Turn on suggestions

Auto-suggest helps you quickly narrow down your search results by suggesting possible matches as you type.

Showing results for

Get 50% OFF QuickBooks for 3 months*

Buy nowHello!

I've recently bought a computer (office supply expense) to use for my company. I bought the computer from Apple through Affirm who offers payment plan.

At the transaction time, I've paid the taxes and will be paying the rest in 12 equal payments. I'd like to have some input on how to set up that expense and reconcile the future payments that will come in, as well as the taxes I've already paid.

Thanks!

Solved! Go to Solution.

The answer provided by @Mich_S is not entirely correct. You do not want to assign an opening balance to the liability account. That will be done when you assign the cost of the computer to the loan account when entering the bill.

To properly record this, create a liability account called "Computer Loan" or something similar. Also, make sure you have an appropriate fixed asset account called "Equipment" or "Computers". What you call the fixed asset account is up to you.

Then, when you enter the bill for the computer, assign the full cost of the computer (including tax) to the fixed asset account and enter the amount financed as a negative amount and assign that portion to the Computer Loan liability account. If you financed 100% of it, the bill will net to zero and show as paid. Then, when you make payments, assign the payment to the Computer Loan liability account. That will reduce the loan amount. If there is any interest, assign the interest portion of the payment to your interest expense account.

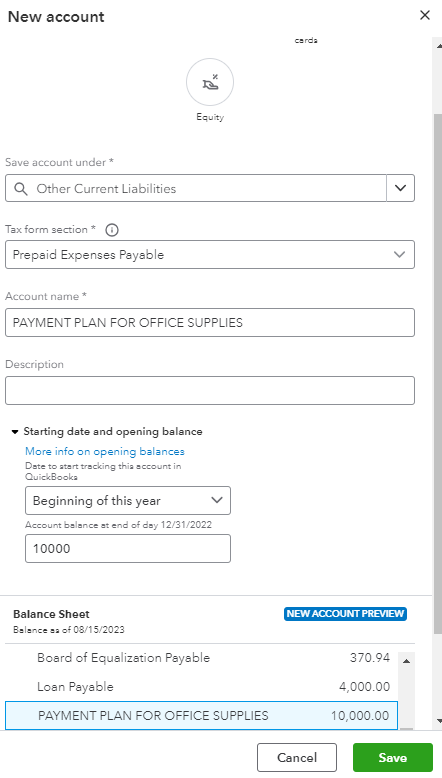

Good day, matty5. I want to share some tips about setting up expenses for an office supply bought using a payment plan.

First, create a liability account with an opening balance equivalent to the total amount of the supplies. This allows QuickBooks to keep track of the in and out transactions to this account. I'll show you how:

Note: It's advisable for you to reach out to your accountant if you're unsure of what accounts to use. They'll help keep your books in order as well.

Next, issue a bill with the total amount of the purchase. Here's how:

Finally, record your partial bill payments for 12 months until the plan is completely paid.

I'll also add this extra guide on how to reconcile your account in QuickBooks Online.

Keep in touch so we can help you further with banking or QuickBooks. Stay safe.

The answer provided by @Mich_S is not entirely correct. You do not want to assign an opening balance to the liability account. That will be done when you assign the cost of the computer to the loan account when entering the bill.

To properly record this, create a liability account called "Computer Loan" or something similar. Also, make sure you have an appropriate fixed asset account called "Equipment" or "Computers". What you call the fixed asset account is up to you.

Then, when you enter the bill for the computer, assign the full cost of the computer (including tax) to the fixed asset account and enter the amount financed as a negative amount and assign that portion to the Computer Loan liability account. If you financed 100% of it, the bill will net to zero and show as paid. Then, when you make payments, assign the payment to the Computer Loan liability account. That will reduce the loan amount. If there is any interest, assign the interest portion of the payment to your interest expense account.

Thank you so much @Rainflurry and @Mich_S for your answers, it solved my question!

Hello Rainflurry,

I have reviewed the solution you’ve shared and it's correct and accurate. Thank you for sharing your inputs to help address the issue.

We love to see members supporting one another. Have a great day.

Question, (the instructions worked perfectly by the way)...

Why does the "Negative Number" created on the BILL for the Loan Liability Account cause a "Credit" (that is, an increase in the right side or the credit side of the T bar or journal entry? This is correct (Credit on the Liability and debit on the asset account), but I don't understand. A liability is INCREASED with a Credit and decreased with a debit. so why is the number input as a negative number? In my head, it seems like it should just be a positive number (I know that doesn't work, but I don't understand why). Again, this worked perfectly! I'm just not smart enough to understand the relationship between the negative number and the journal entry showing an increase in the Loan Balance.

"Why does the "Negative Number" created on the BILL for the Loan Liability Account cause a "Credit" (that is, an increase in the right side or the credit side of the T bar or journal entry?"

A bill is designed to post the total amount of the bill as a credit to A/P. You don't need to specify that when you enter a bill, you just enter the accounts and QB knows those are the debits to offset the A/P credit. When you enter an amount as a negative on a bill, it reduces the A/P credit (because it's reducing the bill total) and credits whatever account you have selected on the negative line item. The negative line item is substituted for the A/P credit.

QB works the same way with invoices, except it enters the invoice total as an A/R debit. Whatever accounts are listed as income accounts on the items will be debited when listed as a negative amount on an invoice. The negative line item is substituted for the A/R debit.

Not sure if I explained that very well.

You have clicked a link to a site outside of the QuickBooks or ProFile Communities. By clicking "Continue", you will leave the community and be taken to that site instead.

For more information visit our Security Center or to report suspicious websites you can contact us here