As a self-employed person living and working in Canada, there are a number of tax return documents you will need to complete and submit to the Canada Revenue Agency each tax year.

But which self-employed tax forms in Canada apply to your situation?

As a self-employed person living and working in Canada, there are a number of tax return documents you will need to complete and submit to the Canada Revenue Agency each tax year.

But which self-employed tax forms in Canada apply to your situation?

First things first, depending on the structure of your self-employed business, you will complete and file different tax returns. Typically, most individuals that work for themselves will structure their business as:

These business structures attribute the income earned from the operations as self-employment income. An incorporated business is considered a corporation for tax purposes. If you have incorporated your business, you are no longer considered self-employed by the Canadian government. Instead, you are an employee of the corporation.

Sole proprietorships and partnerships generate self-employed income. As a result, those who have structured their businesses as such will need to claim their business income on their personal tax returns. A sole proprietorship consists of a single owner, whereas a partnership means there are two or more owners.

Those who fall under self-employment income as sole proprietors or partners will pay the same income tax rate as any other Canadian employed by a business, who makes the equivalent income amount. How much you pay in taxes, is dependent on your income tax bracket. Depending on how much income you bring in within a year, your taxes will change.

No matter the structure of your self-employed business, you will need to file a personal income taxes alongside other applicable returns. Therefore, one of the most essential self-employed tax documents is Form T2125, Statement of Business or Professional Activities.

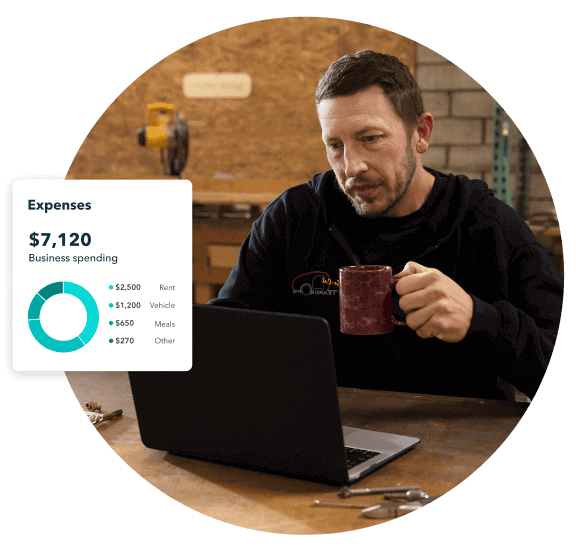

Form T2125, Statement of Business or Professional Activities is where you will record your personal and business income. This document is also where you will record your business expenses and will be able to deduct the costs of mobile phone bills, office rent, and other operating expenses. The CRA allows tax deductions to help lower Canadians’ overall taxable income.

If your income is generated through farming or fishing activities, you will need to complete further documentation, specifically, Form T2042, Statement of Farming Activities for farming income, or form T2121, Statement of Fishing Activities for fishing income.

Individuals that work as independent contractors or freelancers should be familiar with form T4A, the Statement of Pension, Retirement, Annuity, and Other Income. The T4A self-employment income slip helps individuals keep track of their income by client or job throughout the year.

Generally, a contractor or freelancer will receive a T4 slip from each of their clients for the jobs completed within the specified tax period. This slip will provide a total dollar amount for each job, which will help you track and record your income and calculate taxes owing.

Self-employed individuals that run their business as a partnership will need to complete additional tax documents for their returns—namely, form T5013, the partnership information return.

All types of partners must file this return, including limited partnerships and nominees and agents holding an interest in the partnership. If you own an interest in the partnership, then Form T5013SUM, Summary of Partnership Income, must also be completed and filed. The only type of partners that are exempt from filing this partnership information return for their taxes are Status Indians.

Once the above documents are completed, you can take that information and apply it to your T1 general return, the personal income tax return. For self-employment taxes, your business’s income is your personal income, so you will only need to fill out one form for your taxes.

If your sole-proprietorship or partnership business makes more than $30,000 a year, you will need to file form GST34, the GST/HST return. This allows the CRA to collect on the harmonized sales tax of your business. Your business will need to register for a GST/HST number in order to file this return.

The Canada Pension Plan is a government-run program that has anyone over the age of 18 who is earning money pay into this fund. An employee of a company will have two types of contributions to their CPP - their own, as the employee, and their company’s share, as the employer.

However, in self-employment, you will need to contribute to your own CPP fund, covering both the employee and employer’s contributions. Self-employed Canada Pension Plan contributions are based on what you earn within a tax year. If you make over $3,500 of net income each year, your tax bill will include CPP alongside income tax. There is no CPP contribution made on income above the maximum threshold. The CRA changes this maximum threshold each year depending on the average wage and salaries in Canada.

The CPP contribution rate is set to increase over the next few years for self-employment, so it is best to keep up to date with the CRA on these figures. On January 1st, 2022, the CPP contribution rate increased from 10.9% to 11.4% for self-employed persons living in Canada.

For further information on preparing for retirement when working for yourself, consider contributing to an RRSP or take dividends.

Now that you understand the applicable tax returns for self-employment, you will also need to consider when these returns must be completed and submitted to the CRA by.

The tax deadlines for self-employed individuals typically fall on June 15th each year. If you do not meet these deadlines, then the CRA can penalize you accordingly.

This also applies to your tax payments. The CRA offers small businesses and individuals installment payments to help you cover your taxes each year. If you do not pay off these installments before the appropriate deadline, you could incur a larger penalty.

On top of these penalties, you should be aware that the CRA can decide to audit your returns if your tax rates, salary information, deductions, or source documents such as invoicing or receipt documents do not add up.

To help you fill out these essential forms, you will need the corresponding business and financial information of your activities. When it comes to tracking and categorizing your expenses and revenue, look to QuickBooks accounting software to accurately record and depict your financial activity. Keeping up-to-date on your bookkeeping responsibilities will make the tax form process that much easier comes tax season.

Thanks to the QuickBooks Self-Employed tax features, this software provides you with the support you need to complete these necessary documents. With expense tracking and sorting and tax summary reporting, you’ll have access to an accounting firm on your smartphone. Why not try it free today!

Call Sales: 1-888-829-8589