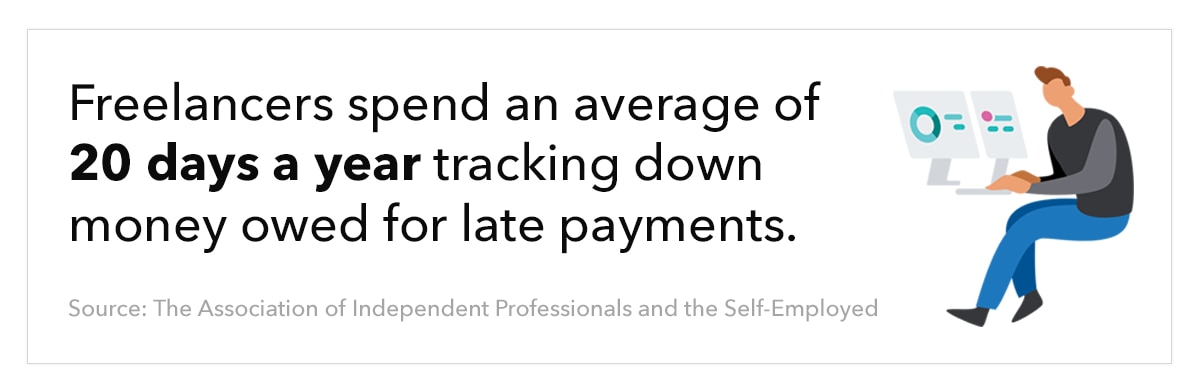

Here’s a situation no business owner or freelancer wants to deal with: invoices way past their due date. You’ve provided the agreed-upon service or product. You’ve sent out an invoice. You’ve waited and waited, and now it’s been months since you sent out the original invoice. Do you charge your customer a late payment fee in addition to pursuing the outstanding balance?

One of the toughest decisions businesses have to make is how to approach past due invoices. Freelancers and small business owners are particularly vulnerable to the negative effects of overdue payments. Why? Because when you’re running a business, multiple late invoices can negatively impact your cash flow and ability to run your operations.

In this article we’ll explore when you might need to assess late charges, how to create a late payment policy, and how to encourage prompt payments. Keep reading for a full explanation of late payment fees, or jump ahead to the section that directly answers your query.

- How to deal with late payments and unpaid invoices

- Charge a late fee

- Use a payment plan

- Offer an extension for first-time late payments

- Invoice management tips

- Use automated invoicing

- Keep track of unpaid invoices

- Send payment reminders

- Expand payment options

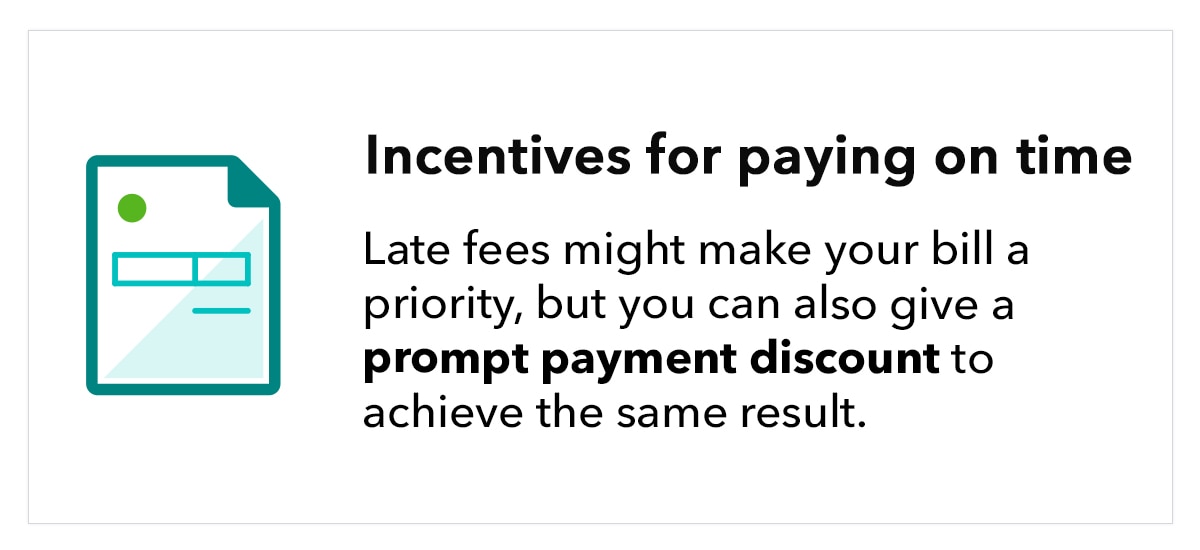

- Offer discounts for prompt payment

- How to create a late payment policy