Turn on suggestions

Auto-suggest helps you quickly narrow down your search results by suggesting possible matches as you type.

Showing results for

Get 50% OFF QuickBooks for 3 months*

Buy nowMy company is a LLC taxed as an S-Corp. I have just established a SEP IRA. I am the only owner and have my wife on payroll as an employee.

The company will be makeing all of the contributions to the SEP. I have been reading through some Q&A but can't identify what sort of expense account to set up to record these SEP contributions. I have seen some say "Employee Benefits Expense" account but there is no such option in QBO chart of accounts.

What is the appropriate expense account to set up and record these SEP contributions to?

"you will need to make two journal entries:"

Actually, no, you don't need to make a JE at all. First, in payroll there is a provision for Benefits (taxable and nontaxable types) as "Company Contribution" so this can be "run through payroll" as part of allowing for Computation, even if it is not reported on the 940, 941, W2, etc. This is helpful when something is "based on wages" or Earnings.

"One increasing he IRA fund (set it up as a Banking account of type trust)"

You never track an IRA account in the Business data file; that IRA account is a Personal account owned by a Person. The Employer might be sending funds there, but that is not a Bank type of activity (asset accounting) for the Business entity.

"and decreasing the business checking account"

"And Decreasing Checking" = Write Check (entering an expense transaction). Now you can list the actual Payee, as well, because Banking menu has the banking tools. This would be instead of using payroll processing simply for computation, even as something set for Tax tracking as None. This would be, for instance, the employer paying out the Employer's optional contribution at year end, and they didn't want to compute anything relative to employee names throughout the year.

"(or recording the means of payment if not from business checking), and one journal entry debiting retirement plan expense and crediting retirement plan liability."

You don't need one JE, much less more of them.

If you use the "expense check" (even if ACH or EFT, and Paperless) to show the spending from Checking, you would list what you just paid out. You paid out Expense or you paid out Liability. And the way to Accrue that liability would be through payroll processing. And if you did that, you cannot treat that as a typical and regular "expense" entry; you would pay it out as any other tax-type liability.

So, it is always helpful to remind folks that you nearly never use JE in any QB product or program; and not for Banking; and not for something you computed through payroll. And not when Names are involved; paying out to brokerages = having a Payee name on the check expense or paying that from your liability tools from payroll, because you decided to compute it through payroll.

And often it is easier to wait until year end for the Employer Options, to see how much is available, or required to meet your Plan documents. For the Shareholder-employee, it often helps to wait until year end, because your Computed allowances takes into account your K-1 earnings and your W2 earnings. It's a bit more complicated, for you.

"I am the only owner and have my wife on payroll as an employee."

Do you Work for the business? Because that means you also are an Employee. There is no Owner. You might be a Shareholder-Employee, or just Shareholder and do not do any work.

There is no such thing as Nonemployee if you Work for the company. This is a very costly error; I have attached some IRS wording for you. You still have time to Correct this before year end.

"The company will be makeing all of the contributions to the SEP. I have been reading through some Q&A but can't identify what sort of expense account to set up to record these SEP contributions. I have seen some say "Employee Benefits Expense" account but there is no such option in QBO chart of accounts."

Then add one, make a new expense account. The W2 needs to indicate "Covered by retirement plan" as well.

https://www.irs.gov/retirement-plans/operating-a-sep

"Current tax law permits the S-Corporation to contribute up to $54,000 or 25% of the compensation of the employee"

And you also just stated this: "To date, company contributions are 100%, shareholder-employees contributions 0%."

That is the Employer's Optional amount as expense. I covered this. You can simply put this on an "expense" check, when you pay it out, such as at year end, you determine what is affordable.

"I think when you mention the "Benefits section" you are talking about QB DESKTOP payroll, rather than QB ONLINE payroll. I am using QB Online Essentials payroll. QB Online Essentials does not appear to have a Benefits section."

This does not need to run through Payroll; it isn't reported on any tax form or payroll form. You should have a Benefits section of Expense. Yes, all payroll provides for Benefit types of activity, but you don't need it, for Employer Optional Amount, unless you want to accrue it through the year, such as Compute on Gross. You know this exists; it is similar to any other Tax type, such as FUTA is employer-paid only, and based on Gross.

"When setting up company contributions in payroll deductions under payroll settings"

It's not a Deduction .

Here, read these articles:

https://community.intuit.com/articles/1643602-deductions-and-contributions

I have a similar situation with a Simple IRA. Please see below. Thank you.

I'm a 1 person S-Corp where I am the single employee. I just transferred from QB Desktop to QB Online.

