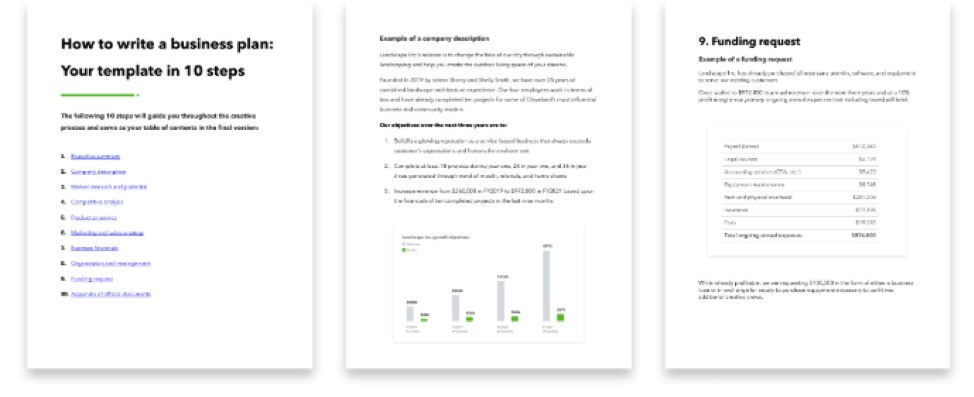

Here’s a handy template you can use to cover all of your bases: Download the template, here.

Put together your financial statements

Lenders want to look back at your financial history to gauge your management capabilities and look at your future business prospects. Although each lender might have different requirements, most will require a three-year projection for your income statement, balance sheet, and cash flow statement.

For startups, an opening day balance sheet, first- and second-year projections, and initial startup costs should be provided. While it may be difficult to project future results, lenders expect you to have a reasonable idea of the necessary capital and cash flow for your business.

These statements should be detailed, and show an analysis of how the cost of goods, gross margin, overhead and net profit have changed over time, and what those changes mean for the company moving forward.

Build this forecast from the bottom up, not the top-down, through simple multiplication. For example, know the time and cost of driving customer purchases and the gross profit on each sale. Understand the lifetime value (LTV) of a customer. Show where the leverage for increasing profit is and how the company will make money as the business grows in size.

If you aren’t 100% confident in preparing these documents, you may want to enlist the help of a business accounting expert or use QuickBooks Online to generate financial statements.

Finally, make a loan guarantee

If your business lacks a solid credit history or collateral, some lenders might require a personal guarantee on the loan. Lenders look first to the business for collateral. If it’s not sufficient, they’ll look next to the business owner’s equity position.

A loan guarantee document should list all forms of collateral, both business and personal. When a personal loan guarantee is required, lenders may also need a personal financial statement and three years of tax returns from the business owner.

If you bring it up first to the bank, it shows that you’re willing to stand behind the risk the bank is assuming. If appropriate, remind the bankers of a personal track record of previous loan repayments, both private or corporate, to this or other banks. Again, any past track record of repayment will make the bank’s decision easier.

Beyond all of the numbers and analysis, lenders look to the loan proposal and how it is presented as a gauge of your competence and confidence in managing your business to success. Try to present it in as professional a manner as possible.