Turn on suggestions

Auto-suggest helps you quickly narrow down your search results by suggesting possible matches as you type.

Showing results for

Get 50% OFF QuickBooks for 3 months*

Buy nowMy boss has two companies, Company A and Company B. My boss got a loan ($25,000) from BOA. This loan belongs to Company A in BOA, but my boss requires that Company B shares a part of the loan ($10,000).

How to record it?

Solved! Go to Solution.

Hi janezh!

It's great to see you in the Community! I'll help you record your boss's loan. However, please have this checked with an accountant to be sure your records are correct.

COMPANY A:

Create a liability account to track the bank loan.

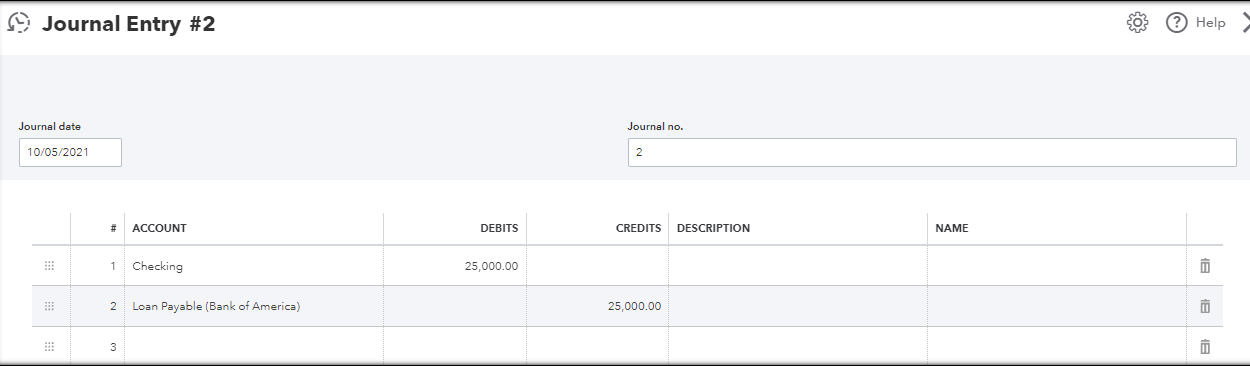

Record the $ 25,000 they received via bank deposit or journal entry. This should increase the balances of their loan account and their asset account, in which the actual money is deposited.

via bank deposit:

via journal entry:

Now, let's record the money that will be given to Company B. However, you didn't mention if Company B will still need to repay Company A or not.

To record the money that'll be given to Company B, you'll want to track it in an Other Current Asset account if it's repayable. If not, you can create an expense or something like a donation account instead.