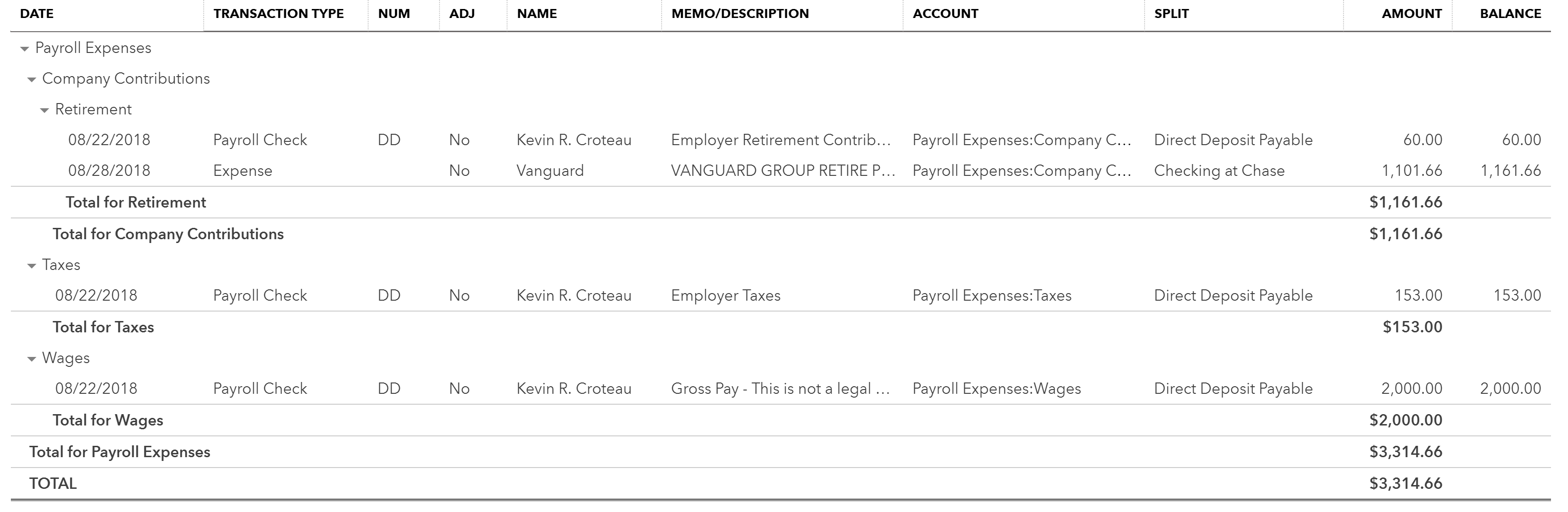

Both my Employee & Employer Simple IRA contributions are falling under my Payroll Expense Retirement Account. I'm not sure if this is correct.

As an example, each month the Company Contribution or employer contribution is $60 while the employee contribution or deduction is $1,041.66 for a total of $1.101.66. I think something is wrong with my payroll setup, what account should the employee contribution / deduction fall under? It seems it's going to Payroll Liabilities. The Total $1,101.66 transaction each month is initiated from Vanguard.

Greatly appreciate it. As a small business owner who some years makes less than $50k I love to learn. Thanks.

Your Check on the 28th is an Error.

Here is how this works: On the 22nd, because of the Paycheck, the Gross Wage expense for the employee is not fully paid to the employee. The Employee's share of taxes, and IRA, are held back. That makes this amount Not paid out of Checking, seen as a Liability (to be paid out later, instead of being part of takehome).

As a result of the setup, the Employer Share of taxes and the Employer's share of IRA is also computed. It is posted for the 22nd as Expense, and since it was not immediately paid out, it is also seen in Liability for the 22nd.

Later, these are NEVER banking checks as CHK. They are all Special. They are Liability Checks, because they are part of Payroll activities. They are never Expense; the Expense was posted as part of the computation on the 22nd. The 28th simply is the Banking, that the Liability Payment happened.

It doesn't matter that Vanguard "pulls" the funds. You need to do the Bookkeeping of the Liability Payment, and for Check #, you can put EFT or ACH, to show you did not issue this as a paper check. You want to show how much Vanguard took this time, as a Payroll Liability check activity.

Hope that helps.

I migrated from QB Desktop and Intuit Online Payroll to QB Online in June 2018 and this is how they set it up?

When you say that my Check on the 28th is an error do you mean the amount, incorrect account, or that it shouldn't exist at all? My Wages account shows the entire monthly salary of $2,000 as payable?

I am so frustrated with Intuit. I own stock in this company and I am irate at this migration.

Can you please advise? Thank you.

