart, visit the checkout page, and enter their card details directly.

2. App-based mobile payments

This type of payment is similar to a browser-based payment, however, it takes place within a dedicated mobile payment app instead of through an internet browser.

This is common among larger businesses and retailers, especially food businesses. Starbucks, Panera, and McDonald’s are just a few of many companies who have a dedicated mobile app where customers can make purchases.

Even if you aren’t an industry giant, this type of mobile payment can be used by any business that has and runs their own app.

Example: Keegan runs his own bakery where people stop to grab a quick to-go breakfast. He worked with a developer to create a mobile app specifically for his bakery. Through the app, customers can order pastries and process their payment, then pick up their order at the counter.

3. Mobile credit card readers

A mobile credit card reader allows business owners to use their mobile phone as their point of sale (POS) system.

To do this, they’ll need to purchase a mobile card reader. Today, most card readers not only process physical cards but digital wallets too—which we’ll talk about more in the next section.

Example: Jordan has a commercial cleaning business, where his crew cleans various office buildings. He likes to process payments from customers on the spot, so he uses a mobile card reader to accept payments from clients on location.

4. Contactless payments

Out of all of these types of payment methods, contactless payments are the ones that seem to be gaining more and more steam—especially since the start of the COVID-19 pandemic. Research from Payments Canada found that no-touch payments were used by 53% of Canadians.

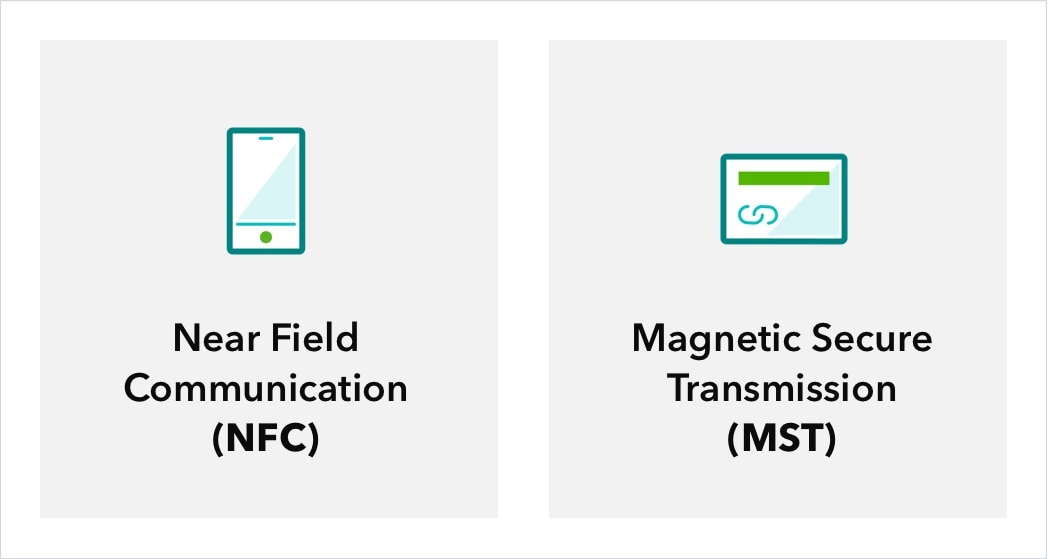

Here’s how it works: Customers use a mobile wallet (like Apple Pay for iPhone, Samsung Pay for Android devices, or Google Pay). They open their wallet app and a card reader scans their phone. Using Near Field Communication (NFC) technology, the card reader processes the payment information. There are a few contactless payment services (like PayPal) that use a Quick Response code (QR code) instead of NFC technology.

There are no physical card swipes or traditional authentication methods like PINs and signatures, and the actual card information isn’t transmitted. Instead, contactless payments use a virtual token that stands in for the card numbers, which is called tokenization.

There’s another subset of contactless payments: invisible payments. These happen almost without any action by the customer and reduce a lot of friction in the purchase process. Uber is a common example; you pay for your ride without even thinking about it.

Example: Jordan runs his own automotive repair shop. When customers come to pay for and pick up their vehicle, they hold their mobile device over Jordan’s card reader to process their payment.