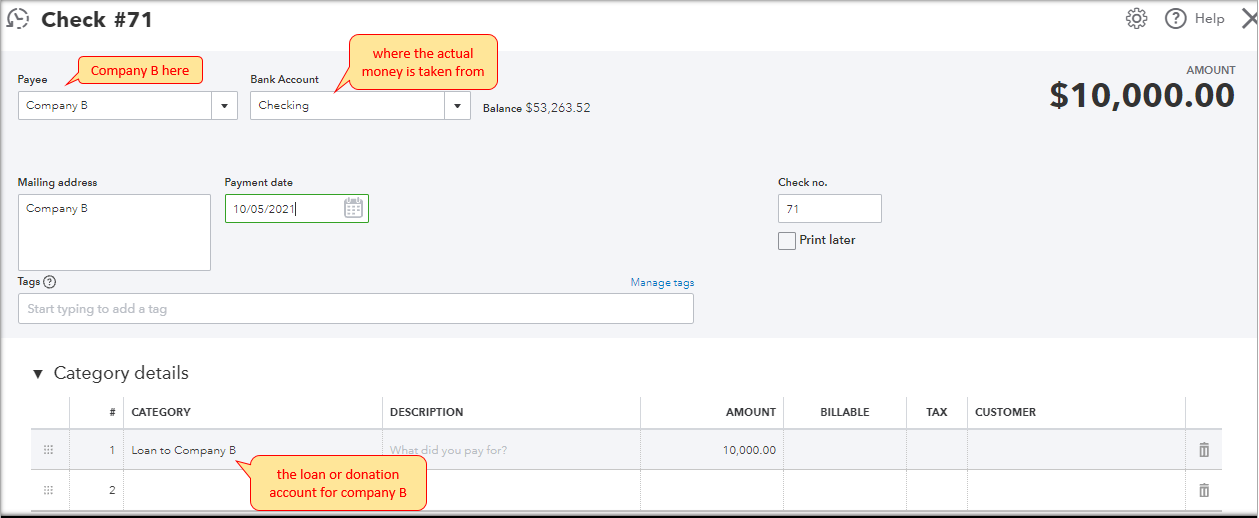

Add Company B as a vendor. Then, record a check transaction for them against the asset account and use the loan, expense, or donation account that is created for them.

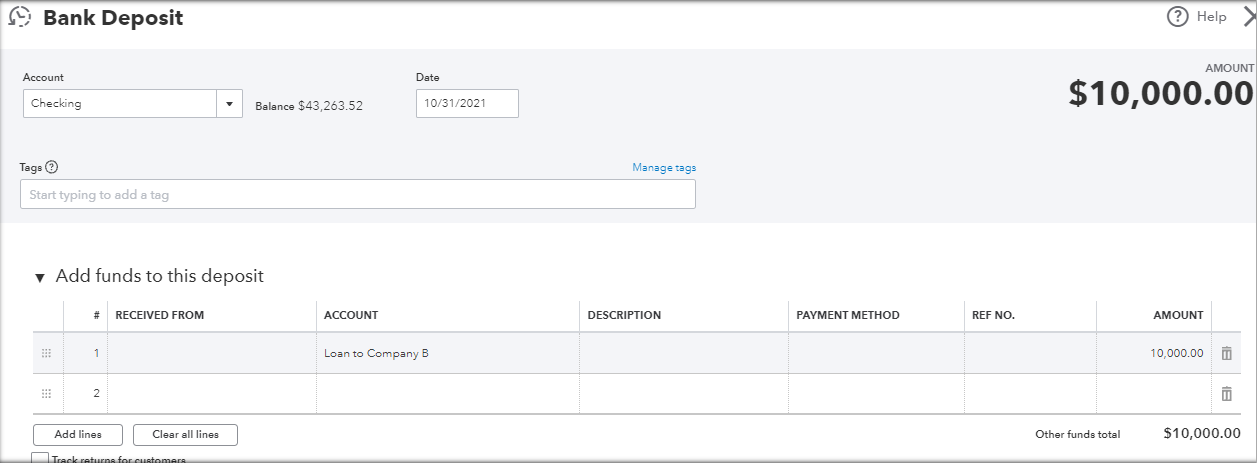

If Company B repays Company A, record it as a bank deposit or journal entry. But, this time the affecting accounts should be an asset and the loan account for Company B.