The employee 60 is never expense; that part is wrong. It's already part of 2,000 that is Gross Wages as expense. That is supposed to post the employee deduction to Liability = to be sent on, later. The 60 should not show Separately as expense in addition to Gross Wages as expense. Payroll Expense has Gross Wages. Employer has Tax Expense for FICA, SUI, FUTA, etc. Employer has Benefit Plan Expense for their match (1041.66).

Payroll Liability should have two entries into it from the One paycheck, the 22nd: Employee deducted amount and the Employer match amount. Additional entries would be tax liability (employer + employee shares). That's why Liability gets paid out at a later date, which is not More Expense. It's banking Expenditure = cash flow.

If you are earning 2,000; you don't get it. You have employee tax deductions, sent on your behalf. You have Retirement contribution deducted, send on your behalf. "sent on your behalf" = the employer is Holding your funds = they are responsible, or have the Liability to send in your money.

All of these deductions do not change Expense; you still are getting 2,000 gross wages; it just isn't all paid to you.

The 60/month employer contribution should be posted as retirement benefits, never issued as a check directly to you. When the employer writes the check, the check should be written out to the company in charge of the retirement fund (VanGuard for instance or Edward Jones or American Funds or whoever) rather than to you directly. The employee contribution would be deducted from your paycheck, and paid by the employer to the company in charge of the retirement fund.

When I open the "banking" SEP account (to increase the IRA fund), what tax-line mapping do I choose?

There is no Bank account for the SEP; you don't track the SEP in the business accounting. The SEP is a Personal account.

A business establishes the Plan, which means, intends to comply with the Regulations. The Funds are contributed to the Brokerage account owned by the Employee.

You do not track the SEP in the Business. You would already be entering the payroll and banking events as the Spending. You don't track changes in the SEP account in the business, because that does not belong to the business.

Here's where that gets confusing: the one employee of the business who contributed to the SEP is the sole S-Corp owner of the business, and the only employee of the business. So the account is still held by the owner of the business, because the employee and owner are the same person. So basically you are telling me that I need to tell the business owner if he wants to know how much he put in his SEP later on he has to ask his brokerage?

No, this is not part of what got stated:

"So the account is still held by the owner of the business, because the employee and owner are the same person. So basically you are telling me that I need to tell the business owner if he wants to know how much he put in his SEP later on he has to ask his brokerage?"

Think if this was Rent. You can always report on how much Rent has been paid out. But, you are the tenant, so you don't track anything other than the Outflow.

You don't have an Owner. You have a Shareholder, or Shareholder-Employee. You have Payroll reporting for employee contribution and employer match. You are not Tracking the SEP; you are tracking the Financial Activity as it impacts the Employer's accounting and reporting.

had this part Wrong: "When I open the "banking" SEP account (to increase the IRA fund), what tax-line mapping do I choose?"

It isn't the Employer's bank account. If my employer sends funds to my SEP, that is My Account, not my employer's.

I used the term "owner" because the shareholder-employee of the S-Corp is also the ONLY shareholder, as well as the ONLY employee of the S-Corp. Therefore, this shareholder has 100% ownership, which is usually what the term owner means. So the SEP account does belong to the shareholder-employee, who has 100% ownership of the company. This year, he chose to do a 100% employer contribution to the SEP, which cannot be run through payroll on QuickBooks Online Payroll, because that is only set up for a SARSEP which is not the same thing as a SEP for tax purposes. SARSEP accounts cannot be established after 1998. Since the same person is the onIy shareholder and the only employee, there was no employee matching of the employer contribution. I can certainly reverse the journal entry I used to establish the tracking account of type bank for the SEP, which matches the liability for the SEP that still remains on the books indicating that the SEP does not belong to the business but to the employee. Technically there is no other liability, since it has been sent to the brokerage already by the 100% shareholder-employee. The expense for retirement plan has already been recorded against the bank account.

Let's try this again:

"which is usually what the term owner means."

No; the Supreme Court has declared that a Corporation is its own Entity. There is no Owner.

"So the SEP account does belong to the shareholder-employee"

But not part of the Company Financial data, not tracked here, and is only a Cash Flow activity for the business. It's like paying Rent. There is no Account to Manage the activity or balances because this is not a Company Investment account. It is personal for the Employee.

"who has 100% ownership of the company. This year, he chose to do a 100% employer contribution to the SEP, which cannot be run through payroll on QuickBooks Online Payroll"

It's just Spending. It's money Out. There is no Bank. You post it as Expense. It's like paying Rent.

"I can certainly reverse the journal entry I used to establish the tracking account of type bank for the SEP"

This is the Error. There is no Bank and there is no Tracking the SEP. Let's try it like this:

You are their employee. They put in money on your behalf. They do not track your Retirement Account holding(s). It's the same thing you just described, that the Company would have a Bank account to track Your retirement holdings. That is the Error.

