For many businesses, all commissioned work is considered a good thing. After all, that’s how your business makes money. However, not all projects are created equal. In fact, some can require more resources than they’re actually worth.

That’s why it’s important to weigh the cost-benefit of individual projects, especially when they fall outside the scope of your usual offerings. But how do you do that efficiently? Project accounting is one tool you can use to evaluate projects and determine if they’re worthwhile or if the margins are too tight.

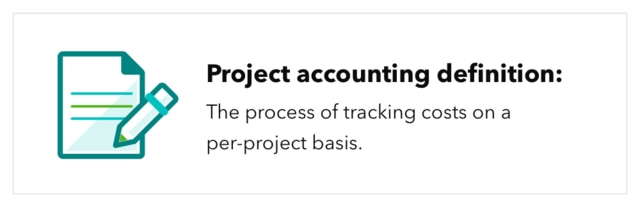

Project-based accounting is exactly what it sounds like—accounting on a per-project basis. The purpose of project-based accounting is to track project-specific costs and financial benefits. By employing project accounting methods, your business can get a better understanding of which projects add value and how to improve margins.

In this guide to project accounting principles, we’ll define project-based accounting and the benefits it can provide to your business. Read from start to finish for a comprehensive understanding of this approach, or use the links below to go to a specific section.