Turn on suggestions

Auto-suggest helps you quickly narrow down your search results by suggesting possible matches as you type.

Showing results for

Get 50% OFF QuickBooks for 3 months*

Buy nowHello,

My accountant wants my deposits into my bank account from Square to be categorized as "Payments To Deposits". From what I read here, this does not show as income on the P&L, and I understand why, but is there a way to get the deposits to show as income without changing the category, and without going through months of data?

I'm here to ensure the deposit will show as income in your profit and loss report, @HeyGirlHeyBoutique.

The payments to deposits, also called undeposited funds, is an account that temporarily holds cash or checks that a business has received and is yet to deposit into its bank account. Yes, it won't show as income on the profit and loss.

There are two methods to achieve your goal. You can change the category or create a journal entry to transfer the funds from Payments to Deposit to the correct income category. However, I recommend seeking advice and guidance from your accountant before proceeding with the steps below.

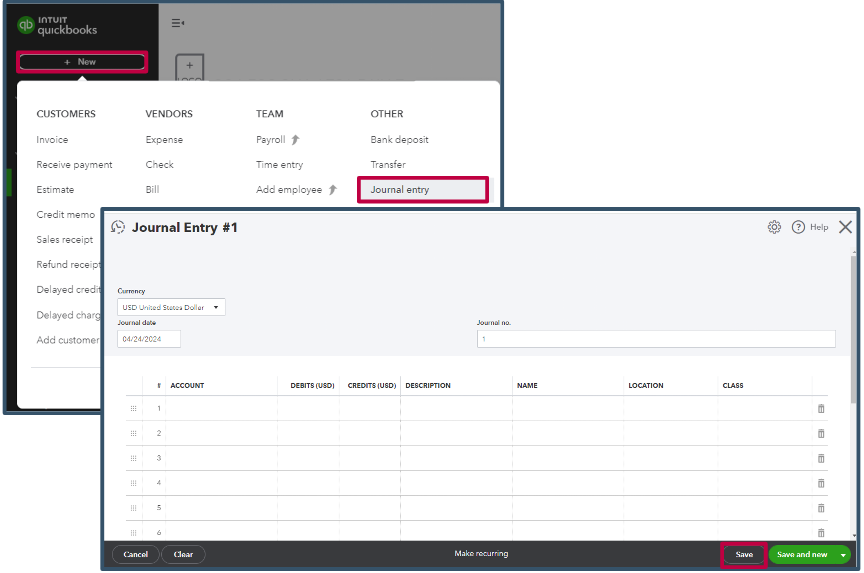

To create a journal entry:

Afterward, you can run the profit and loss report to view all income and expense transactions.

Furthermore, it's essential to regularly check your accounts in QuickBooks to ensure they match your bank and credit card statements. I'll add this article to learn how reconciliation works:

I can help you further whenever you need assistance managing your bank transactions. You can comment down below. Best wishes!

Thank for the quick response and solutions. Just to clarify, both of these solutions ultimately change the category of the transaction, is that a correct statement?

Thanks for getting back to us, @HeyGirlHeyBoutique. Both solutions provided by my colleague will change the category of the transaction.

The first option will change the transaction's category from deposit to income if you change it.

The second option is creating a journal entry, which can help you transfer money between income and expense accounts. It can also move money from an asset, liability, or equity account to an income or expense account.

However, it's important to note that creating a journal entry should be a last resort for entering transactions. It's recommended to consult your accountant before proceeding.

In case you need more guidance on reversing a journal entry to swap the debits and credits or deleting it completely, you can check out this article: Reverse or delete a journal entry in QuickBooks Online.

If you still have questions in mind, please feel free to message us back here by leaving a comment below. I hope you have a nice day ahead!

You have clicked a link to a site outside of the QuickBooks or ProFile Communities. By clicking "Continue", you will leave the community and be taken to that site instead.

For more information visit our Security Center or to report suspicious websites you can contact us here