"which matches the liability for the SEP that still remains on the books indicating that the SEP does not belong to the business but to the employee."

Let's try this part:

I write a Check to pay out the Expense. If I accrued the Expense into liability, I later pay out the Liability. There is no Bank here. And Bank is Asset. All we have is either Expense; or Accrued Expense as Liability to be paid out later, the same ad Employer pays FUTA or Worker Comp or General Liability insurance.

"Technically there is no other liability, since it has been sent to the brokerage already by the 100% shareholder-employee."

Sent "by" the Employee is also an Error. The company sends the funds for Employer-only. And if this was Paid already, there is no Liability tracking. Again, it's like paying Rent: Enter the Spending. Done.

"The expense for retirement plan has already been recorded against the bank account."

The Spending is part of the bank account or credit card used to make the payment.

The Details are what just got paid for.

I enter on the Check from Checking, the expense for employee retirement.

You have deeply overthought this and are tracking the wrong things.

Ok, if the employee and the employer weren't the same person, I wouldn't have even bothered to track this. I looked for information in other replies as to how to do this, and found information on entering both liability and retirement plan expense. So basically the liability only applies until the funds are sent to the retirement plan brokerage then? If that is the case, then what I have currently is a tracking asset that is not really an asset, and a tracking liability that is not really a liability. To zero those out, I would then debit the liability and credit the asset in a journal entry.

This is Not the issue: "Ok, if the employee and the employer weren't the same person"

By Definition, they are Not the same Person. You keep forgetting this. The Employer is the Entity. Sure, the employee has to work for the entity, but that is The Entity. The Human is doing the work. The Employer is the Entity. The entity is not a Person. It's The Corporation.

They are Never the same Person. The Human person is wearing two different hats at different times: Representing the Employer, or Being the Employee.

The bookkeeping belongs to the Business, the Corporate Entity. It doesn't belong to the Person, Personally. The Bookkeeping is the Business, which then reports the End Results to the Shareholders.

"So basically the liability only applies until the funds are sent to the retirement plan brokerage then?"

You use Liability accounting when there are Accrued amounts not yet sent in, to show you need to Pay It Later. Example:

The Paycheck has employer expense and employee withholding. They both flow to Liability, so that the employer expense is already in the P&l, as is the employee's Gross Wage as expense. The amount the employee did not get to take home is included in the employer's Liability payment, since both amounts were held as Liability to be paid later. That makes it Cash Flow, later, and not Expense, when the Banking happens later.

"If that is the case, then what I have currently is a tracking asset that is not really an asset, and a tracking liability that is not really a liability. To zero those out, I would then debit the liability and credit the asset in a journal entry.'

Or, remove your Wrong entries entirely.

Paycheck Gross wages for 40 hours this week at $10 = $400

I don't get to take that home.

The Employer holds back my taxes and my share of Retirement as Liability.

The paycheck processing results in the program computing and posting Employer taxes and employer share of retirement and anything else we put into payroll processing.

Now, the Banking that happens right away is Employee gets their takehome pay.

Later, we Pay Liabilities, as the taxes and retirement funds, and that clears out the Liability.

The only asset tracking here is all of the Bank Payments that get made = funds Out.

You will need to wear 2 thinking caps and also maintain 2 sets of books. The business owner/company books and the Employee/personal books.

Since you are one in the same you can make it difficult on yourself and co-mingle the books; but it gets messy unless you're a trained accountant and even then we wouldn't do it that way.

But if you insist in only using 1 set of books then you will need to make your personal accounts different then the conapmy's truce set of books. This way you can track all aspects of your finances. If you're interested in having me elaborate then please send me a message and expect a few days for a response at this time of the year being its tax season.... Best of luck.

How can i get the employee and Employer contribution to go on check to the vendor......right now i can only get it to show the employee contribution as a liability....but i should be able to send our-the company contribution and employee contribution one check? can anyone help with this.

i am using desktop

Hello jerold3095,

The employee deduction and the company contribution come in pair. Thus, they should fall under the same vendor. Let's check your settings and verify if these two have different names.

If that's your case, we'll need to edit one of them so you can print a single check for your vendor.

Let me show you how:

Then, go to the Pay Liabilities tab to create a liability check.

Please read this helpful article for details: Set up and pay scheduled or custom (unscheduled) liabilities.

You might also want to check out this article for future reference: Set up your Federal Forms 940, 941 and 944 for e-file in QuickBooks Desktop.

Get back to me anytime if you have follow up questions. I'm always here to help.

You have clicked a link to a site outside of the QuickBooks or ProFile Communities. By clicking "Continue", you will leave the community and be taken to that site instead.

For more information visit our Security Center or to report suspicious websites you can contact us here

{kind=link}

{kind=link}