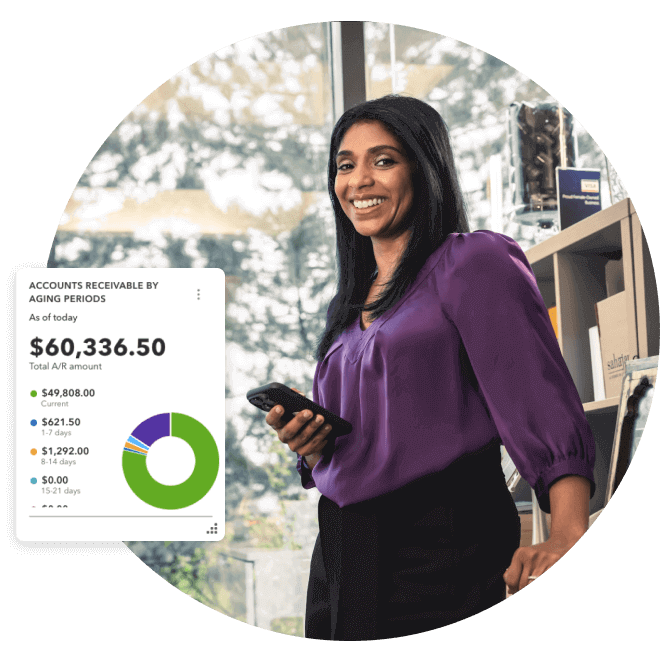

Artificial intelligence (AI) is no longer a phenomenon of the future when it comes to accounting. It’s quietly transforming how business owners manage their finances every day. From automating invoices to detecting errors early, AI in accounting can help you work faster and smarter.

According to the latest QuickBooks research, 62% of business owners use AI every month to save time, improve productivity, reduce costs and get paid faster. The best AI-powered accounting tools automatically handle the manual work you may still do, freeing up time to grow your business.

Find out how accounting AI can benefit your business, where to use it, and what to keep in mind as you choose the right AI-powered software for your

Start small by automating one time-consuming task, like data entry. Once you see the results, you’ll feel more comfortable integrating AI into your bookkeeping process.

Start small by automating one time-consuming task, like data entry. Once you see the results, you’ll feel more comfortable integrating AI into your bookkeeping process.