Turn on suggestions

Auto-suggest helps you quickly narrow down your search results by suggesting possible matches as you type.

Showing results for

Get 50% OFF QuickBooks for 3 months*

Buy now

You can not have both, if the tool is high dollar (lathe, drill press, etc) then it is a fixed asset and subject to depreciation

Other wise it is an expense

Hey there, @charlie22.

Thank you for reaching out to Community. I'm happy to assist you with your tools.

May I ask which tools you are referring to? There are several different types of tools that you can change. As mentioned by Rustler, if you are referring to tools such as lathe, drill press, etc., this would be considered a fixed asset.

Here's how to change the tool account types:

However, if you are referring to a different type of tool within the product, you can check out these various articles to familiarize yourself with the processes.

If you have further questions or concerns, feel free to reach back out. I'm only a post away. Take care, and have a great day!

So yes drill press, jack hammer those sorts of things, but also small hand tools like hammers and screw drivers.

Hello, @charlie22. Thank you for your feedback.

As my colleague @Tori B, you can check out these various articles to familiarize yourself with the processes.

I'm providing the articles here that will help you set up your tools.

Set Up and Use the Project Feature

Change Product and Service Type

Also, this will help you set the tools you are needing up.

If you have any more questions or concerns, please don't hesitate to reach back out.

Hi, new to all this and doing loads of google searches and forum checks to get answers which brought me here.

I keep seeing time and time again, people with low knowledge asking!

were low cost is tools/ electrical items/ office equipment etc etc in expenses is.

the answer is always a long list of how to create which is a little confusing for someone new.

why arnt these just added to the relevant sections and added as a pre-select. seems like so many people are asking the same questions the amount of times ive read different responses typed out by admin surely it could have been entered into a field to help people out.

Just a thought there might be an obvious reason im missing but it seems frustrating for newbie

I am with @info-ahl-ltd on this one, every answer i see just leaves me with more question, just in this thread alone i went from should i put a hammer it as an asset to do i have non-inventory this crap creating more work.

@Rustler i normally find your answers very helpful so my question to you is, is there a specific amount for heavy equipment where i should to depreciation on? i am also having trouble finding answers on how to calculate depreciation... even for the vehicle, so i don't even want to ask about heavy equipment, but if you can shed some light that would be great. I don't consider any of the equipment i have to be heavy equipment but i do have a table saw, a few miter saw, compressors, just general equipment and i'm trying to figure out if i should classify them specifically as something when i buy them. Currently, i have everything under job supply but that is meant for things that will be used within a year, so i think i need to change them to something else but even the tax program doesn't help much on where i should put them besides as an asset... if the answer is an asset do i always have to depreciate it?

@Tori B i tried to followed what you said but either i lost you somewhere or you may not have understood the question which is the same one i have. I have a home depot receipt lets say for a hammer, that is an imported entry from my credit card, what category do i use? how does it relate to product and service? my service list consist on "demo with dumpster" because that is what i use to create invoices

@Sarah Bl the links you provided serve no purpose to our question, i am not going to classify a hammer under a project... where does it go when i buy it? is a tool we will keep using over and over, i may loose it, i may buy more, what do i do with my hammer purchase, my drill bits, 20G trashcans, are they consider company assets?

The IRS has a de minimus amount of $2,500 as an expense, per purchase. So basically it is a judgement call, do you want to lower net taxable profit all at one time, or in smaller increments over a number of years. Depreciation is found in IRS pub 946.

From what you say I would just expense those tools when purchased

No you do not have to depreciate any asset, but when you sell it or scrap it, the IRS can come back to you and say, no your income is higher since you did not take the depreciation you should/could have.

@Rustler like i said before your answers are always very helpful. i found https://www.section179.org/ which is under the publication you mentioned. Thank you, thank you, thank you for answering questions the way you do, it really helps a lot of us and if you have a youtube channel I would absolutely watch, i think you could make great short videos to explain things in a way it addresses questions from the little guy

Hello,

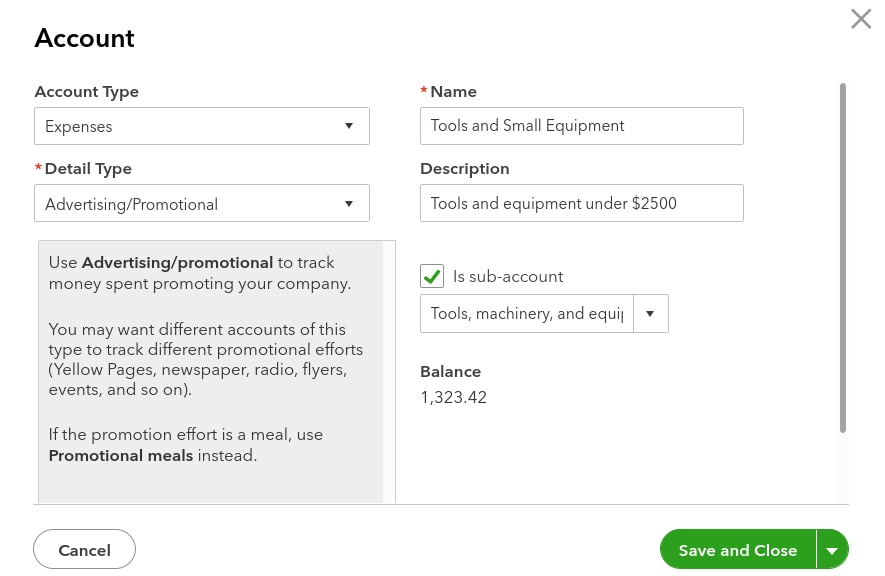

I'm trying to set up my tools and small equipment account as well. I do understand the value rating and how it affects the asset or expense account. My question is this however. When i click expense account I don't have a "tools" option under "detail type" drop down. None of the options apply to small tools. What do you suggest?

Use the category Supplies & Materials. Tools are usually listed as a sub section of Supplies on tax forms

Hi Rustler.

When I purchase small non asset tools, this is an expense. But which sub category do I use? Purchases?

Thanks in advance.

What if they're cheap tools, say $20 to $100 and what if they're $100 to $500? I have a wide range of tools i buy and am not to sure what to put the receipts under when i scan them.

Hey @masrollc out of curiosity what did you end up categorizing the expense as? Or did you just leave them as assets and depreciate over time?

I know I am way late to answering this, but we have a "production tools" expense for basically anything that doesnt fall into the asset category.

Okay I will pipe in here now as I am facing a similar issue. I understand that I need to expense tools for tax and accounting purposes. What I am also trying to do is record the small tools I own (torque wrenches, hex keys, hammers, speciality bicycle shop tools etc. The reason for this is simple; I want to know the value of my business. Can i record them as a product and service and just change to non inventory? or is there a way to record them as owners equity against cash/bank? Again all I am trying to do is put a value on my business; I have dealt with the expensing of them.

Robin

If you recorded them as an expense at the time of purchase, you will not/cannot show any value for them on your financial statements (balance sheet). You can track them outside of QB, but since you have expensed them, they have no value from an accounting perspective. They have value from a fair market value (FMV) perspective but that is different than the value you can show on your balance sheet. Your situation is not unusual. I have owned multiple businesses with expensed and/or fully depreciated assets and it was necessary to track their FMV outside of QB to understand the asset value of the business.

You have clicked a link to a site outside of the QuickBooks or ProFile Communities. By clicking "Continue", you will leave the community and be taken to that site instead.

For more information visit our Security Center or to report suspicious websites you can contact us here

{kind=link}