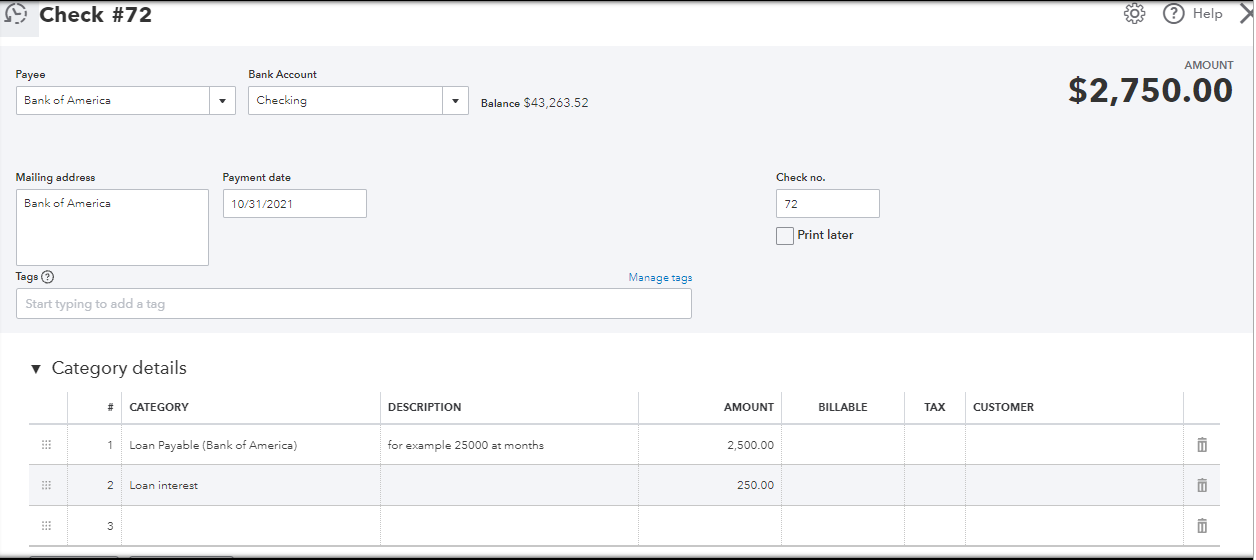

When Company A repays the bank, add the bank as a vendor and record a check transaction for them. In the Account field at the top, choose an asset account where the repayment is taken from. Then, in the Category details section, choose the loan account for the bank and enter the amount. If it carries an interest, add it in the second line.

If Company A does a staggered payment with interest, use the loan account in the first line and add another line to track the interest.

COMPANY B:

In Company B, you'll want to create a liability account to track the borrowed amount from Company A. If this is not payable, use a different account. Then, track the received money via bank deposit or journal entry. If it's payable, add company A as a vendor and create a check for them or record the repayment as a journal entry.

That will do it. If you have other questions in mind, feel free to go back to this thread.

Hi janezh!

It's great to see you in the Community! I'll help you record your boss's loan. However, please have this checked with an accountant to be sure your records are correct.

COMPANY A:

Create a liability account to track the bank loan.

Record the $ 25,000 they received via bank deposit or journal entry. This should increase the balances of their loan account and their asset account, in which the actual money is deposited.

via bank deposit:

via journal entry:

Now, let's record the money that will be given to Company B. However, you didn't mention if Company B will still need to repay Company A or not.

To record the money that'll be given to Company B, you'll want to track it in an Other Current Asset account if it's repayable. If not, you can create an expense or something like a donation account instead.

Add Company B as a vendor. Then, record a check transaction for them against the asset account and use the loan, expense, or donation account that is created for them.

If Company B repays Company A, record it as a bank deposit or journal entry. But, this time the affecting accounts should be an asset and the loan account for Company B.

When Company A repays the bank, add the bank as a vendor and record a check transaction for them. In the Account field at the top, choose an asset account where the repayment is taken from. Then, in the Category details section, choose the loan account for the bank and enter the amount. If it carries an interest, add it in the second line.

If Company A does a staggered payment with interest, use the loan account in the first line and add another line to track the interest.

COMPANY B:

In Company B, you'll want to create a liability account to track the borrowed amount from Company A. If this is not payable, use a different account. Then, track the received money via bank deposit or journal entry. If it's payable, add company A as a vendor and create a check for them or record the repayment as a journal entry.

That will do it. If you have other questions in mind, feel free to go back to this thread.

You have clicked a link to a site outside of the QuickBooks or ProFile Communities. By clicking "Continue", you will leave the community and be taken to that site instead.

For more information visit our Security Center or to report suspicious websites you can contact us here