Turn on suggestions

Auto-suggest helps you quickly narrow down your search results by suggesting possible matches as you type.

Showing results for

Get 50% OFF QuickBooks for 3 months*

Buy now

Let me help with your question about creating invoices, bdy-kmv.

Can you share with us the link or article that says you need to delete the invoice? We just want to make sure that everything is sorted out.

If you need to record a prepayment or a deposit, I'll share some steps with you to avoid deleting the invoice.

First, create a liability account to track the amount of the deposit you receive from your customers. Here's how:

Second, create a retainer item by following these steps:

Third, create an invoice to record the transaction. Here's how:

Lastly, turn the deposit into credits on invoices. Here's how:

You can read more details about these processes from this article: Record a Retainer or Deposit.

Let me share a couple more articles for additional references when working with your customers in QBO:

Reply to me or reach out to us again if you have other questions. The Community is always here to make sure they're answered and taken care of.

Thank you.

I'll try this.

To answer your question, when I initially posted this issue there was a response that suggested creating an invoice for the deposit, and then deleting it once the goods were actually billed.

I don't know how to find it, unfortunately, but I think it came from a QB employee.

One question.

When you say to create a retainer item and choose "Trust Liability Account" as income account do you mean the account I created in step one, or is this a specific account. I don't see "Trust Liability Account" as an option, though I do see the account I created.

Thank you.

Invoicing your customer for orders that will be paid through deposit is our top priority, bdy-kmv.

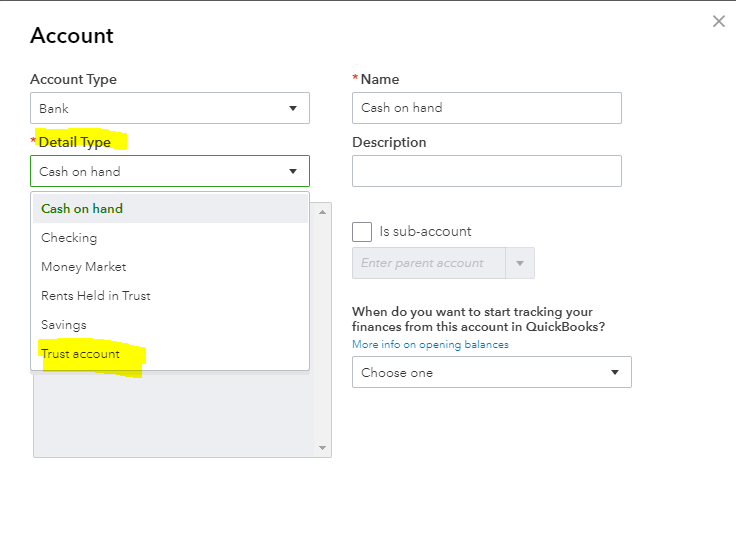

In accounting, a trust account is opened by an individual and managed by a designated trustee for the benefit of a third party per agreed-upon terms. On this point of view, the trust account is treated as a liability to show that although your business is holding the money from a deposit, it doesn't belong to you until it's used to pay for services.

Once you invoice the customer and receive payment from them, you'll turn that liability into income. Usually, you'll find the Trust account option under the Detail Type section. I've added a screenshot for your reference:

To know more about different account types so you'll be able to categorize transactions, check this article for more information: Learn About Chart Of Accounts In QuickBooks.

Additionally, QuickBooks download the latest bank transactions automatically. To know on how you can match them, I've attached this article for your reference: Categorize And Match Online Bank Transactions In QuickBooks Online.

Fill me in if you have questions about invoicing. I'm always right here to assist you.

I understand all that.

Please reread my question.

Greetings, @bdy-kmv.

Definitely, the account created in step one is the account is the item you'll need to use when creating an invoice. This will increase the liability and give a credit for any sales you have.

Therefore, all you have to do is select the same account you created in your Chart of Accounts from the drop-down menu.

Let me also add these helpful articles that you can read about handling deposits:

Please let me know if you have other questions about QuickBooks or deposits. I got your back anytime you need assistance. Have a good one!

You have clicked a link to a site outside of the QuickBooks or ProFile Communities. By clicking "Continue", you will leave the community and be taken to that site instead.

For more information visit our Security Center or to report suspicious websites you can contact us here