Turn on suggestions

Auto-suggest helps you quickly narrow down your search results by suggesting possible matches as you type.

Showing results for

dear sir or Madam, i have a quesiton about stock adjustment.

I will check my inventory regularly and find that the real inventory is less than what the QB balance sheet indicates. Maybe some inventories lost or someone forgot to record them properly in the system. So, how can I adjust the inventory in the QB to make it is as same as the real amount?

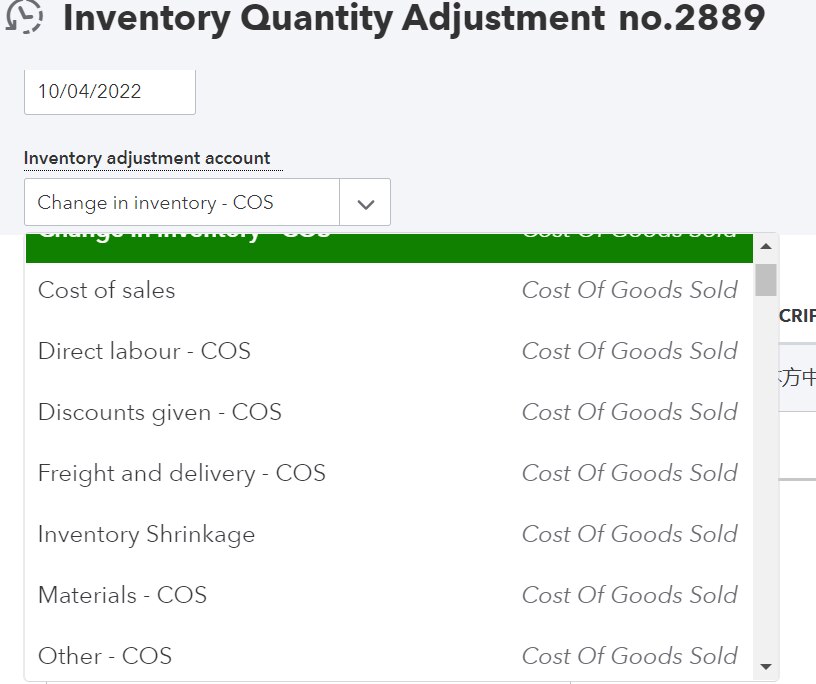

i fiannly find "Inventory Quantity Adjustment" in Qb.

i find that there are some items to choose in the "inventory adjustment account" ,including "change in inventory", "cost of sales", "inventory shrinkage", Other", etc. which one should I choose? "inventory shrinkage"?is there any other field or memos to record the real reasons?

if I choose "inventory shrinkage", how does it affect my balance sheet and income statement?

thanks a million

Recent

Good day, golden2010.

I can help share some information about inventory adjustment in QuickBooks Online.

QuickBooks automatically creates the Inventory Shrinkage account when making inventory adjustments and uses this account to record all changes and adjustments.

If you wish to use another account, I recommend reaching out to your accountant to guide you on a specific account to use. This ensures your books are updated.

To give you more insights about tracking inventories and the default accounts in QuickBooks Online, please visit these links:

I'll be right here to keep helping if you need more help with inventory management in QBO.

Select Suppliers and then Stock Activities. ...

Select Stock and then select Adjust Quantity/Value on Hand.

Select the Adjustment Type ▼ dropdown, then select Quantity, Total Value, or Quantity and Total Value. ...

Enter the Adjustment Date.

Determine the Type of Adjustment Needed:

Set Up an Inventory Adjustment Account:

Adjust Your Inventory:

Impact on Financial Statements:

Remember to consult with your accountant for specific guidance based on your business needs. Properly adjusting inventory ensures accurate financial reporting and helps maintain the integrity of your records

It's common to find discrepancies between physical inventory and what's recorded in QuickBooks due to losses or unrecorded transactions. QuickBooks has a feature to adjust these quantities, but choosing the right account is crucial to reflect these changes accurately in your financial statements.

Steps to Solve:

Inventory Quantity Adjustment:

Choosing the Correct Account:

Recording Reasons:

Impact on Financial Statements:

Additional Advice: If stock taking every day, consider using barcodes and a third-party app like Warehouse 15. It will help to do paperless stock take, and if you were dragging the product boxes to the desktop you will not need either, you will be able to perform stock taking on site, near the shelves, utilize item barcodes, and have that info automatically reflected in QBO via Adjustment document.

For more details, you can check out the Cleverence Warehouse 15 solution.

Hope this helps!

You have clicked a link to a site outside of the QuickBooks or ProFile Communities. By clicking "Continue", you will leave the community and be taken to that site instead.

For more information visit our Security Center or to report suspicious websites you can contact us here

{kind=link}