Hello, @devapatir.

Thank you for the detailed information. I can guide you on how you can use your customer's payments to allocate it to your interest expense and loan.

First, you have to record the payment, then deposit the amount on your bank account. Once done, you can use that account when writing a check for the interest expense and the long-term car loan.

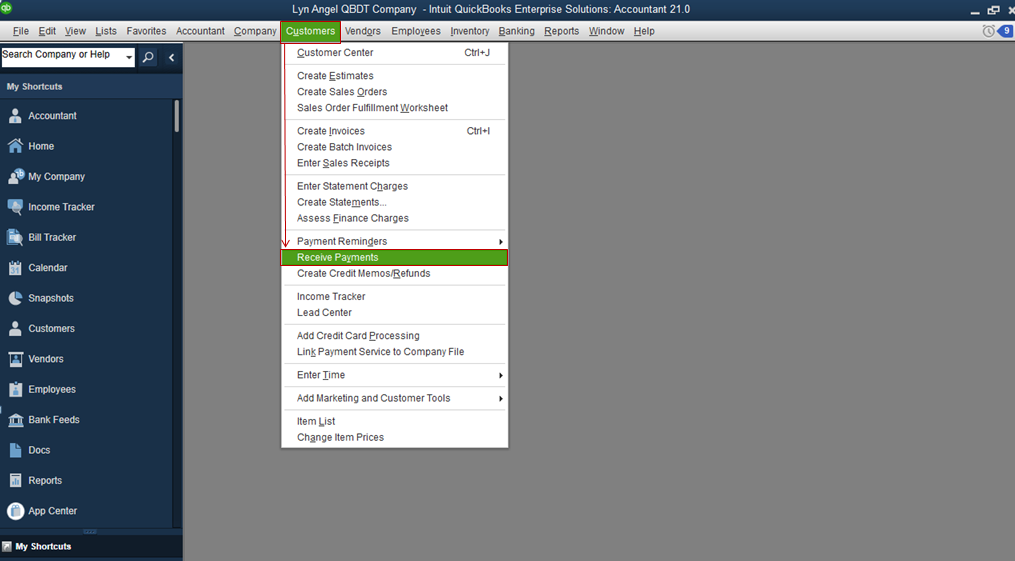

To record the payment on the client's invoice:

- Go to the Customers tab, then click Receive Payments from the drop-down.

- Pick the customer's beside the Received From section, then choose the invoice/s you want to mark as paid.

- Select a bank account where you want to deposit the funds beside Deposit To. If your account was set-up to deposit the payments automatically to the Undeposited Funds, deposit it to the desired bank account.

- Save the transaction.

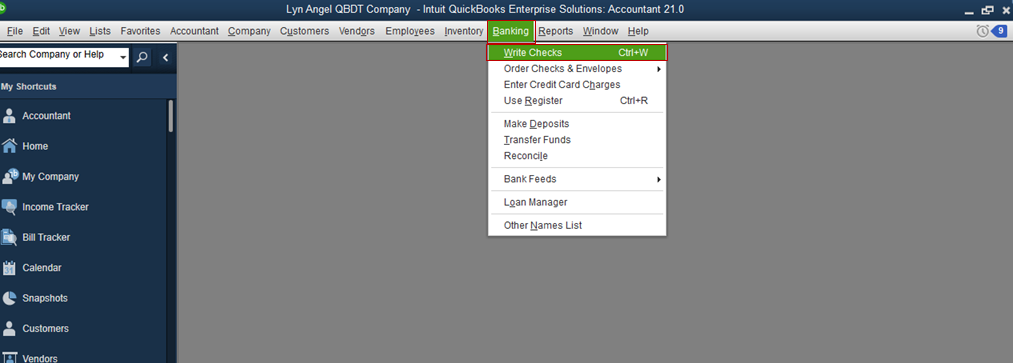

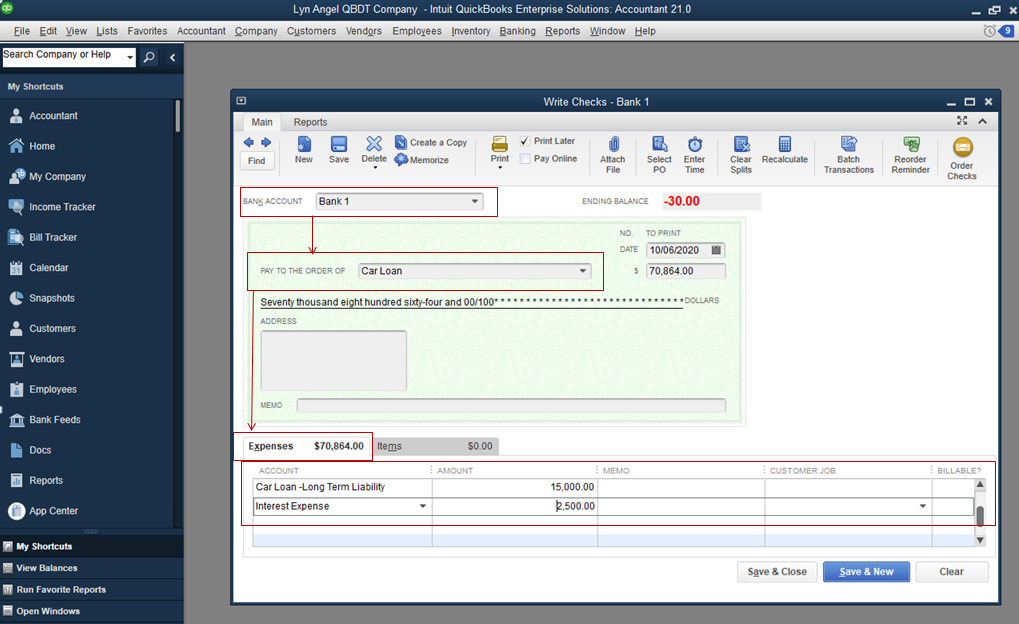

Then, here's how you can record your loan and interest payment:

- From the Banking tab, tap on Write Checks.

- Select the account where you deposited payment on the Bank Account field.

- Fill in the required information, then click on Save and Close.

To learn more about tracking loans in QuickBooks Desktop, feel free to read the details from this link: Manually track loans in QuickBooks Desktop.

If you need additional resources while working with QuickBooks, you can also read the topics from our help articles.

Let me know if you have any other questions. I'm always here to help. Have a good day!