Turn on suggestions

Auto-suggest helps you quickly narrow down your search results by suggesting possible matches as you type.

Showing results for

My client is using an inventory system outside of QBO essentials, so I will be doing monthly periodic inventory adjustments. Can someone confirm I am entering purchases, sales (of inventory), and periodic inventory adjustments correctly?

Inventory Purchased goes into an Other Current Asset Account (called Inventory Asset).

Inventory Sold goes into an Income Account (called Sales- Parts).

At the end of each month I do a journal entry- credit Inventory Asset (based on the inventory value in the system client is using) and debit COGS.

Thank you!

That's not an option. My client is running QBO Essentials.

You can always upgrade them to Plus, there is not much of a price difference.

If not, the JE process you are doing seems to be a good alternative.

Thank you. What about the inventory sales- it's income (Sales-parts), correct?

At YE my client sold about 60K worth of his inventory (sales- parts), and has 80K Total Income. With the monthly periodic inventory adjustments he has 48K in COGS (Beg Inv 21K (+) Purchases 75K (-) End Inv 48K. So, 32K gross profit. I guess this is correct, but for some reason something doesn't seem right?! Does this all sound correct?

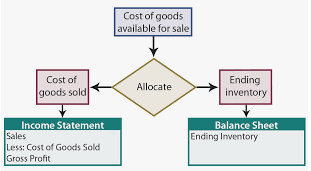

The formula is: Beginning inventory + Purchases - Ending inventory = Cost of goods sold. The inventory adjustment figure can be substituted into this formula, so that the replacement formula is: Purchases + Inventory decrease - Inventory increase = Cost of goods sold.

Yes. Inventory Sales is Income, you map the products or services sold to income accounts.

You have clicked a link to a site outside of the QuickBooks or ProFile Communities. By clicking "Continue", you will leave the community and be taken to that site instead.

For more information visit our Security Center or to report suspicious websites you can contact us here

{kind=link}

{kind=link}