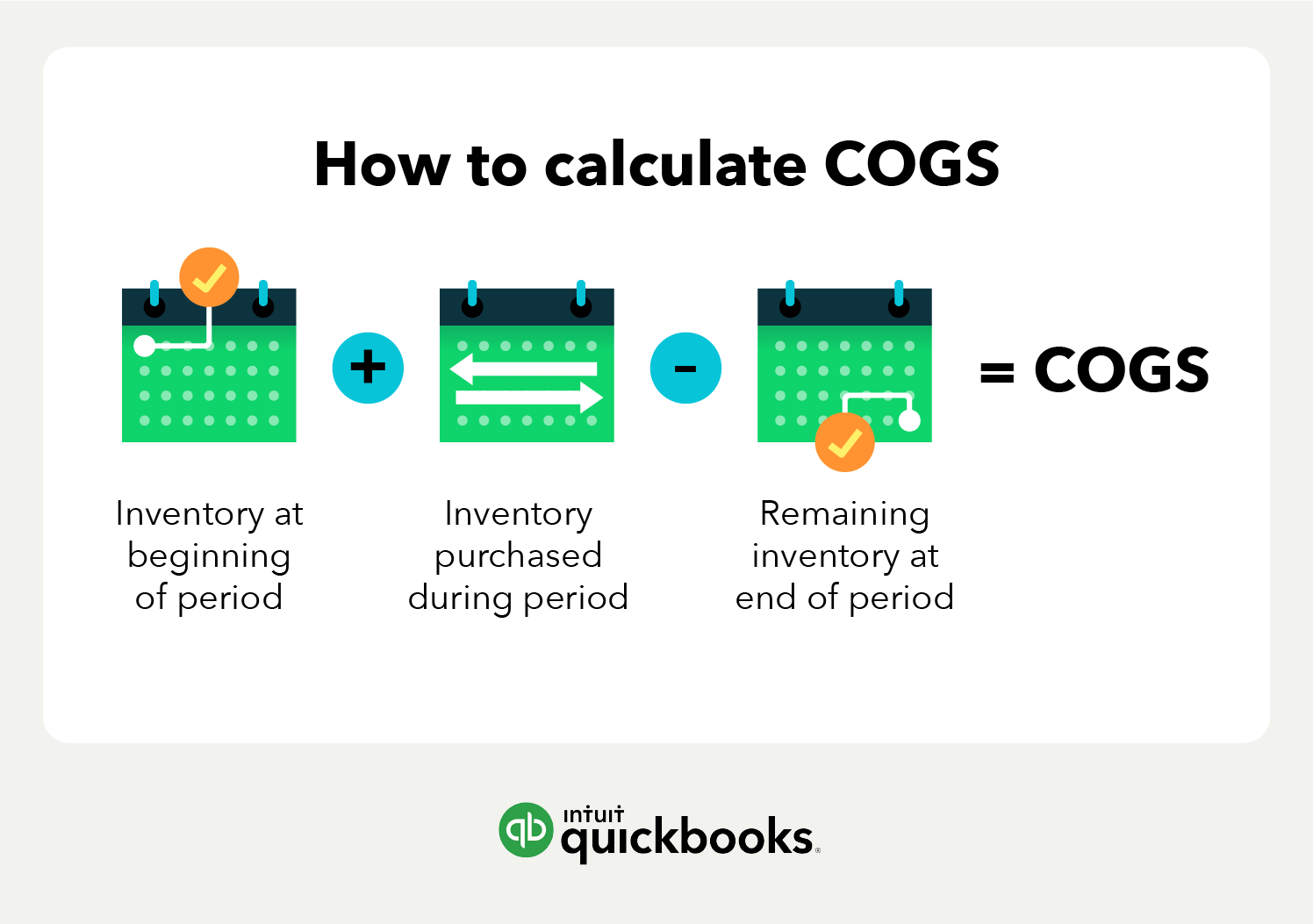

Understanding the financial health of your business is not simply looking at sales and revenue. To be successful, you need to know how much you are spending to generate that revenue. This is where the Cost of Goods Sold (COGS) comes in. COGS, sometimes called Cost of Sales, is one of the most important metrics for businesses selling a product or service. In sum, it shows the the direct costs that you can attribute to the production or purchase of the goods your company sells for given period.

Accurately calculating and analyzing your cost of goods sold isn't just an accounting requirement; it's fundamental to determining your true profitability, making informed pricing decisions, managing inventory effectively, and meeting your tax obligations with the CRA. Misunderstanding or miscalculating COGS can lead to misinformation when calculating profit margins and can lead to poor strategic, so it;s always a good idea to stay on top of it.

This is a comprehensive guide with all the information you need to know about COGS: